Boockvar on Wholesale Cost Pressures, European Central Bank Rate Tweak

From Peter Boockvar:

Stiff wholesale cost pressures/Claims lift/Rate tweak for now from ECB

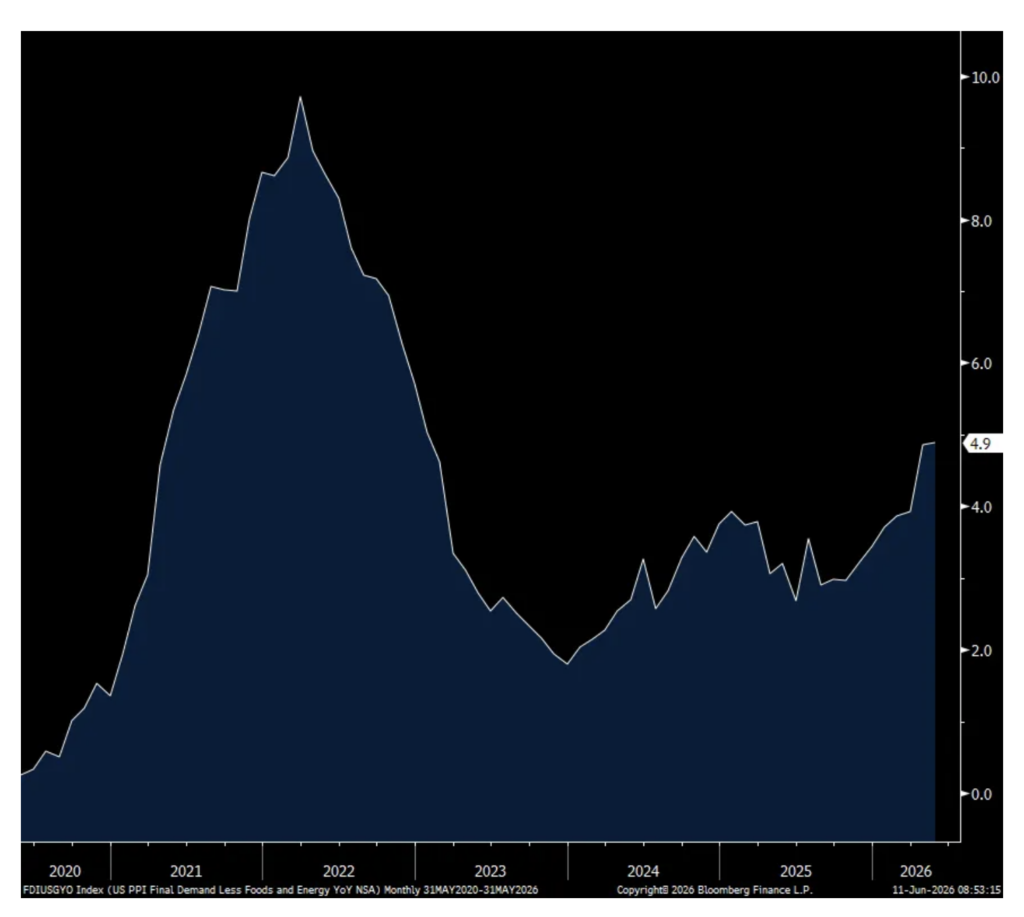

When we include the downward revision in April for the heady PPI read, the May headline figure was as expected but showing a 2nd straight month of 1.1% wholesale price increases after a .7% gain in March and .6% gains in each of January and February. The y/o/y headline gain was 6.5%, up from 5.7% in April. The core rate was higher by .4% m/o/m after a .7% increase in the month before and which followed an .8% gain in January, .4% rise in February and .2% increase in March. Core wholesale prices are up by 4.9% for a 2nd month y/o/y. Energy prices as expected were higher by 10.7% m/o/m and 37% y/o/y. Food prices gained another .6% m/o/m and 2.6% y/o/y.

Core goods prices were up .8% m/o/m and by 5.1% y/o/y with plastic resins and industrial chemicals leading this ex food and energy category.

On the services side, prices were up .3% m/o/m and by 4.9% y/o/y and higher asset prices were a factor. The BLS said “Over 40% of the May advance in the index for final demand services can be traced to a 4.8% rise in prices for portfolio management.” That follows a 2.3% drop in April. Of course though, there are other things like higher prices for truck transportation of freight (up 3.4% m/o/m and 17.3% y/o/y), air transportation of freight (up .5% m/o/m and 5.7% y/o/y) chemicals and allied products wholesaling (up 6% m/o/m and 16.4% y/o/y), food wholesaling and airline passenger services. Prices fell for machinery/equipment wholesaling and real estate loans.

Bottom line, strength in goods prices ex food and energy, drove the higher core rate while the obvious sharply lifted the headline. Those rising transportation costs also flows through to every business that has to stock stuff on the shelves, both goods producers and service providers and whether at the intermediate stage of the supply chain or final stage. We now have a more complete picture of the US inflation situation with the main question right now being who will have to absorb the widespread cost pressures. Stretching out the US Treasury market reaction from 8:29am est yesterday, 2s, 10s and 30s are about unchanged but with the 2 yr holding above 4.10%, the 10 yr above 4.50% and the 30 yr yield more than 5%. Inflation breakevens are little changed too with most of the recent rise in interest rates being more on the REAL side.

Headline PPI y/o/y

Core PPI y/o/y

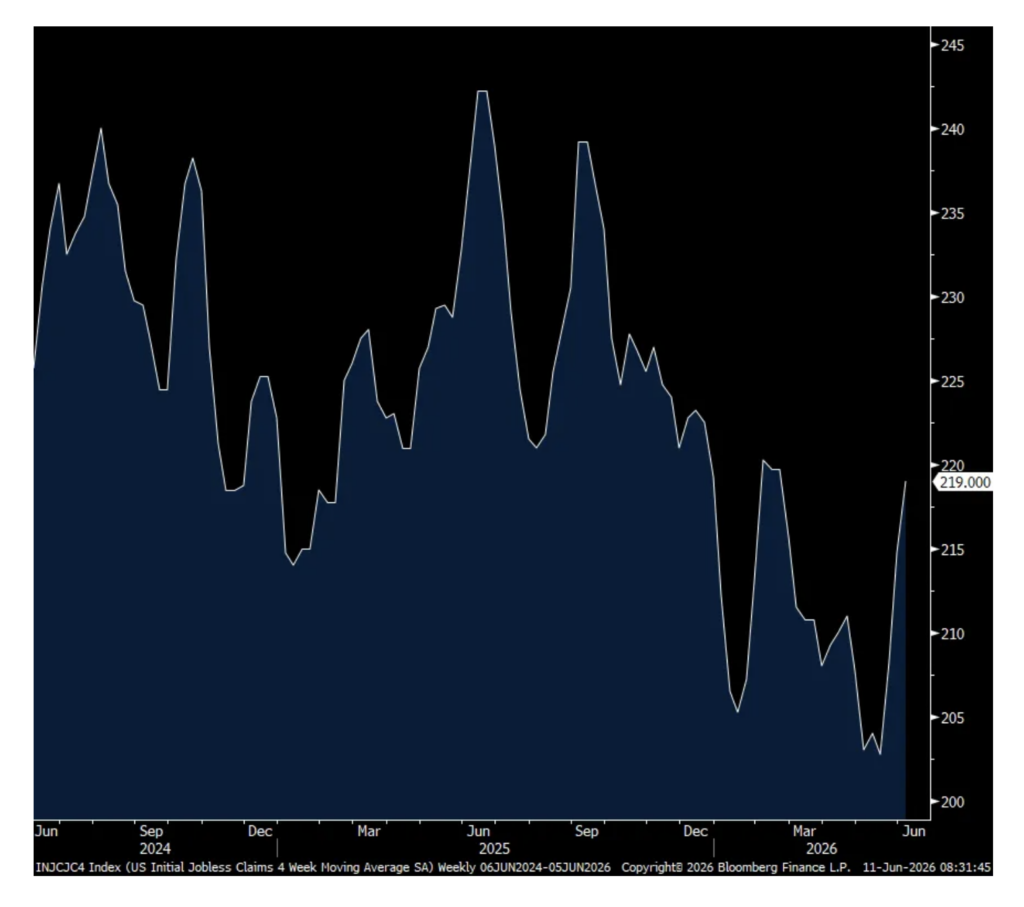

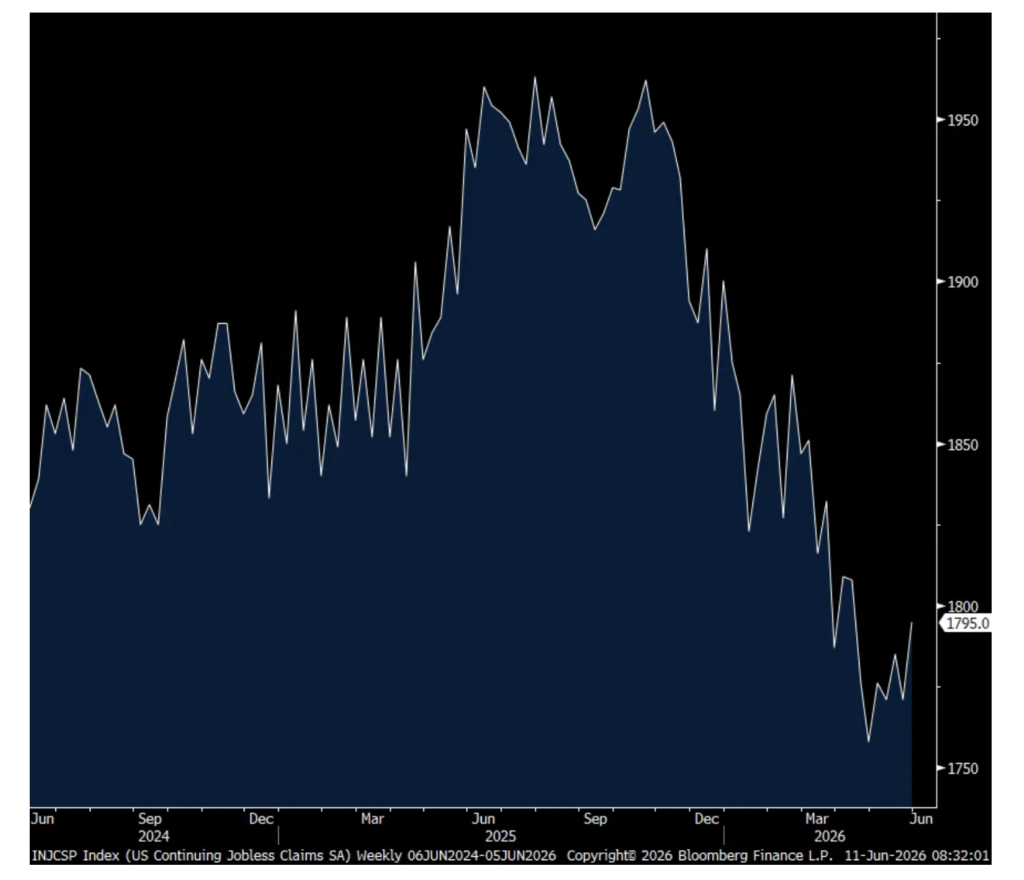

Initial jobless claims rose 4k w/o/w to 229k and that was 9k more than anticipated. This brings up the 4 week average to 219k from 215k and while still low, is the most since February. Continuing claims rose by 24k to 1.795mm which is a 7 week high but still below the 1.9mm ish that we saw last year.

While an uptick was seen in claims relative to expectations for the 2nd week, overall the data, as measured here (not including those that take gig jobs when they get laid off and/or those that receive severance), reflects a modest pace of firing’s. With continuing claims, the drop off from the highs is likely a mix of people finding new jobs and for some, claims that are expiring as there has been a rise in the time it’s taking in finding a job as seen with last week’s payroll report.

4 week avg Initial Claims

Continuing Claims

As fully expected, the European Central Bank raised its deposit rate to 2.25% from 2.00%. While they have chosen to not look past the higher oil price shock, they also previously took its rate down to zero on a REAL basis which was already quite aggressive.

In their statement they said “The outlook remains uncertain, with upside risks for inflation and downside risks for economic growth.” Stating the obvious right now.

What they do next we await to see if Lagarde hints at it but for now I view this hike more of a tweak rather than beginning of a fresh rate hiking cycle until we see how things further play out from here. The euro is little changed as no surprises yet and European yields remain lower on the day.

Positions: None.