The Market Bacchanal Rages On — While I Remain Celibate (Part 3)

This is Part 3 of a multi-part discussion of the markets (Read Part 1 here and Part 2 here)…

My Market Concerns Summarized

In my view, the markets have ignored the same conditions that set off the January-February selloff. None of the non-war issues that drove stocks lower have been resolved:

* Oil prices are off their highs but are likely to remain elevated because of the magnitude of the supply shock and continued uncertainties related to the Iran conflict.

* Inflation is now rising on a sequential monthly basis — and is higher than before the conflict in Iran.

* Interest rates will be higher for longer.

* The 2026 annual deficit will approach $2 trillion, and neither political party show any signs of being fiscally responsible.

* The U.S. debt will hit $40 trillion this year — the cost of servicing the debt is over $1 trillion/year.

* With a burgeoning deficit, stiff debt load and persistent inflation, the Fed’s hands are tied.

* While private equity’s problems are not systemic, the leverage they brought us remains in place. KKR Private-Credit Fund Takes $560 Million Loss – WSJ

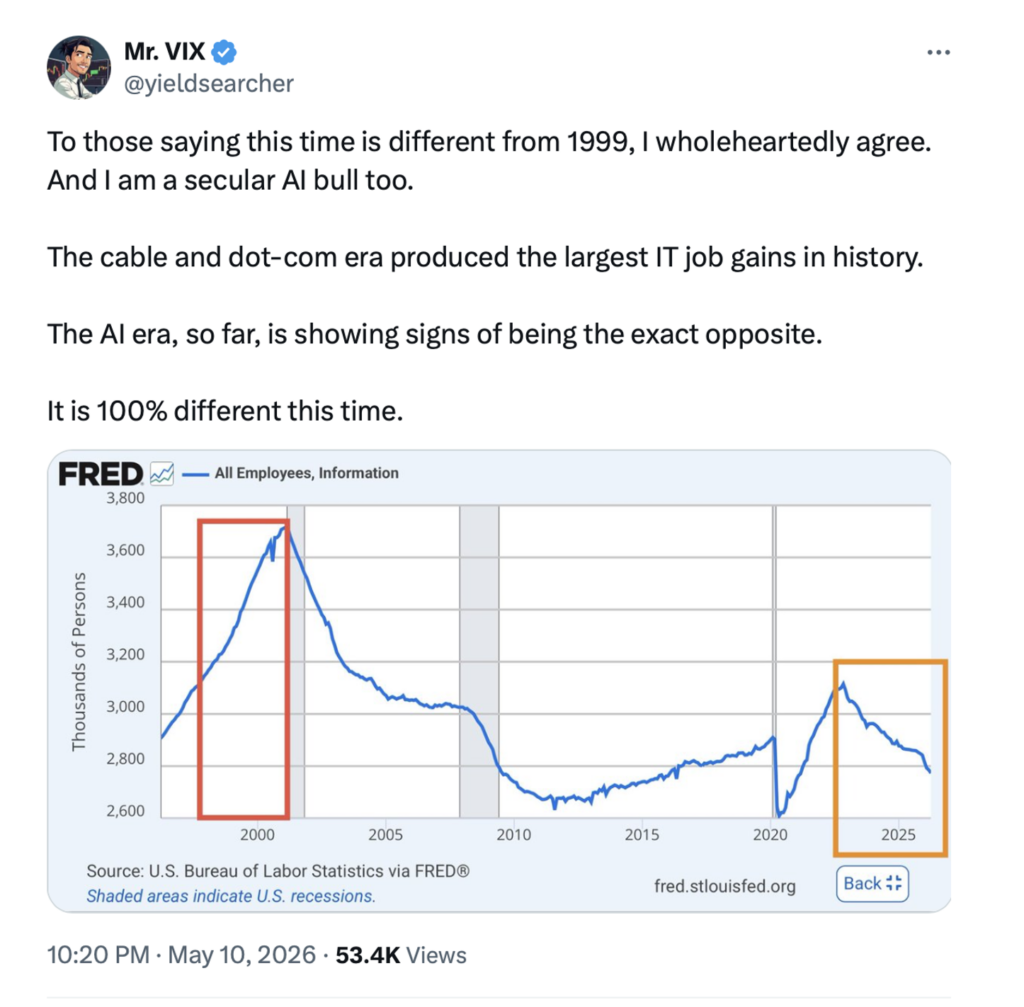

* The enormous amount of money spent on AI will probably never see an adequate return on investment. As noted by Stan Druckenmiller (again!), AI’s societal and transformative impact could rival the internet’s life-changing influence — and so may the stock market consequences (rhyme) be similar:

“If we were all sitting here in 1999 talking about the Internet, I don’t think anybody would have estimated it would be as big as it got in 20 years. And yet, if you bought the Nasdaq in ’99, it went down 80% before that all came to fruition. That’s not going to happen with AI. But it could rhyme – AI could rhyme with the Internet as we go through all this capital spending we need to do. The big payoff might be four to five years from now. So AI might be a little overhyped now but under-hyped long term.”

* Valuations are a terrible clock but a good weather forecast. That valuations are stretched is an understatement. See CAPE Shiller in Part 2. The Buffett ratio (the total market capitalization divided by GDP) hit an all-time high this week). Most other traditional metrics indicate that equity valuations are in the 97 percentile.

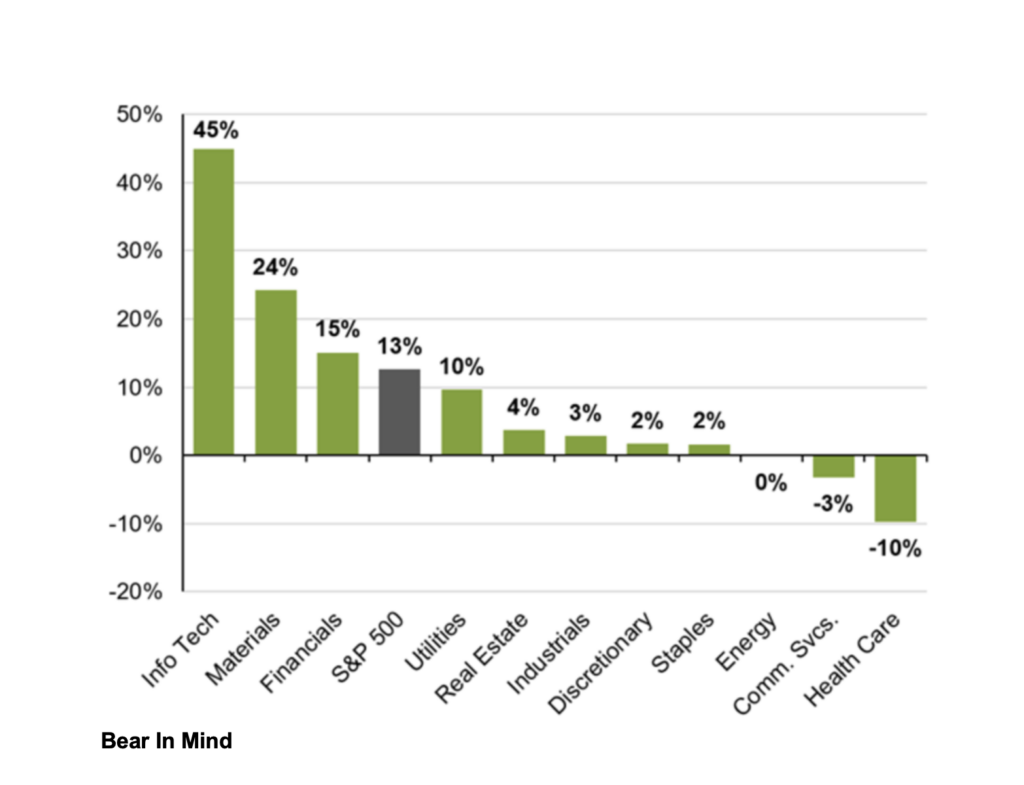

* Many bulls highlight the improving strength in projected 2026 S&P EPS. They argue that this year’s robust growth in profits (at about +17%) justify current valuations. However, if one takes out Nvidia ($NVDA) and Micron ($MU), 2026 S&P EPS growth falls to under +10%:

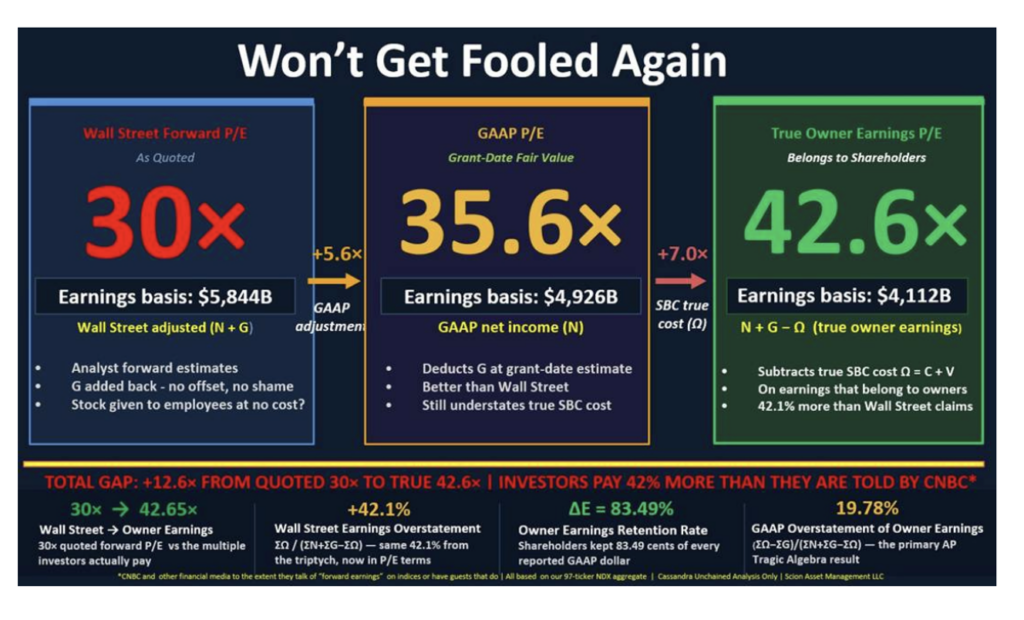

Almost no tech stock, not even the bombed-out software stocks, are inexpensive when held to strict accounting standards, more strict and more forensic in nature than GAAP.

Michael Burry hits the target in his recent commentary:

The NASDAQ 100’s true PE is closer to 43x than the 30x Wall Street tells us.

In addition to the effects of stock-based compensation, previously discussed problems with depreciation policies, construction-in-progress, M&A costs, capital leases, and other necessary adjustments to GAAP net income to find true owners’ earnings.

Including all these adjustments, Wall Street may be overstating by more than 50% the earnings at our fastest growing, most highly valued companies.

In addition, there is the likelihood of future write-downs, in large measure stemming from the numerous circular financings. (Cisco in 2021 and 2002 wrote down years of its best earnings when it had to write off the same types of contracts with its suppliers).

Most investors are now convinced we are in a continued bull market led by AI-related equities.

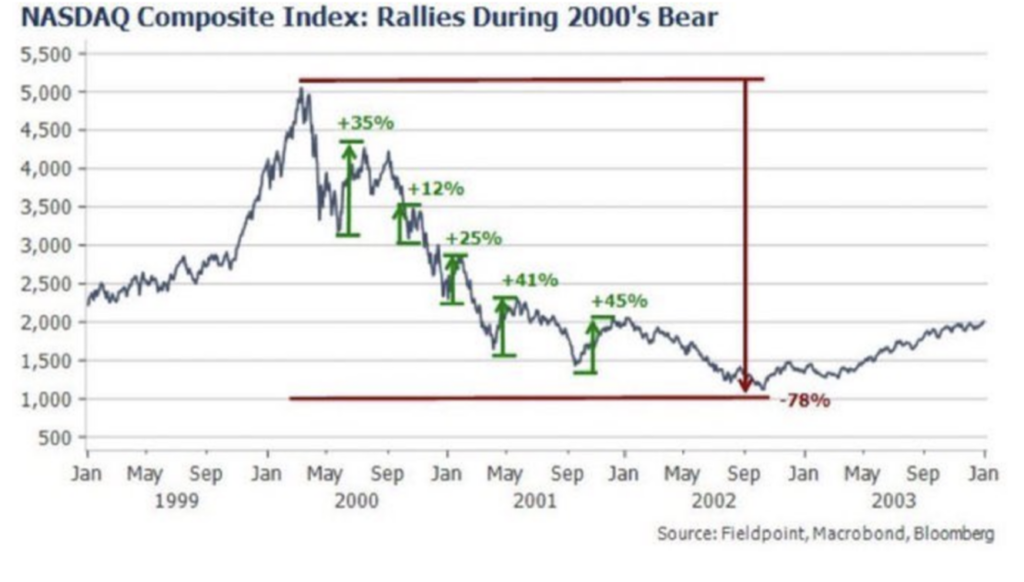

However, the anatomy of a bear market (we will not know until after the fact!) is that there are violent rallies.

As noted earlier, a classic and extreme example was when the Nasdaq declined by -81% (2000-2002) following the dot-com boom in which the revolutionary impact of the internet was heralded and applauded in the indexes.

Along the way to the nearly 80% drop, there were five robust rallies of between +12% and +45%. The average gain in the rallies was +33%.

Every rally felt like a bottom, but every rally was a trap:

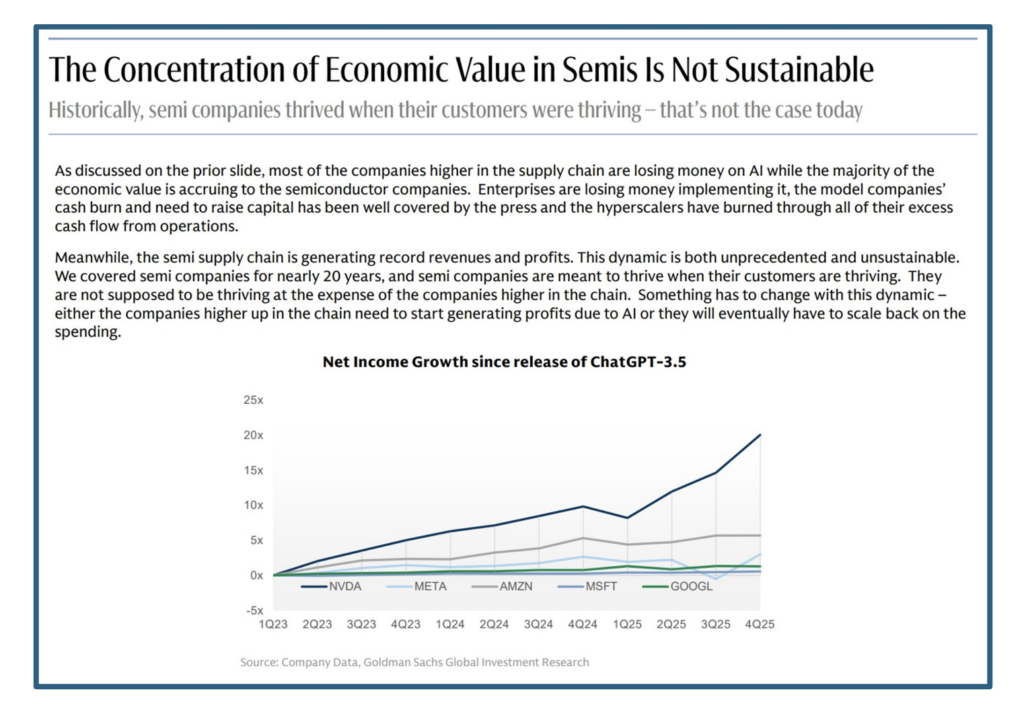

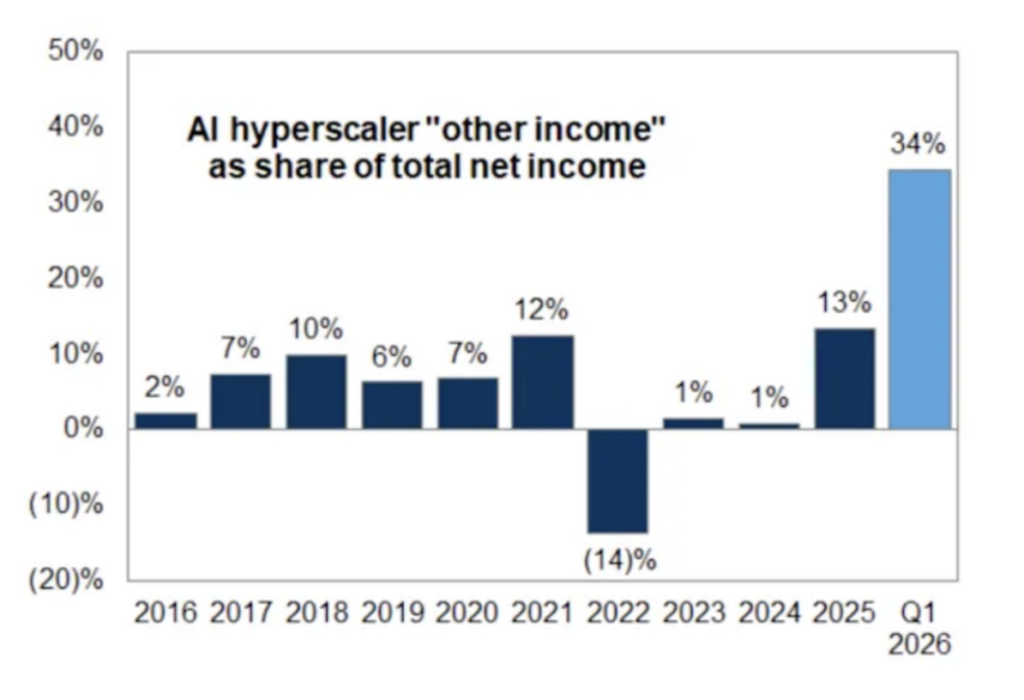

I see multiple traps ahead, including financing circularity and quality of earnings (the other income line has been aided by sizeable increases in private investment valuation marks – below), among other issues (like the large erosion in hyperscaler free cash flow):

Stay tuned for Part 4…