Peace Sells … And the Markets Are Buying It

A deal? This time, the news appears to have a lot more substance to it than it has in the recent past. At least financial markets seem to be buying it. What happened? In posts to social media, U.S. Pres. Donald Trump informed that some time was needed “for the purpose of mine removal,” but also that Iranian restrictions on maritime transit through the Strait of Hormuz and the U.S. naval blockade would come to a simultaneous and immediate halt. The president stated that “The Deal with the Islamic Republic of Iran is now complete.” For a welcome change from the recent past, this sentiment was echoed from all sides.

Iranian deputy foreign minister, Kazem Gharibabadi confirmed, “The text of the memorandum of understanding has been finalized.” Pakistani Prime Minister Shehbaz Sharif, who had acted as a mediator, stated, “Following intensive talks, we are pleased to announce that the Peace Deal between the United States of America and Islamic Republic of Iran has been REACHED. Both sides have declared the immediate and permanent termination of military operations on all fronts, including Lebanon.” The deal was also confirmed by representatives of Qatar, a nation that had also contributed to the mediation.

What’s Inside?

Good question. Details have so far been scant. There are competing drafts that have been released by various sources that may or may not have nuggets of truth inside. Most of these drafts do have some commonalities.

It is believed that under the deal agreed to, that there will be a signing ceremony attended to by all sides this Friday in Switzerland. The deal will also include both Israel and Hezbollah who had been actively warring as recently as Sunday morning.

It is believed that for at least 60 days, that both Iran and the U.S. Navy will allow free passage through the Strait of Hormuz. and access to Iranian ports. Iran will reaffirm its commitment to not procure or develop nuclear weapons. Further negotiations will be required in regard to how Iran’s stockpile of enriched uranium will either be disposed of or downblended.

The minimum agreement across all drafts requires all uranium to be diluted under the supervision of the International Atomic Energy Agency and some sanctions relief for Iran once evidence of that nation’s commitment to the peace process is evident.

Market Reaction

Financial markets appear to be exuberant of the reaching of this deal by all sides. Japanese and South Korean equities rallied a rough 5% on Monday. Chinese stocks were up more than 1.5%. As this article went to print, stock markets across Europe were opening in the green as well. Overnight, WTI Crude is trading with an $80 handle (-5.5%) while Brent Crude is trading with an $82 handle (-5.2%).

U.S. Treasury debt securities are rallying across the yield curve as well as the re-opening of maritime transit through that region of the world can be expected to bring significant relief to those suffering from upward global inflationary pressures. S&P futures are trading a rough 1% higher overnight as well, as Nasdaq futures are trading more than 2% higher.

It Was a Hard Thing to Undo This Knot

See one bow each, yet not the same to all,

But each a hand’s breadth further than the next.

The sun on falling waters writes the text

Which yet is in the eye or in the thought.

It was a hard thing to undo this knot.

-Gerard Manley Hopkins (1864)

Week Ahead

What matters moving forward as markets respond to a rapidly evolving news cycle. Keep in mind, financial markets will be closed this Friday for the federal Juneteenth holiday.

- The Geopolitical… As the U.S. and its allies and Iran and its proxies appear to have agreed to a potentially lasting peace deal, it stands to reason that energy prices will fall precipitously and that consumer level inflation will slow sharply. There certainly is good reason for optimism on this front for the first time in a couple of months.

- Macro… The macroeconomic focus this week will be on May retail sales this Wednesday morning and to a lesser degree, May Industrial Production this morning. In addition, investors and traders will be watching for May Housing Starts on Tuesday morning and the results of regional manufacturing sector surveys to be published by the New York and Philadelphia Feds on Monday and Thursday respectively.

- The Federal Reserve… The Fed will come out of its eight times a year media “blackout period” this Wednesday afternoon with the publication of the Federal Open Market Committee’s first official policy statement under the leadership of Kevin Warsh. Along with the release, the FOMC will release their updated quarterly economic projections. A half hour after those releases, Warsh will hold his first press conference as Fed Chair.

- Earnings… Second-quarter earnings season will not begin in earnest until mid-July. All we have now are the few publicly traded firms that report out of season. Making this week even lighter in this regard will be the market holiday on Friday. There are no headline level names reporting. That said, this afternoon, we’ll hear from Dave & Buster’s ($PLAY). Tomorrow afternoon, La-Z-Boy ($LZB) will post their quarterly results. On Wednesday and Friday, CarMax ($KMX), Jabil ($JBL) and Kroger ($KR) will all step to the plate.

The Week That Was…

The S&P 500 posted a tenth winning week in the past eleven. This is how it went…

- The S&P 500 gained 0.5% on Friday and 0.65% for the week.

- The Nasdaq Composite added 0.31% on Friday and 0.7% for the week.

- The Nasdaq 100 rallied 0.64% on Friday and a nice 2.34% for the week.

- The Russell 2000 gained 0.79% on Friday and an impressive 3.9% on the week.

- The S&P Small Cap 600 ran 0.91% on Friday and soared 4.29% for the week.

- The S&P Midcap 400 gained 0.71% on Friday and 2.78% for the week.

- The Dow Transports tacked on 0.32% on Friday and 3.12% for the week.

- The Philly Semis popped for 1.52% on Friday to scream 9.42% higher for the week.

- The KBW Bank Index rallied 1.71% on Friday and 3.4% for the week. On Friday, nine of the 11 S&P sector SPDR ETFs closed out the session in the green. The materials ($XLB) and the financials ($XLF) easily led markets higher. Communication services ($XLC) led the losers.

For the week, as for the day. nine of the 11 S&P sector SPDR ETFs finished in the green. Materials were again the leader, followed by the staples ($XLP) and by tech ($XLK). Energy rose out the week in last place.

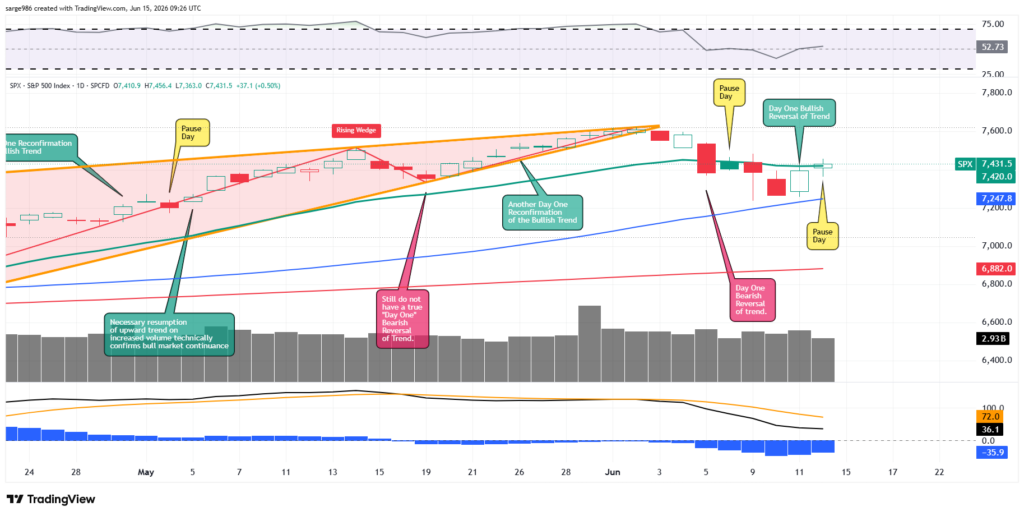

The Chart

Readers will see that though Friday was an overall positive day that due to lower trading volume and sloppy breadth will go down as a necessary “pause day.” The pause is required in order to post a “Day of Bullish Trend Confirmation” which could come as soon as today as long as markets continue to buy the “peace deal” story.

For the S&P 500, relative strength has returned to better than neutral levels, but the daily moving average convergence divergence still needs some work in order to leave its bearish posture behind. Last week, the S&P 500 found support at its 50-day simple moving average as professional money defended the market against an attempted bearish shift in trend. Swing traders appeared to battle around the 21-day exponential moving average for that index on Friday without a conclusive outcome. That should, one would think, change for the better in a few hours.

Earnings

As of June 12, according to FactSet, for the second quarter, Wall Street now expects to see year-over-year earnings growth for the S&P 500 of 21.9%, up from 21.7% last week. Wall Street also sees revenue growth of 12%, up from 11.2% one week ago. For the second quarter, 47 S&P 500 companies have issued negative earnings guidance while 62 have issued positive guidance.

For the full year of 2026, Wall Street now looks for earnings growth of 23.2%, up from 22.8% last week, and up from 14.7% more than two months ago. This would come on revenue growth of 11%, up from 10.8% last week and up from 7.7% a rough ten-plus weeks ago. The outlook for the third quarter is also very positive. Third quarter S&P 500 earnings growth is now estimated at 25.3%, year over year.

At the moment, the energy and technology sectors are projected to have grown Q2 earnings an absolutely jaw-dropping 121.9% and 59% respectively. Just one sector, health care (at -5.1%) is currently projected to have suffered a Q2 earnings contraction.

Valuation

Still using data provided by FactSet, the S&P 500 ended last week trading at 20.1 times twelve months’ forward-looking earnings, down from 21.1 times last week, and down from 21.6 times about ten weeks ago. This is still well above the five-year average of 19.9 times for the index as well as being well above its ten-year average of 19 times.

The S&P 500 also ended last week trading at 27.4-times trailing 12 months’ earnings, down from 28.6 times just one week ago, and also above levels that the index reached more than two months back. This also stands well above the five-year (24.5 times) and 10-year (23.4 times) averages for the index.

Seven of the 11 sectors are now trading at or above their five-year average valuations, led by the discretionaries (25.3 times). Four sectors closed out last week undervalued relative to or even with their five-year norms, up from just two sectors the week prior.

Fed Funds Futures

Fed Funds futures trading in Chicago are currently pricing in a 97% probability for no change to be made to the current target range (3.5% to 3.75) for the Fed Funds Rate at the culmination of the next FOMC policy meeting this Wednesday. That’s down from a 99% likelihood a week ago. There is now a 3% chance for a rate cut priced in. As we know, Kevin Warsh is now running the central bank, and this will be his first FOMC policy meeting as chair. Jerome Powell, however, is still a governor and still has a say. He also probably still has some loyalists as well.

There are no rate cuts fully priced in at any point in the future looking out toward year’s end 2027. That said, there is now a rate hike priced in for January 2027 (59%). That’s been pushed out from a 55% probability for a rate hike as early as September 2026. This possibility for a September rate hike had been visible as recently as Friday.

I Looked at You

I looked at you

You looked me

I smiled at you

You smiled at me

And we’re on our way

No, we can’t turn back

Yeah, we’re on our way

And we can’t turn back

– Morrison, Densmore, Kreiger, Manzarek (The Doors), 1967

Economics (All Times Eastern)

08:30 – Empire State Manufacturing Index (June): Expecting 12.6, Last 19.6.

08:30 – Industrial Production (May): Expecting 0.3% m/m, Last 0.7% m/m.

08:30 – Capacity Utilization (May): Expecting 76.1%, Last 76.1%.

10:00 – NAHB Housing Market Index (June): Expecting 37, Last 37.

The Fed (All Times Eastern)

Fed Blackout Period.

Today’s Earnings Highlights (Consensus EPS Expectations)

After the Close: PLAY (.66)

At the time of publication, Guilfoyle had no position in any security mentioned.