Quarter-End Markups Make Presence Known in Tone-Setting Session

Tuesday’s stock market action was all about position for the second half of the year.

Tuesday’s stock market action was all about position for the second half of the year.

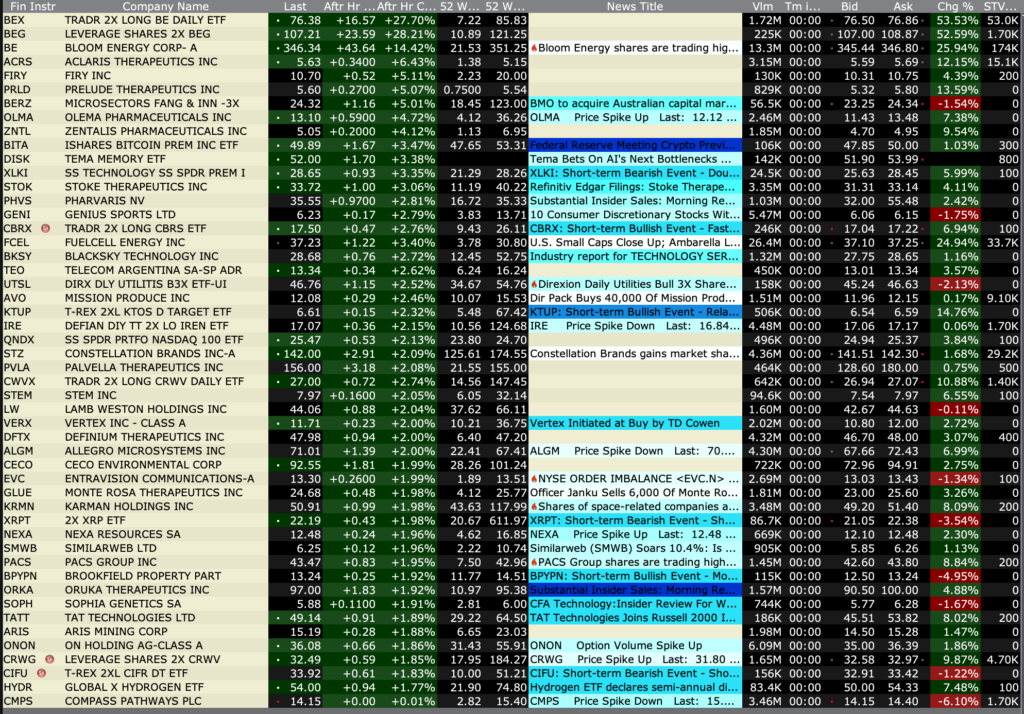

After-Hours % Advancers

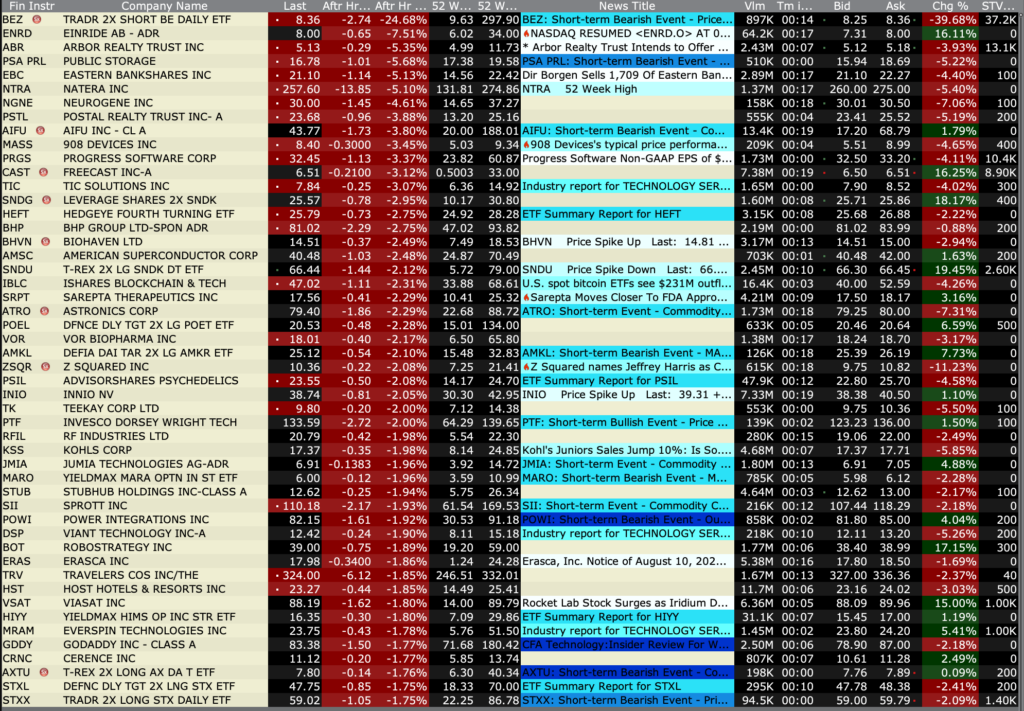

After-Hours % Decliners

Position: None

Closing Volume

– NYSE volume 9% below its one-month average

– NASDAQ volume 19% below its one-month average

– VIX index: down 6.91% to 16.43

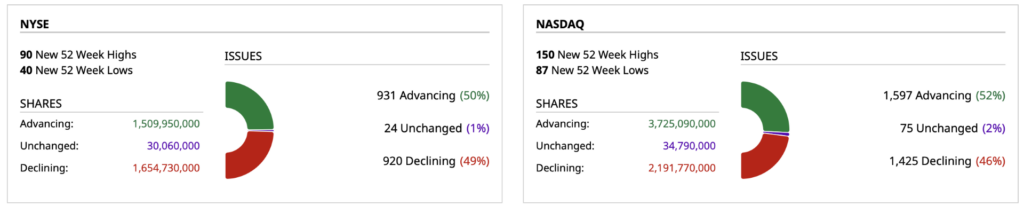

Breadth

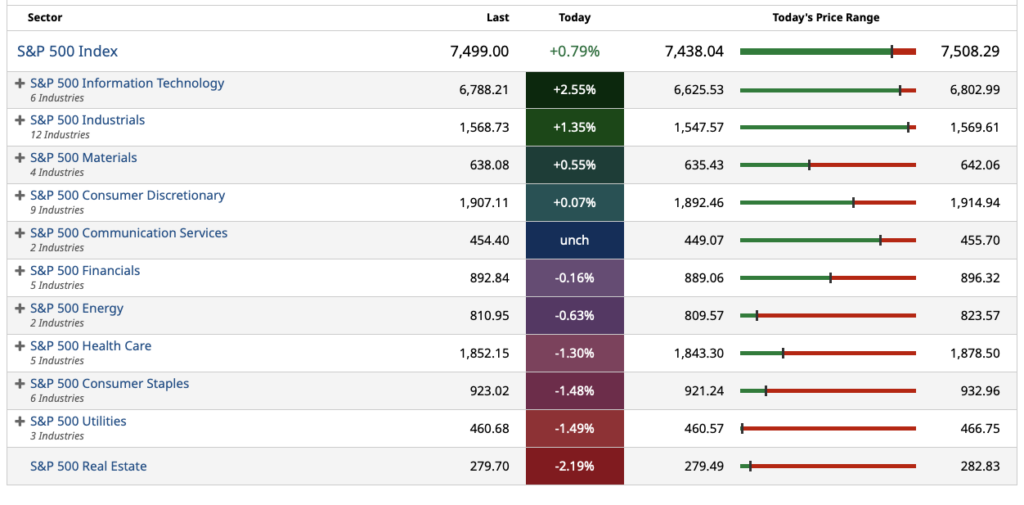

S&P 500 Sectors

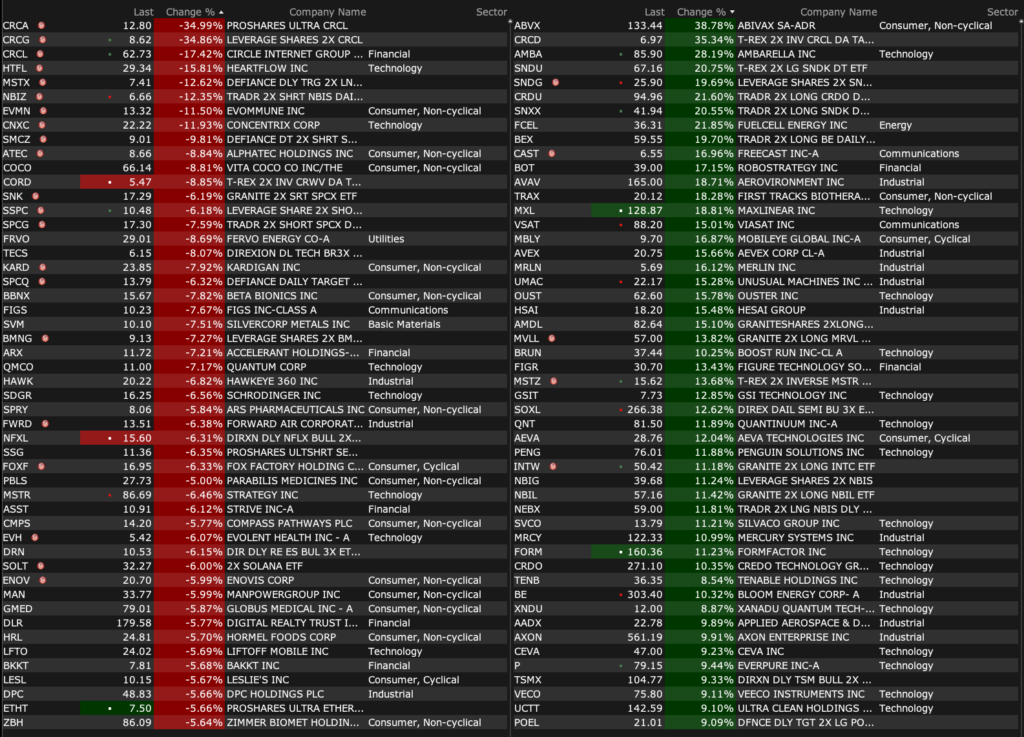

% Movers

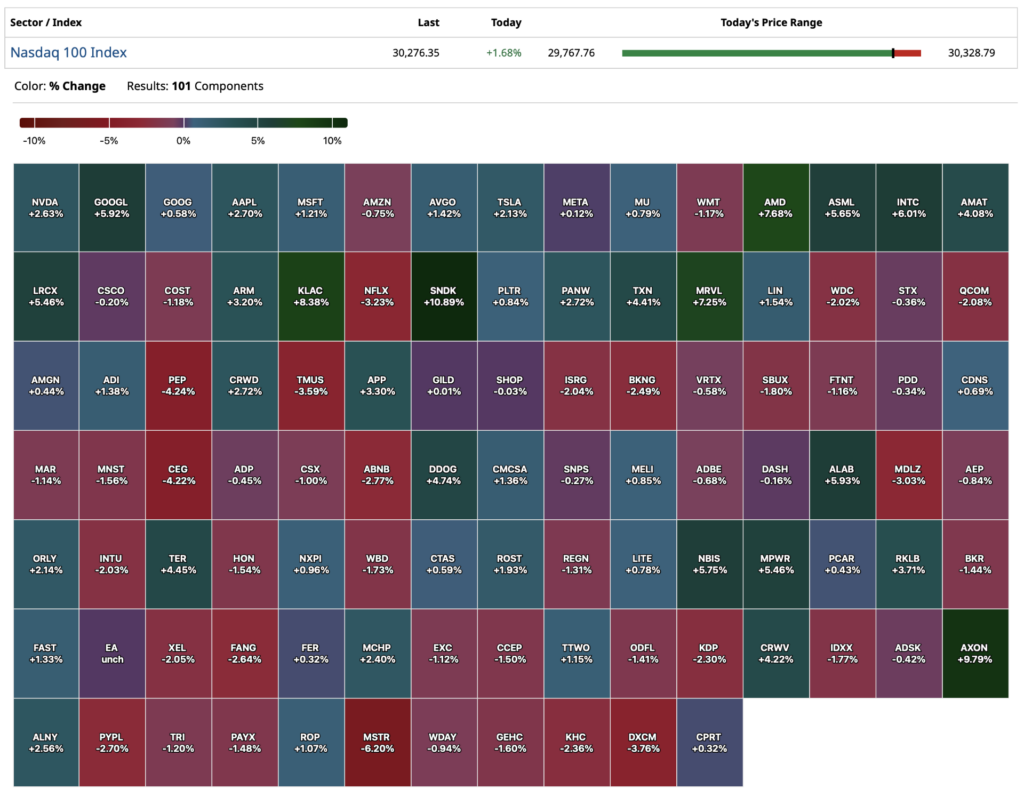

Nasdaq 100 Heat Map

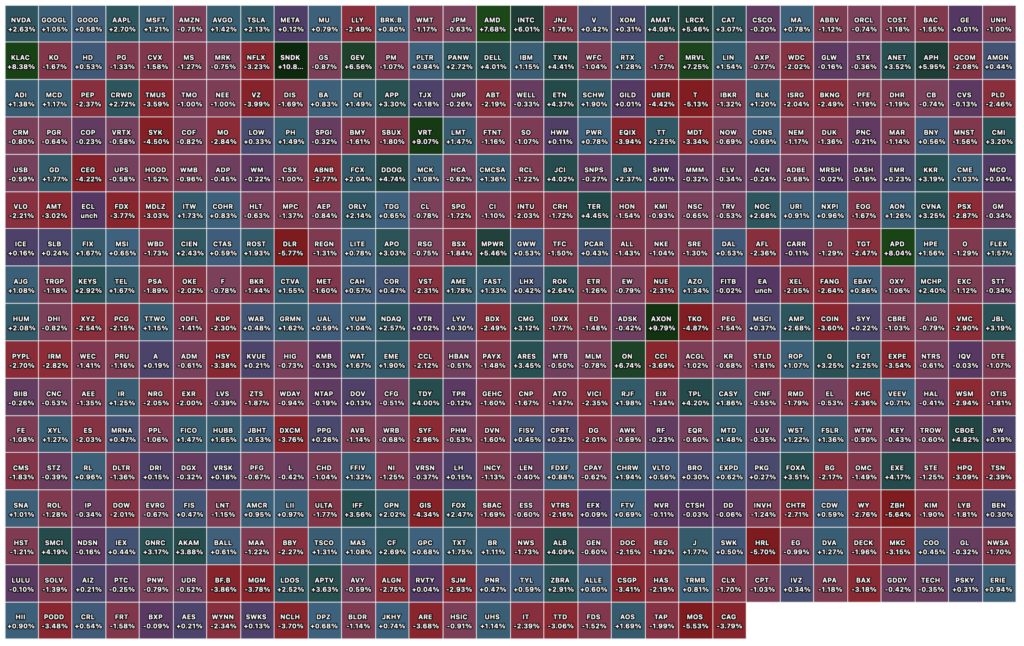

Closing S&P 500 Heat Map

Position: None

EARNINGS AFTER CLOSE TUESDAY, JUNE 30

EARNINGS BEFORE OPEN WEDNESDAY, JULY 1

Position: None

I am heading out early to pick my granddaughter up at camp.

Enjoy the evening.

Thanks for reading.

Be safe.

Position: None

Position: None

I am adding a second tranche to my high-beta tech short basket now with S&P cash +60 handles.

Position: Short high-beta tech basket

This pair of stocks is on our radar as both names have entered overbought territory.

As I noted in my 8 Reasons I’m Getting More Positive on Cannabis, the custodian issues are about to be resolved with rescheduling and uplistings:

Position: None

Let’s set the stage for part two of the process and discuss two other things we’ll be watching tomorrow.