May ISM and ADP Data Should Keep the Fed’s Focus on Inflation

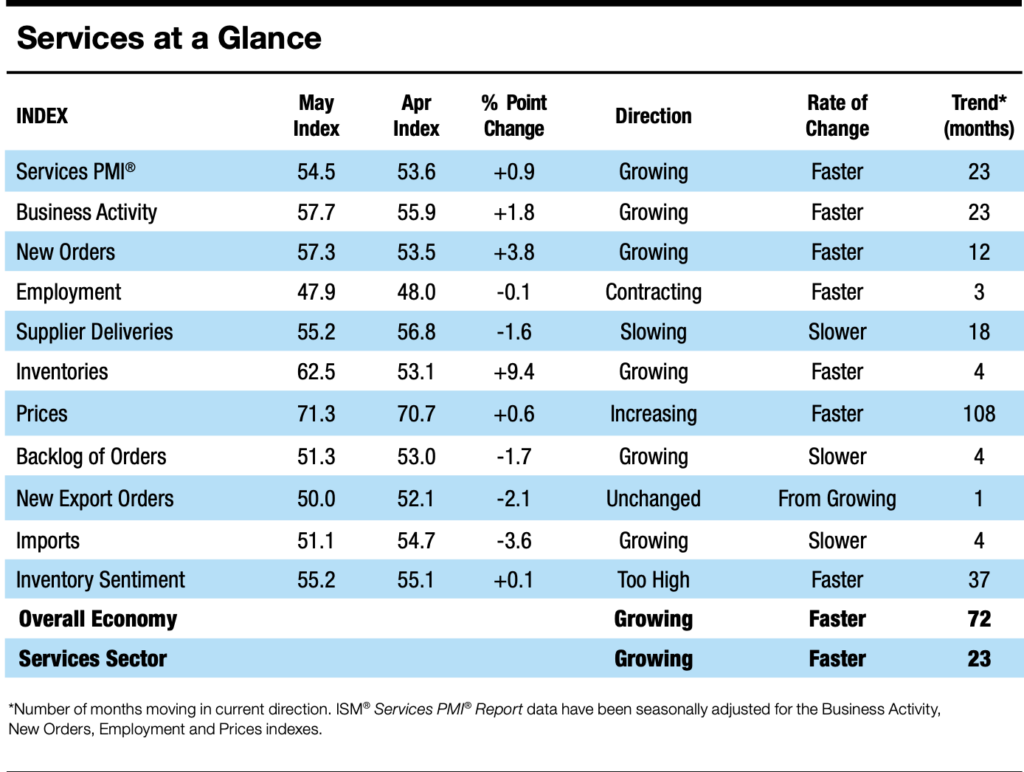

The ISM Services PMI report for May is out, and it showed a pickup in activity for that part of the U.S. economy, with stronger new orders suggesting further gains ahead.

Employment in the Services sector continued in May at a modestly faster pace compared to April. On the inflation front, another step up was recorded for the Services sector, marking the third consecutive month above 70.

S&P Global’s Services PMI, also out this morning, found inflation pressures rose further in May as well:

On the price front, cost pressures remained historically elevated, driven principally by rising fuel and energy prices. The pace of inflation was at a five-month high and pushed services companies to raise their own selling prices at a slightly faster rate.

Cost pressures reportedly stemmed from rising fuel, energy and supplier prices, and pushed overall input costs up to the fastest degree in 2026 so far. Higher labor costs and tariffs also added to upward pressure on company operating expenses.

In line with the trend for overall costs, selling prices increased to a greater extent than in April with inflation comfortably above its long-run average. Firms often sought to pass higher input costs onto clients, although a stronger increase was limited by reports of competitive pressures.

Paired with the elevated figures for ISM’s Manufacturing PMI, we should see another rise in May headline PPI next week compared to April’s 6.0% year-over-year increase and the 4.3% advance for April. Given the lead time between PPI and CPI, the uptrend in the PPI data that began in February and has since accelerated is bound to flow through to CPI data.

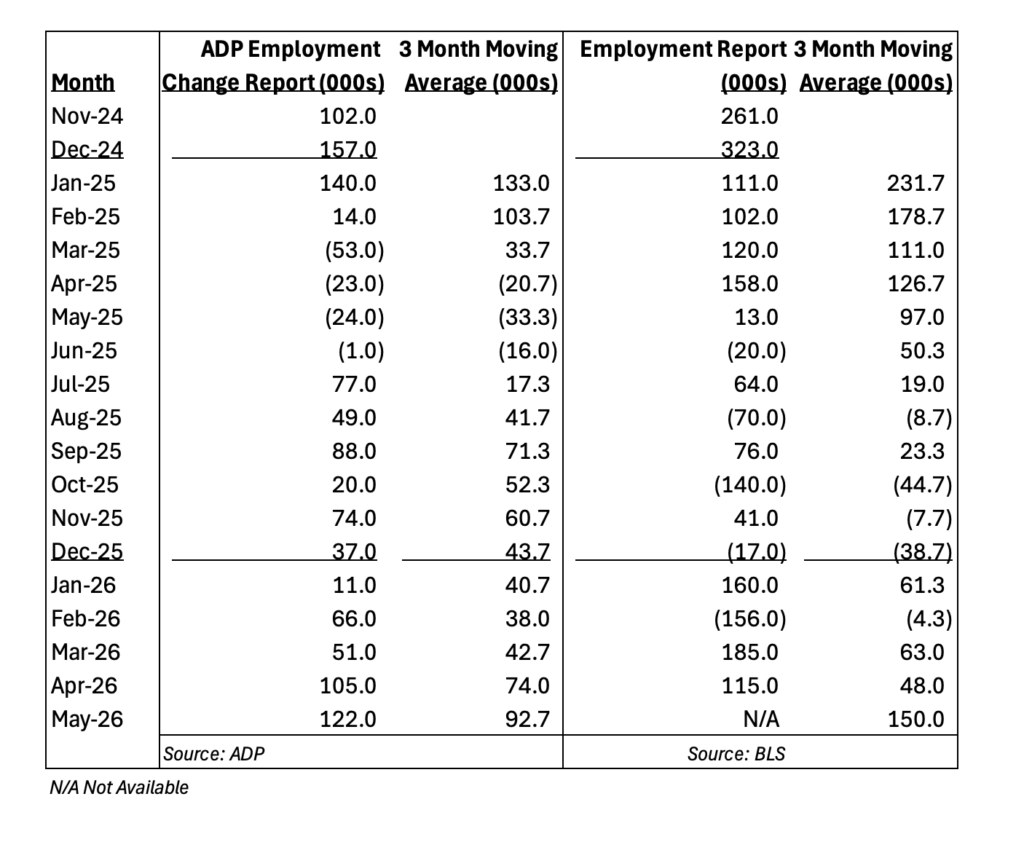

ADP’s May Jobs Figure Tops Expectations

This morning’s ADP Employment Change report found 122,000 jobs were added during May, marking the greatest number of jobs created since January 2025. As we can see below, the three-month moving average also hit its highest level since February 2025.

While not the robust level of job creation seen in 2022 and 2023, ADP’s figures point to a pickup in job creation in the last few months. That should mean the Fed’s focus will be more on renewed inflation pressures reflected in the May ISM reports for both Manufacturing and Services, barring a horrible May Employment Report on Friday.