Boockvar on Orders, Builder Sentiment

From Peter Boockvar:

Pull forward of orders now over?/Builder sentiment

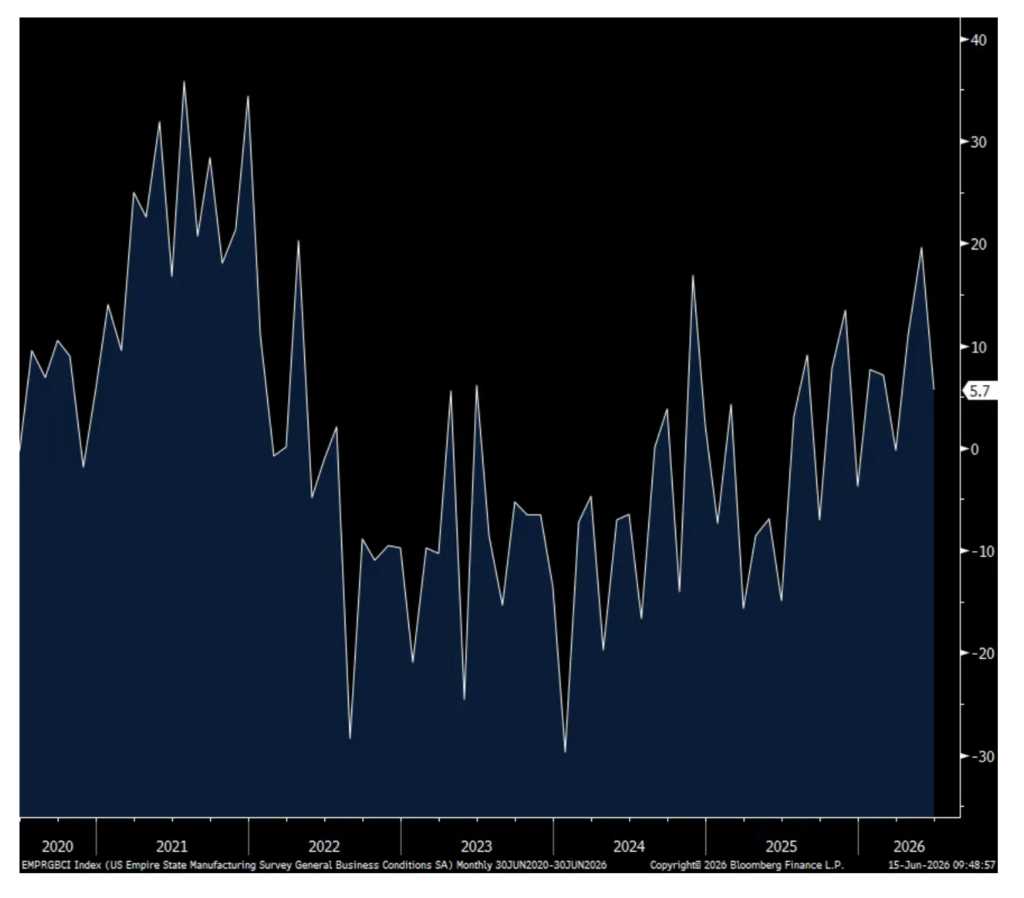

Now we watch to see the extent to which orders were pulled forward over the past few months. Ahead of this but reflecting that some of this has already taken place, the June NY manufacturing index fell to 5.7 from 19.6. Specifically, new orders fell to 3.5 from 22.7 in May and 19.3 in April while inventories dropped to zero from 9.7 in May and 5.1 in April. Backlogs though were little changed m/o/m at 5.0.

Delivery Times gave back the May jump but remained elevated at 11.9. Prices paid stayed high but a bit less so at 61, down 1.6 pts. Prices received at 31.4 was also little changed m/o/m but 7.6 pts above its 6 month average. Employment stayed above zero at 9.6 but the workweek fell, though was above zero.

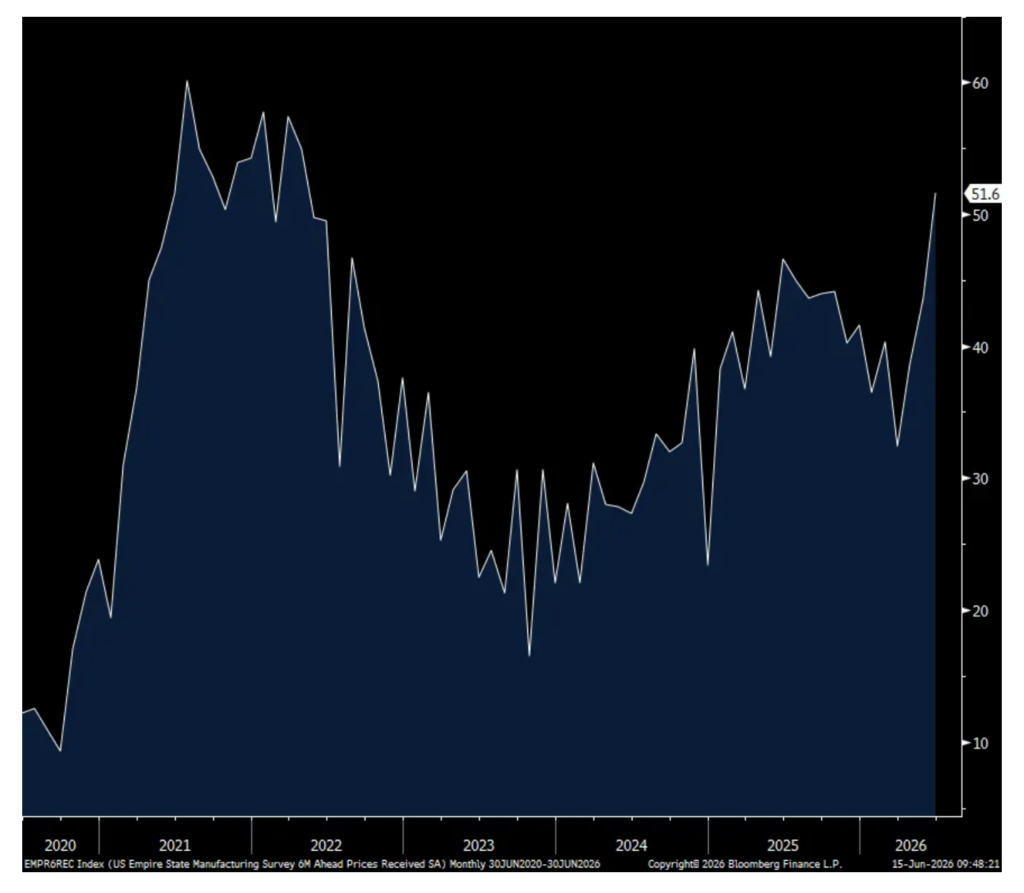

The six month business outlook at 30.1 was down 3.4 pts m/o/m and about where the half year average is. Of note, the six month expectation for price received rose 8 pts to the highest since April 2022. The six month outlook for prices paid slipped by 2.7 pts to 59.4 but that is still above its half year average. Capital spending plans dropped by 4.6 pts to 10.9, a 5 month low.

Bottom line, as stated, we now get to see how much of the recent lift in manufacturing was organic end demand and how much of it was the front loading of orders ahead of expected price increases and/or supply challenges. On the cost side, price pressures are clear on the producer side that will hopefully now get some relief but unless things go back to the cost structure of pre March, companies will still do what they can to recapture lost profit margins. That will be done either thru further productivity gains and/or cost cuts and/or less hiring and/or price increases.

NY Mfr’g

Expectations for Prices Received

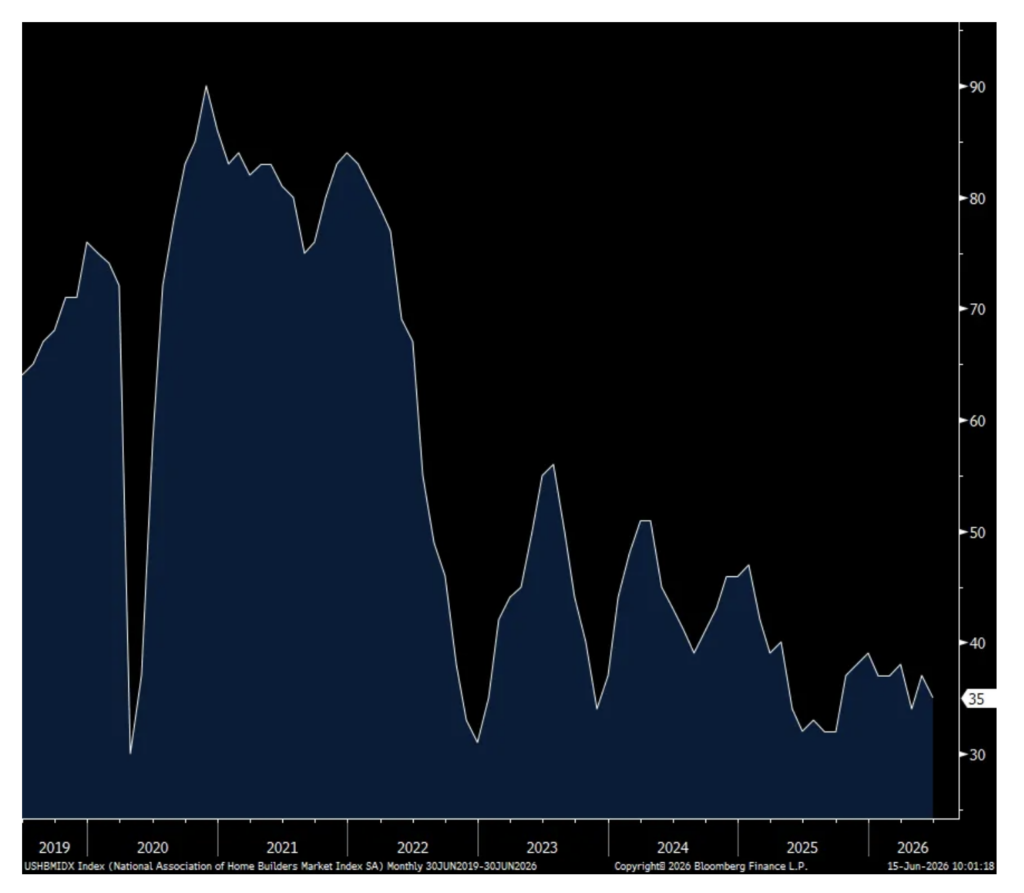

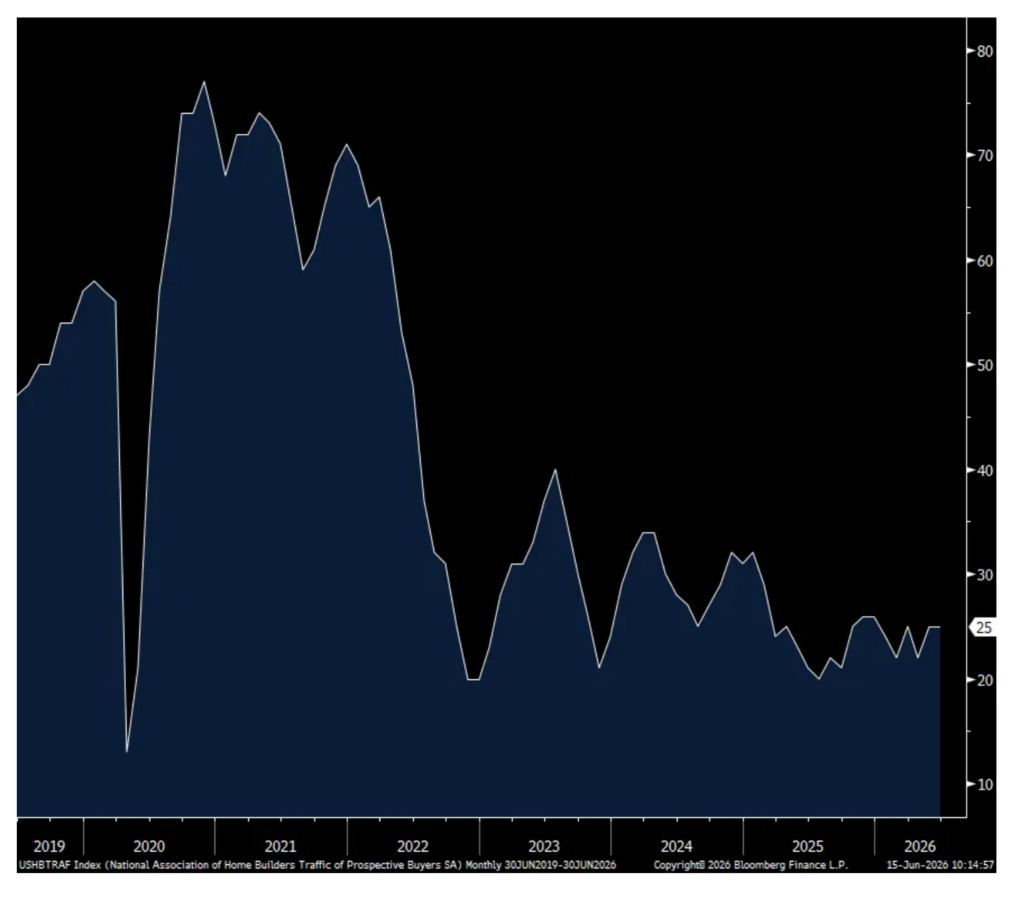

The June NAHB home builder sentiment index fell to 35 from 37 and vs the estimate of no change and thus remaining well below the breakeven of 50. The Present situation fell 2 pts to 38 after rising by 3 pts last month. The Future outlook was unchanged at 45. Prospective Buyers Traffic remained depressed at 25.

The NAHB talked about what builders are doing to drive sales, “The latest HMI survey also revealed that 35% of builders cut prices in June, up from 32% in May. The average price reduction was 6% in June, the same rate as the previous month. The use of sales incentives was 62% in June, up slightly from 61% in May, and marking the 15th consecutive month this share has reached 60% or higher.”

They also blamed government policy that is limiting the ability to deliver supply. “Costly and inefficient regulatory policy is clearly impeding the ability of builders to increase the housing supply. According to a new NAHB study, government regulation, taxes, fees and other costs add more than 26% to the price of an average single-family home. Easing permitting bottlenecks, density limits and inefficient zoning rules would help reduce costs and support the housing growth the nation needs.”

With respect to mortgage rates, they averaged 6.54% in June vs 6.41% in May. We know all about the affordability challenges and they remain until proven otherwise.

NAHB

Prospective buyers traffic

Positions: None.