Sticking With This Intel Price Target as Trump, Apple Update Prove Us Right

As the president sends shares on the move, we’re revisiting our target price for the foundry name.

As the president sends shares on the move, we’re revisiting our target price for the foundry name.

Here are today’s things:

* Re-shorted $SPY at $746.68 and $QQQ at $736.53.

* Re-shorted $GRNY at $27.49 and JOET at $45.57.

* Added to cannabis longs: $MSOS ($4.69), $MSOX (new position) and GTBIF ($7.49).

* Shorted more $MS at $228.47.

Position: Long GTBIF (S), MSOS (VL), MSOX (VS); Short SPY (S), QQQ (S), GRNY (VS), JOET (VS), MS.

The stock remains in a range after a couple of violent moves.

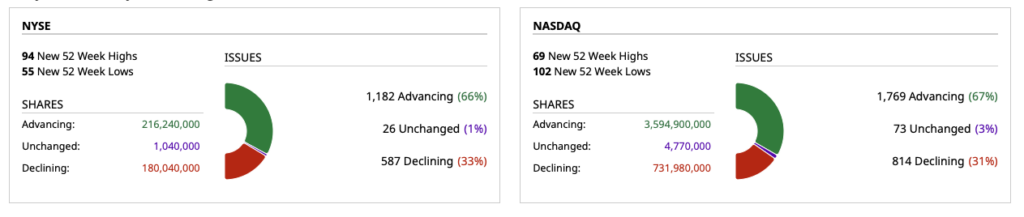

– NYSE volume 154% above its one-month average;

– Nasdq volume 105% above its one-month average;

– VIX index: down 7.75% to 17.01

Positions: None.

I added to index shorts as the market makes a high for the day:

* $SPY $746.83

* $QQQ $738.73

Proximate reasons: extended memory stocks (moving to Ludacris Speed!) and the outside day to the downside in JPMorgan ($JPM).

Position: Short SPY (S), QQQ (S)

I have a research call at 11 am.

Back before noon.

Positions: None.

How can I not like the looks of the company?

From Peter Boockvar:

I think Kevin Warsh did a great job laying out his thoughts. Not where he thinks monetary policy goes from here but how he will approach the incoming data and the ‘task forces’ he wants to create to help get outside opinions on crucial things, like how to manage their balance sheet from here. That said, he has half his colleagues that expect rates to rise this year and that is something he has to balance with whatever he might think should happen from here, which he of course did not reveal to us other than emphasizing “This committee will deliver price stability.”

Also, I can only imagine how many memes are going to be created on ‘task forces.’

With a heads up from my friend George Goncalves, head of US macro strategy at MUFG, yesterday was the worst day for the US 2 yr Treasury on a Fed meeting day, with the yield up 13 bps, since the March 2008 meeting when it jumped by 26 bps. That day the Fed actually cut rates by 75 bps in response to the Bear Stearns bailout by JP Morgan but was widely anticipated and reversed the decline in the two prior days.

As of this writing, according to the fed funds futures, the rate hike odds are now 100% for one increase by year end with a 50% chance of a second. That first hike is fully priced in for the October 27-28 meeting.

Having nothing to do with supply disruptions from the Middle East, we and the FOMC were reminded again that at least for now, the Gen AI data center buildout is inflationary after the WSJ reported yesterday that “Apple to Raise Prices Due to Memory Chip Crunch, Tim Cook says.” Tim Cook said in the article, “Unfortunately, price increases are unavoidable. We’re doing our best to mitigate the huge increases that are being passed to us, and we’ve been trying to shield our customers from the increases, but the situation has become unsustainable.”

The writer then said, “Cook declined to offer details on the timing or scale of the planned price increases, nor which products would be affected. Apple’s next major product launch is likely to be in September when it releases the iPhone 18 lineup, expected to include a new foldable iPhone. Price increases, especially for Macs and iPads, could come sooner. Apple raised the starting price of the Mac Mini last month in between launch events.”

Remember that Apple reported a 48% gross margin in Q1, a record high so they are certainly trying to defend that level and we’ll see to what extent they can. From a valuation perspective, the stock now trades at just under 10x sales, around a record high.

https://www.wsj.com/tech/apple-price-increases-memory-supply-199845b1

Other central banks met today and as expected we got no changes from the Swiss National Bank (zero rates), the Norges Bank (4.25%) and the BoE (3.75%). In Asia, Bank Indonesia hiked again by 25 bps to 5.75% while in Taiwan, their benchmark rate held at 2.0%.

More on the Bank of England, 2 members wanted to hike rates while 7 voted to keep them unchanged. In their statement they said “The impact of the energy shock on the UK economy remains uncertain. Monetary policy cannot influence energy prices but is being set to ensure that the economic adjustment to them occurs in a way that achieves the 2% inflation target sustainably.”

The 2 yr gilt yield is higher by 6 bps today, following what went on in the US, but is coming off its highs of the day by 2 bps as it seems that the BoE is on hold for a bit. The pound is at the lows of the day post statement.

Also out of the UK, employment in May rose 2k, which was much better than the feared loss of 25k and April was revised up to a loss of 53k from the initial print of down 100k.

CarMax stock fell 9% yesterday as comps were down .8% y/o/y and gross profit per unit was lower too and this is what they said of note on their call:

“we feel really good about how we are viewing the consumer that’s on our books, our receivable base, how we have reserved…This is our third quarter in a row where we really kind of hit the losses as expected. The consumer, overall, I think you can see in the industry they are continuing to be pressured by overall inflation.”

“If you look at delinquency rates among credit cards, auto, all of that, it is higher, but again, we feel like we have an excellent handle on that, and that’s captured.”