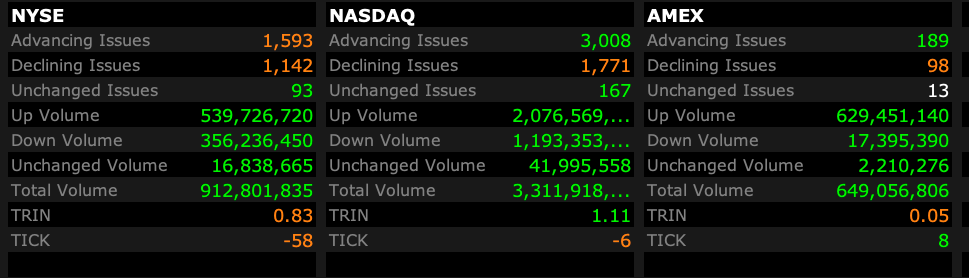

Late Morning Market Stats and Charts

– NYSE volume 23% below its one-month average;

– Nasdaq volume 4% below its one-month average;

– VIX index: up 1.28% to 16.62

Positions: None.

– NYSE volume 23% below its one-month average;

– Nasdaq volume 4% below its one-month average;

– VIX index: up 1.28% to 16.62

Positions: None.

JavaJoe

7m ago

Have you basically become a day trader now? It’s an honest question.

Dougie Kass

just now

absolutely not

when i am wrong as rain on the market, i trade much more actively to hit the cash register – since i dont want to have much long exposure — i typically do this with the indices… so you see all my index trades

i always trade around longs and shorts – always

you see my day/trade/transactional stuff because, well because i am transparent – holds are holds , trades you see as it is transactional

on the short side (as i have been bearish) i have held more than 15 positions for years

i would much prefer catching a primary trend (down or up) and just hold… so much easier.

Positions: None

From Peter Boockvar:

Core retail sales in May rose .7% m/o/m after a .5% increase in April and that was 3 tenths above the estimate. Above this line, sales for autos/parts were up by 1.2% m/o/m after dropping by .9% in the month before. They are up 1.8% y/o/y. Building material sales were flat and up by 1.8% y/o/y. As to be expected, gasoline station sales increased by 3.4% m/o/m and 25% y/o/y with price being the main reason.

Sales were up in furniture, clothing, sporting goods, online retail, general merchandise (like department stores) and in the miscellaneous category which includes dollar stores, convenience stores, pet, etc…

On the downside, sales fell for electronics after strength in the prior months and still up 5.9% y/o/y. Sales dropped by one tenth at eating/drinking establishments but after a .9% rise in April and sales here were up 2.4% y/o/y.

Bottom line, a lot coursing thru this data. We have tax refunds on one hand but we also have inflation, mostly at the gas pump on the other and a reminder too that this data is in nominal terms. Wages are still growing but now less than inflation and in part why the savings rate keeps dropping. And we wonder how much of the lift in sales was a consumer response to buy things ahead of expected price increases.

While not apples to apples, headline retail sales were up 6.9% y/o/y (after a 4.8% increase in April) vs the May CPI rise of 4.2% (vs 3.8% in April).

Treasury yields didn’t move much in response with the 2 yr at 4.06%, the 10 yr at 4.43% and the 30 yr at 4.93%.

Positions: None.

Chart from 9:52 a.m. ET.

Positions: None.

Positions: None.

* And another positive for the overall cannabis picture…

That the market is ignoring the mounting positives for weed has provided me with what I think is a superb opportunity to increase my cannabis exposure.

Position: Long Cannabis

From Peter Boockvar:

I really look forward to hearing from Kevin Warsh today. I think he’s going to be a refreshing rethink to what has been a standard, mostly Keynesian approach for years to how they model the economic data (mostly focusing on the demand side), how they use monetary policy (aggressively over the past 40 years and with forward guidance as a tool) and what will become of both the balance sheet and future use of QE (bloated and too big a footprint in markets).

I think for now with respect to rates and with an effective fed funds rate currently at 3.63%, around a zero real rate and if one uses headline inflation, its below zero, Warsh & Co should just sit tight and wait to see where prices settle out at, particularly oil prices, as supply chains normalize with the Strait reopening because until then they will have incomplete information.

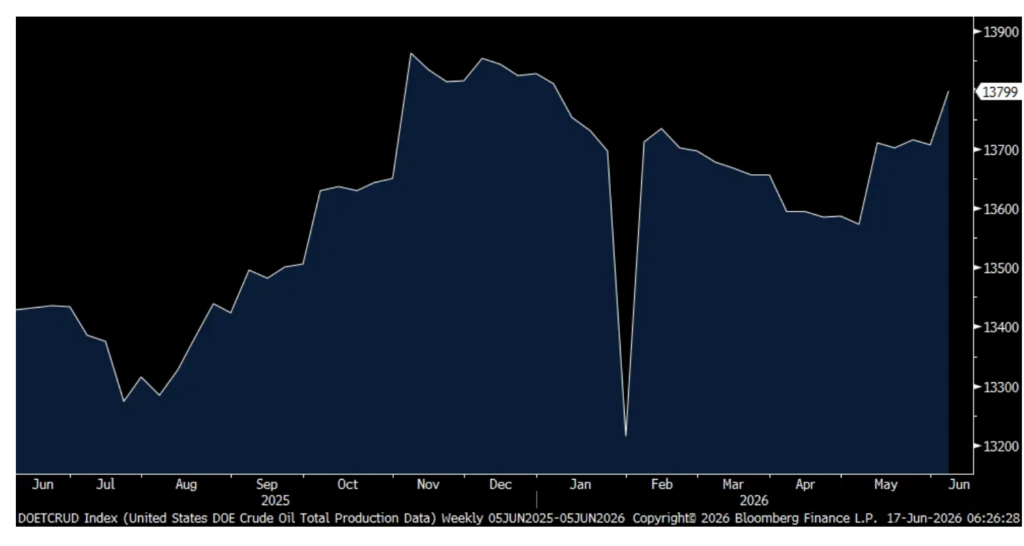

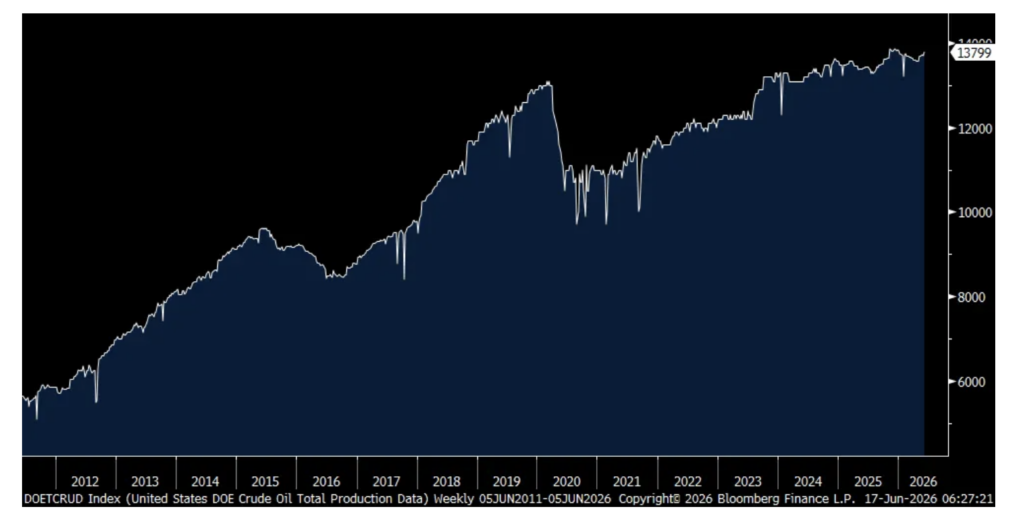

When thinking about oil prices from here and where they eventually stabilize at, I want to highlight again something I talked about in January that is a big picture support, I believe, for crude oil prices. And that is a plateauing of US oil production. It’s not because drillers don’t want to drill, it’s instead the reality of geology in that many of the US shale basins are now seeing a flattening to lower production rate and the rate of growth out of the Permian in particular is slowing as well.

I include two charts, one over the past year of US oil production and one stretching 15 years that reflects both the dramatic increase in production that the technological wonder of shale drilling brought and took the US to the number one in the world spot but also relative to the slowdown in production seen over the past 8 months.

US Oil Production over past year at 13.8mm barrels per day

US Oil Production over past 15 years, from about 5.5mm per day to almost 14mm

Dave & Buster’s reported Monday after the close and its stock fell 5% Monday even with lower oil prices and another 6% Tuesday in response to the earnings. They said this of note:

“We started the quarter well in February. The spring calendar shift between March and April played out largely as expected. But the macro backdrop, elevated gas prices, geopolitical uncertainty, and meaningful softness in consumer sentiment, they all were a real headwind in April.”

They ended the quarter with comps down 5.4% y/o/y. In Q2 to date, they are trending a bit better, down 4% so far.

“Consistent with what we have seen here recently, certainly that lower end consumer is where we’ve seen most of that pressure. The higher end middle consumer is consistently trading but we’re seeing more of that pressure on the low end and that’s part of really what we’ve been trying to focus on with our value offers.”

La-Z-Boy is jumping pre market as while sales were about as expected, profits were much better than estimated. In their release they said this of note:

“Written same store sales decreased 2%, a sequential improvement, as lower traffic was partially offset by higher conversion rates, average ticket, and design sales. During the quarter, same store sales trends were strongest in April with positive comps.” They referred to “an industry that remains soft” and “While we continue to have a measured view of the external environment, we expect to continue to outperform the industry.”

With the average 30 yr mortgage rate holding at 6.60%, purchase applications fell 3.4% w/o/w after rising last week by 7.3% vs the previous 3 weeks of declines. Refi’s were down by 4.5% after last week’s pop that also followed declines in the previous few weeks.

Shifting gears overseas. The Swedish Riksbank decided to not follow the ECB with a rate hike and they held their policy rate at 1.75% as expected. That said, they are leaning to a hike and said “The Executive Board assesses that it is well balanced to leave the policy rate unchanged at 1.75% now, but the probability that the rate will be raised later this year has increased in relation to the assessment in March.” The Swedish krona is little changed in response.

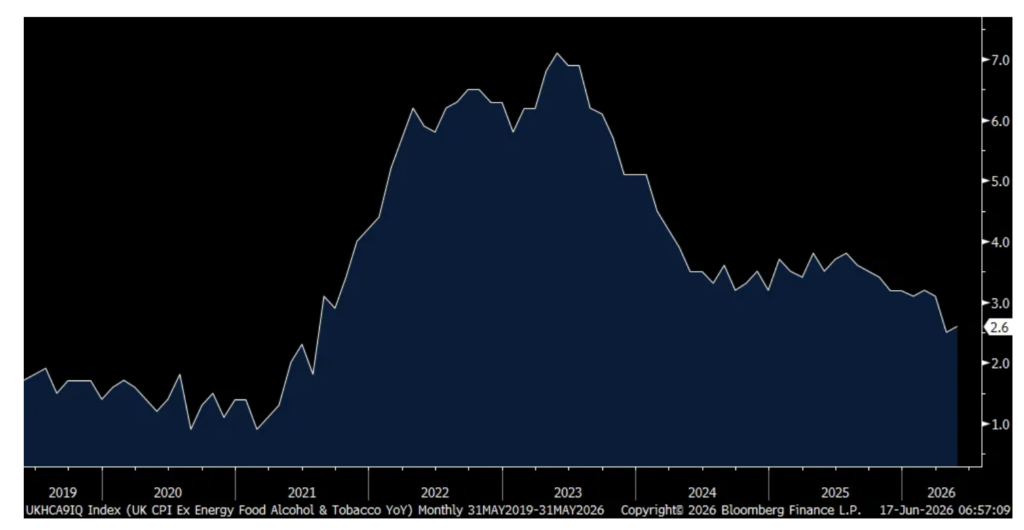

Ahead of the BoE meeting tomorrow where no change with its base rate of 3.75% is expected, the UK May CPI rose 2.8% y/o/y, 2 tenths below expectations and the same pace seen in April. The ONS said lower food prices kept a lid on price gains but as energy bills reset in coming months, that will be a headline figure offset from here. The core rate was higher by 2.6% y/o/y vs 2.5% in April and one tenth below the estimate. Services inflation remains the problem, rising by 3.7% y/o/y vs 3.2% in the month before.

I think the BoE is in wait and see mode too. Gilt yields are lower by 5-6 bps in reaction to the below estimate print. The 10 yr inflation breakeven is down by 3.6 bps to 3.18%, the lowest since early March.

UK Core CPI y/o/y

Positions: None.

We remain short Spacey.

Positions: Short $SPCX

Positions: None.

I added to my Index shorts:

* SPY ($SPY) $751.49

* QQQ ($QQQ) $734.53

Positions: Short SPY M QQQ M