That Dividend Check May Be Costing More Than It Pays

A dividend-heavy portfolio keeps paying even in a prolonged downturn; that’s a pretty important aspect of generating cash for retirement.

That means there’s no need to sell shares of dividend payers when you need cash, or at least it means you can plan for that contingency.

But cash flow and math aren’t the same thing. A portfolio that keeps paying doesn’t necessarily keep growing, and retirees who optimize for the monthly check often do it at the expense of what’s underneath it. They’re eroding principal slowly enough that the damage may not show up until it’s too late to fix.

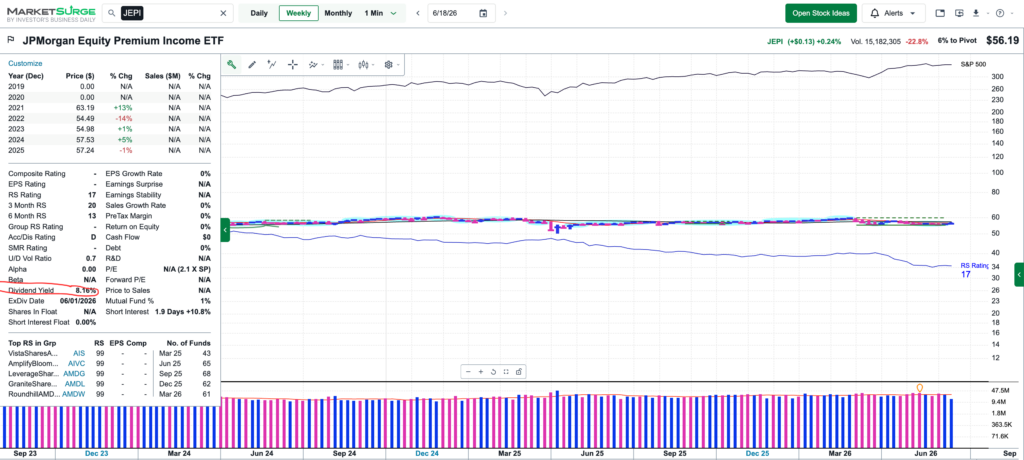

The clearest example is the covered-call ETF category, represented by ETFs like the JPMorgan Equity Premium Income ETF ($JEPI).

The Tradeoff

JEPI and similar funds have been heavily marketed to retirees. The mechanism is pretty easy to understand: The fund holds stocks, sells call options against them and pays the premium out as income.

In exchange, it gives up much of the stock’s upside if it rallies past the strike price.

For example, JEPI illustrates the gap well. Its monthly payouts have ranged from about 34 or 35 cents per share in 2026, supporting a yield around 7% to 8%. Yield currently stands a little above 8%.

But as this chart shows, the flip side of that income is a ceiling on gains.

During the 2023 and 2024 equity rally, JEPI’s covered-call strategy capped its upside while the S&P 500 surged; investors collected distributions but gave up a meaningful portion of the price appreciation an uncapped index fund would have delivered.

Another Fund Comparison

Now let’s look at the Global X Nasdaq 100 Covered Call ETF ($QYLD), comparing it to the Schwab U.S. Dividend Equity ETF ($SCHD).

Over the past decade, QYLD returned about 9.84%, while SCHD returned about 12.59%, with an expense ratio one-tenth of QYLD’s.

Here’s the total return chart comparing SCHD, in black, with QYLD, in yellow.

So the lesson here is: Besides looking at what kind of income a fund generates today, also consider what kind of growth you need over the next 10 or 15 years. QYLD maximizes the current check at the expense of growth; SCHD trades a smaller check now for one that tends to grow.

Neither approach is wrong, but the point is that you need both.

Also: You probably don’t need those two specific funds. This is just for illustration purposes.

The ‘Homemade Dividend’

Selling a small slice of a total-return portfolio each year, say around 4%, can serve the same spending function as receiving dividends, while giving investors more control over the amount withdrawn and the timing of taxable gains.

For example, to generate $24,000 a year, a portfolio yielding 3.5% requires about $686,000; one yielding 7% requires about $343,000.

But don’t get carried away with thinking that juicing up the yield will solve your problems if you don’t have much saved: Higher yields usually come with their own trade-offs, which include less exposure to faster-growing areas of the market as well as much higher risk.

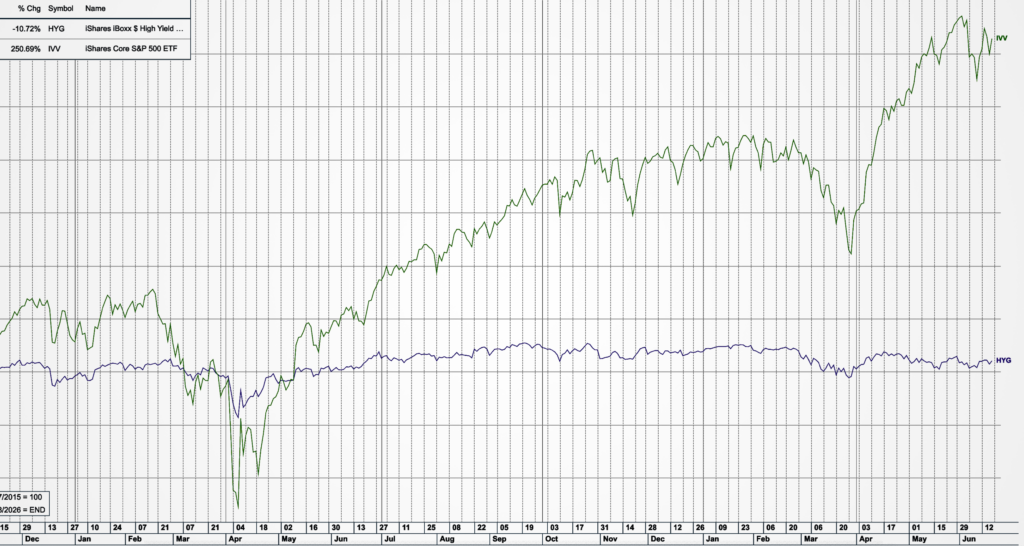

Over the past year and past decade, broad growth-oriented indexes have dramatically outperformed many high-yield strategies. For example, here is how the iShares Core S&P 500 ETF ($IVV) stacked up against the iShares iBoxx $ High Yield Corporate Bond ETF ($HYG) over the past decade.

That growth potential is often what investors give up in exchange for a larger immediate income stream.

Income Is a Tool, Not a Strategy

The monthly check is real, and for many retirees it genuinely helps and is a necessity.

But it’s not free. Every dollar of yield that comes at the expense of growth is a dollar that isn’t compounding, and the cost of that tradeoff tends to be invisible until years have passed.

If you’re building a retirement portfolio, start with what you need to spend, then work backward to figure out how to generate it, not the other way around. A portfolio engineered around the check can leave you with a shrinking base at exactly the moment you can least afford it.