Boockvar on Price War, Oracle Spend, Cracker Barrel

From Peter Boockvar:

A price war coming?/Oracle’s spend, Casey’s customer and more/Shipping costs/BoC

A highly capital heavy business with little pricing power typically creates a lower margin business and likely subject to commoditization. The biggest beneficiary is usually the customer. That is what I thought when I read this article today in the WSJ titled “OpenAI considers drastic price cuts, anticipating war for users with Anthropic…The company might lower prices for tokens, the central unit for gauging AI costs, though the discussions are still in flux…The move would be in anticipation of similar cuts the company expects at Anthropic, the people said.”

We know the CapEx costs are astonishing and they keep getting ever more so. Oracle, who just finished its FY ‘26 ended up spending $55.66 on CapEx (net cash outlay of $48 billion and $8 billion of customer prepayments), a whopping 83% of FY ‘26 revenue. In FY ‘22, before all this spending started, it was 10%. For FY ‘27, they expect to spend $90 billion which is 100% of expected revenue but they say they’ll cover $70 billion of that and $20 billion will come from customer prepayments. That’s up from the prior estimate of $67.6 billion.

On their huge $638 billion of remaining performance obligations, “we expect 12% to be recognized in the next 12 months and another 34% between 13 and 36 months. And these percentages are both expected to accelerate over the coming quarters based on our current long-term outlook.”

And this is the crux and reasoning for the massive bet the company is making, “We’re on the front end of one of the most interesting times in the technology business. Our customers are now focused on how to leverage AI to interrupt businesses. They want AI to increase productivity, enhance customer service, and create real competitive advantages. So they want to do it quickly and within their existing budget envelope. Oracle’s unique advantage is that we deliver the applications, the data, the infrastructure, the AI tooling, and the industry expertise together. That combination invariably puts us at the center of customer conversations, whether they’re existing Oracle customers or not. And our customers have moved past the experiment stage with AI. They are ready to implement enterprise grade complete agentic solutions to help run their businesses.”

And to help close their cash flow and large funding gaps, “we expect to raise around $40 billion in debt and equity in our fiscal year ‘27, and that includes our already announced $20 billion at the market equity issuance. We don’t anticipate raising additional debt funding in calendar year 2026.” Their long term debt two years ago was $82.5 billion including lease liabilities and with the quarter just ended that figure is now $149 billion.

Selling pizza, gasoline and beef jerky, among many other things, is not quite the excitement of producing cloud infrastructure or high bandwidth memory semiconductors but Casey’s General Store does it really well and its stock jumped 20% yesterday after earnings. They said this of note:

“Whole pizzas and non-alcoholic beverages helped drive the strong results during the year.” They had a big quarter selling Monster energy drinks with a red, white and blue Razz flavor to celebrate America’s 250. They are also doing big business selling nicotine alternatives to cigarettes and I’m sure a lot of Zyn pouches. We are long Philip Morris International.

And high level, “So with respect to the consumer, I would say overall, I think consumers are hanging in there. They’re probably being a little more discerning about where they shop and how they spend their money. But we’re seeing growth across all of the income cohorts. And the way we look at that is below $50,000 a year in income is a low income, $50,000 to $100,000 a year is mid and above $100,000 is higher income. And I’d say that all three, we’re seeing growth, a little bit less so in the lower income. The other two cohorts, which is three quarters of our guest base, are spending comparably to what they’ve been spending on.”

“In terms of specific behaviors, we’re not seeing a lot of change on the inside of the store. We are seeing some change in fuel, but it’s very minor. And it’s all the things that we always talk about. If fuel prices get high, we start to see premium sales dip a little bit. We see sales of ethanol blended fuel go up because it’s a little cheaper. We see gallons per transaction drop a little bit. We see fuel transactions themselves go up because people are coming more frequently. So all of those dynamics are happening right now, but in low single digit percentages. So this is kind of very nuanced behaviors.”

Remember that in the quarter before, right after the war started and the average gallon of gasoline was still in the 3s, Casey’s thought $5 per gallon is where you would see demand destruction.

From Chewy and whose stock fell 2% yesterday:

They mentioned that the consumer environment “weakened in the latter parts of the quarter” but still grew sales 7.7% y/o/y.

“Pet remains a resilient category driven by recurring non-discretionary needs and strong emotional attachment. At the same time, consumers are growing more discerning, driven in part by elevated fuel prices and broader macroeconomic pressures.”

“we are seeing a modest level of incremental pressure on premiumization and product attach rates amongst our current customer base…We no longer believe it is prudent to embed a meaningful acceleration in consumer spending into our outlook, given the current operating environment.”

Cracker Barrel Old Country Store has been trying to recover from its rebranding fiasco last year and its stock popped 23% yesterday. From them:

Customers are coming back and “our Google Start rating increased 4%, reaching its highest quarterly score since 2018, while our food taste and service scores rose 5% and food temperature scores increased 7%.”

They are also benefiting from having a lower average check size relative to the industry. “In Q3, our average check was $15.85 compared to over $27 in casual dining and over $19 in family dining, underscoring our lower prices versus competitors. In fact, guests can order add-ons with us and their check will still be lower than an entree at many of our peers.”

Business still fell in the quarter, with comps down 2.6%, “which included a traffic decline of 6.7%. Although traffic remained negative, we are encouraged by the gradual improvement in the underlying traffic trend. The restaurant average check increased 4.3%, including pricing of 4.4%.”

We’ve heard in many of the global manufacturing PMI’s and from some companies that a factor in the improvement in manufacturing has been the pull forward of ordering ahead of expected price increases and/or possible supply issues. MMM spoke at a conference yesterday and talked about this in response to a question with respect to their pick up order rates:

“So, basically, yes. So, what happened is we typically go out with price increases on April 1. And what was happening in the Middle East we saw oil prices coming up. So, we went out with additional price increases on top of what was April 1. And we said, based on our performance, the innovation, on-time delivery, our responsiveness into the channel, we believe our ability to drive price is a lot better. And so we’re going to hold a line on that.”

And the response, “So, naturally we thought we would see some acceleration of orders. It was probably some of that. But, given the momentum we saw in April, in May, and now into June on orders, there might have been some pre-buy. But, predominantly, it is innovation driven, commercial excellence driven, and probably less so on the pre-buy.”

They are certainly seeing business strength that is macro driven, “like semis are good. Our data center business has been pretty good. Aerospace and defense has been pretty good. Commercial branding in Q1 was pretty good.”

Where there is some pressure, “around consumer electronics, auto, a little less so on the US consumer.”

Shifting to some general macro.

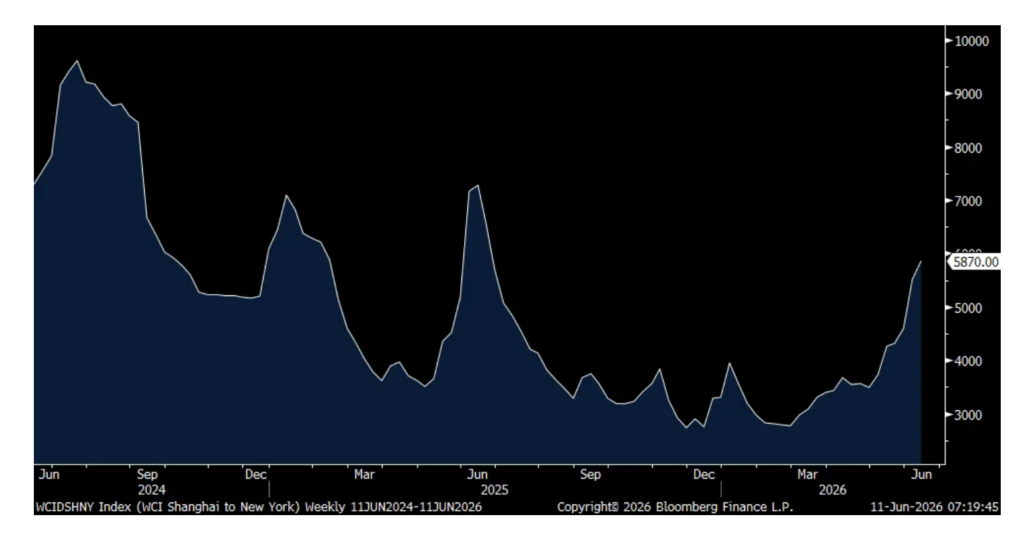

Container shipping rates continue to rise and we’re seeing a general increase in freight transportation as I’ve also highlighted, particularly with trucking. The Shanghai to NY average 40 foot container price jumped by another 6.6% to $5,870, the highest in a year. Shanghai to LA saw its price up by 2.6% w/o/w to $4,683 after spiking by 31% last week. The Shanghai to Rotterdam route rose to the most expensive since January 2025.

Shanghai to NY

Speaking yesterday, the Bank of Canada Governor in his presser distilled the box central bankers are in quite succinctly. Tiff Macklem said “Economic weakness combined with rising inflation is a dilemma for monetary policy. Raising rates to dampen inflation could further slow the economy. Easing rates to support growth increases the risk that higher inflation becomes persistent. For now, holding the policy rate unchanged balances those risks.”

The end result yesterday with the market response was no change in FX and yields but today yields are down with the European and US slight drop in yields and the Canadian dollar is down slightly on the week.

Positions: None.