Kass: The Voting Machine Is Overwhelming the Weighing Machine

For nearly three years the markets and its participants have ignored elevated valuations.

How much longer can the S&P 500 and the other major indices deliver upside when price-earnings multiples and equity risk premiums are in the 95th percentile or higher?

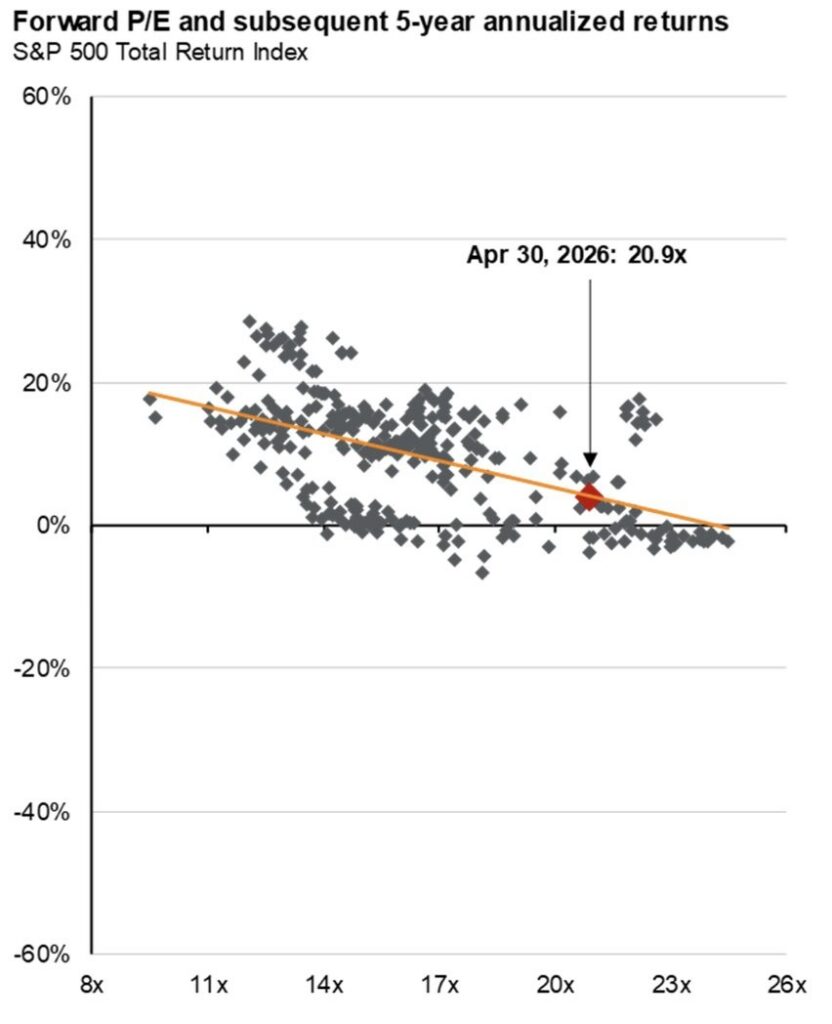

With consensus (I think overly optimistic!) 2026 S&P EPS at $330/share, the senior average trades at 23x and the equity risk premium is negative.

On projected 2027 S&P EPS consensus of $375/share (I think overly optimistic as well) the S&P trades at 20.5x and the equity risk premium is only at 50 basis points, both in the 93rd percentile.

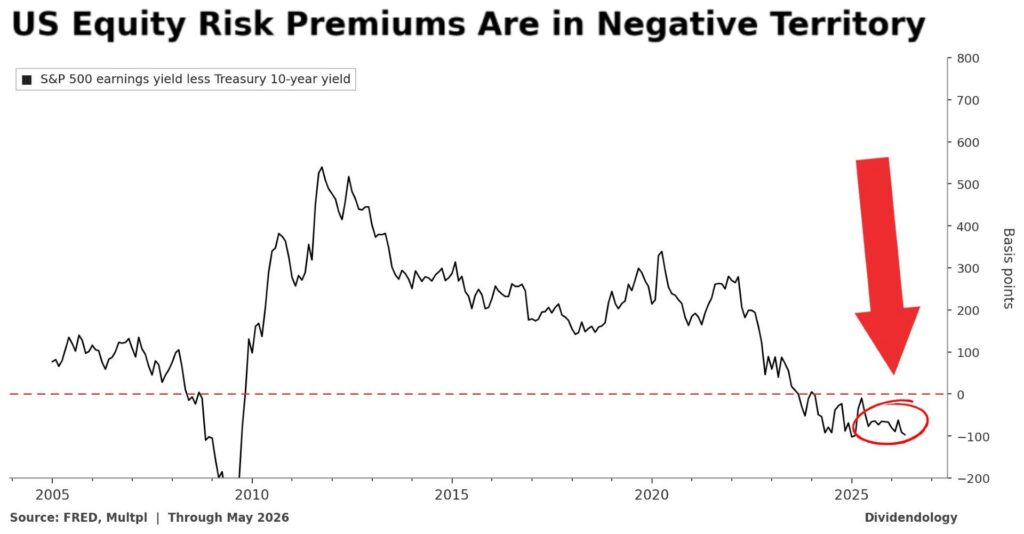

The steady decline in the equity risk premium is a metric I pay very close because. Historically, it has been an excellent indicator future investment returns…

My focus on the ERP has contributed importantly to my wrong-footed market view and a missed opportunity set on the long side.

The Equity Risk Premium

Let’s examine the equity risk premium, which is the difference between the S&P earnings yield (the inverse of the P/E ratio) and the risk-free rate (the 10-year Treasury note yield is typically used):

The equity risk premium tells us how much excess return investors are being paid to own stocks over a risk free Treasury bond.

Historically, equities typically offer a three-to-four percent premium over Treasuries. Such a premium makes sense because it compensates investors for volatility, drawdowns and uncertainty.

Right now, according to the chart above, the investor is being paid negative in equities vis a vis bonds. The ratio is saying that holding bonds is more risky than owning stocks — this is a radical notion, at an extreme! Again, this means:

1. Investors are not being paid extra to take on risk in stocks.

2. Stocks are offering similar or worse “yield” than bonds.

3. Valuations are materially stretched relative to interest rates.

Stated simply, this means that holders of equities are taking more risk for less reward (than bonds). When this has happened in the past (most notably during the dot-com bubble and leading up to The Great Recession in 2007-09), forward returns have been somewhere between non-existent and negative:

Bottom Line

It is hard to understand why stocks have been impervious to elevated valuations (a record high in overvaluation in both the Buffett Indicator and a near record in Shiller’s CAPE ratio), as well as an equity risk discount.

One answer is the dominance of passive products and strategies that worship at the altar of price. They know everything about price and nothing about value.

Other explanations are the euphoria in AI and the fear of missing out (FOMO).

Nonetheless, excessive valuations, excesses and the idea of a “new era” are nothing new — we have seen these at the top of other cycles (for reasons of overenthusiasm/heated speculation).

Finally, it is our strong view that the components of the equity risk premium suggest even more of a discount as 2027 EPS estimates come down and interest rates likely rise.

Let’s not forget when Berkshire Hathaway’s (BRK.A) (BRK.B) shares were suffering in late 1999 and many were questioning Warren Buffett’s investing philosophy (as they are currently with his near $400 billion cash hoard) — right before a more than -80% drawdown in the Nasdaq.

To me, it’s not different this time.

I continue to choose the weighing machine over the voting machine.

This commentary was orginally posted in Doug’s Daily Diary on TheStreet Pro.

At the time of publication, Kass had no positions in any securities mentioned.