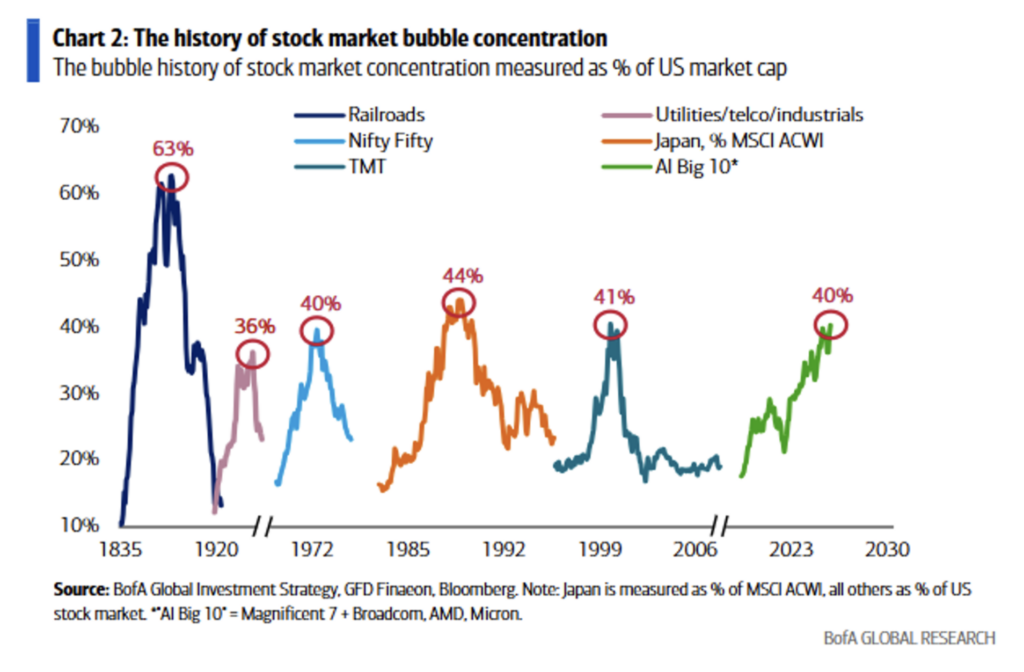

Consider the following price changes in today’s session:

* $SNDK -$201

* $MU -$101

* $AMD -$51

* $MRVL -$38

To me, this should make investors consider whether the market has been nothing more than a casino — in which the many momentum-based investors know everything about price but nothing about value.

And that, as I have observed, the concepts of risk vs. reward and “margin of safety” have been generally ignored.

Payrolls in May rose by 172k, well more than the estimate of up 88k and the two prior months were revised up by a total of 93k. A major factor at play was the 55k person increase in local government hiring. Also helping was the 70k hiring increase in leisure/hospitality vs the average monthly increase of 14k over the prior 12 months. Healthcare, again, the other major contributor, added 35k jobs, about in line with the average of 38k over the prior year.

Elsewhere, the hiring was more mixed. Jobs were lost in retail, financial services and information. Professional/business services, the sector that saw the huge jump in job openings in April, added 6k jobs vs 22k in the month before. On the goods side, manufacturing added 7k people and construction hired a net 17k, both most likely tied to the AI buildout.

The household survey said 149k jobs were new but which follows three months in a row of declines totaling 475k. The labor force grew by 83k and which combined, kept the unemployment rate unchanged at 4.3%. The all in U6 rate at 8.1% was down one tenth m/o/m.

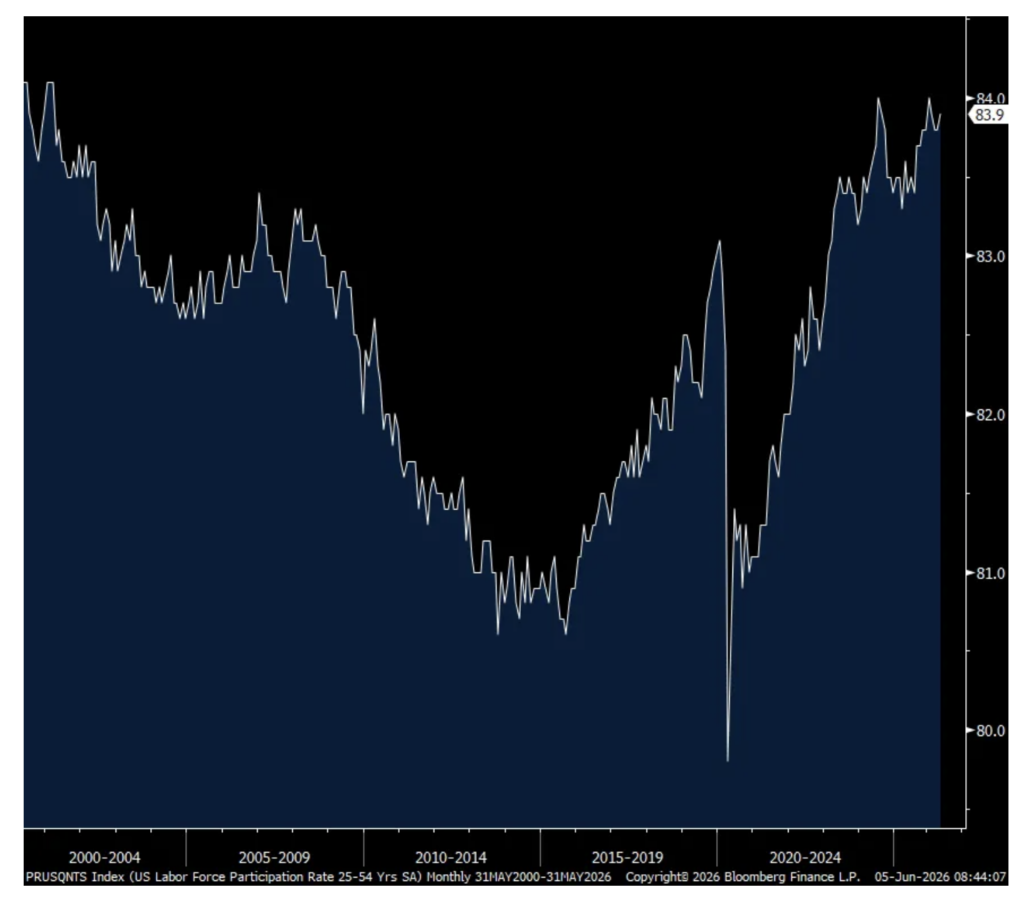

The participation rate held at 61.8%, the lowest since September 2021 but continued to be weighed down by retiring boomers. The participation rate for the 25-54 yr old group rose one tenth to 83.9%, just one tenth below from matching the highest since 2001. Hours worked remained at 34.3 while average hourly earnings grew by .3% m/o/m as expected and by 3.4% y/o/y. Combining the two saw weekly earnings higher by .3% m/o/m and 3.7% y/o/y.

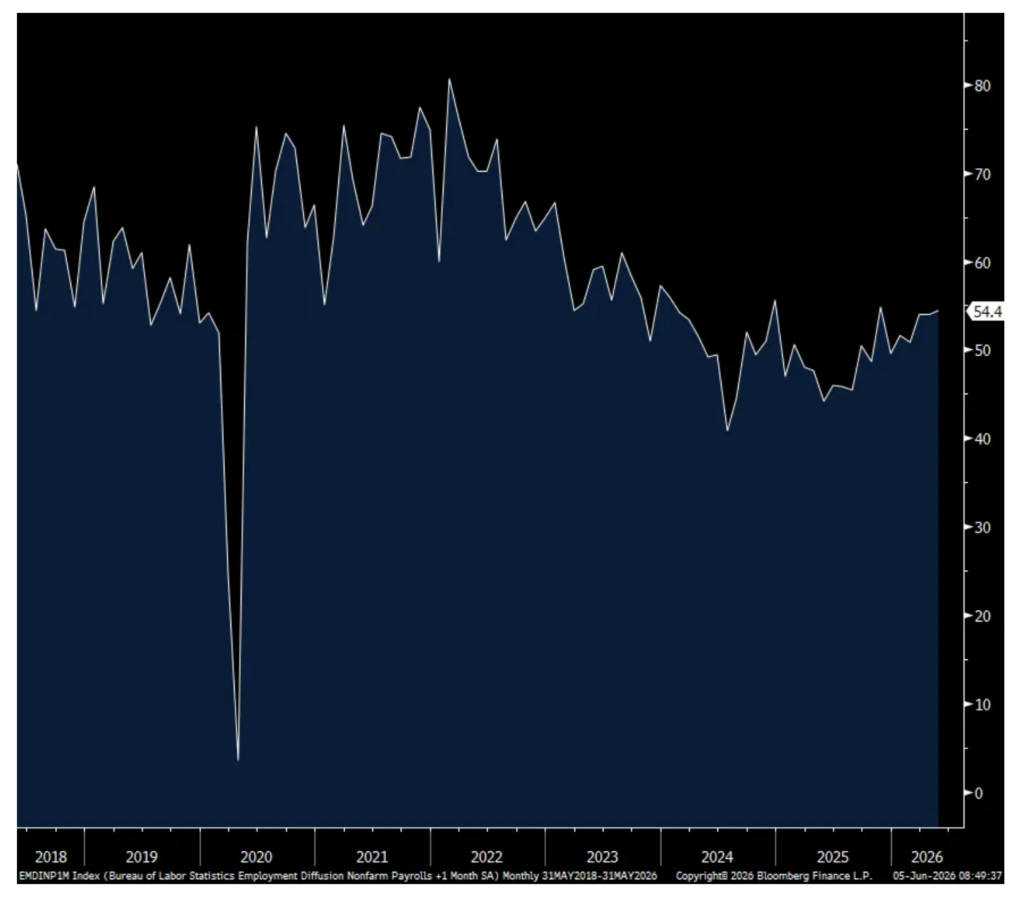

Measuring the breadth of hiring is seen in the diffusion index and it ticked up to 54.4 from 54 and which compares with 54.2 in January 2020. That’s the highest since December 2024.

Bottom line, the data center construction, along with the demand for healthcare workers and leisure/hospitality drove most of the job gains. Because of the local government hiring pop, I’ll do the monthly averages with just the private sector. The 3 month average is 166k vs the 6 month average of 87k and the 12 month average of 56k. Thus, a clear pick up over the past few months and why interest rates are jumping in response with the 10 yr yield back above 4.50% and the 30 yr above 5.00%. The 2 yr yield is having the biggest move, jumping 10 bps to 4.14%. While I don’t think the fed funds futures are that relevant in pricing in rate moves until we hear from Kevin Warsh in a few weeks, it is currently pricing in an 88% chance of one rate hike by yr end.

The US jobs report for May is out, and it includes a big upside surprise on both 1. Job Creation: A significant beat at 172,000 versus the 88,000 consensus forecast (and a "breakeven" rate of ~50,000); and 2. Revisions: The previous two months were revised up by a substantial…

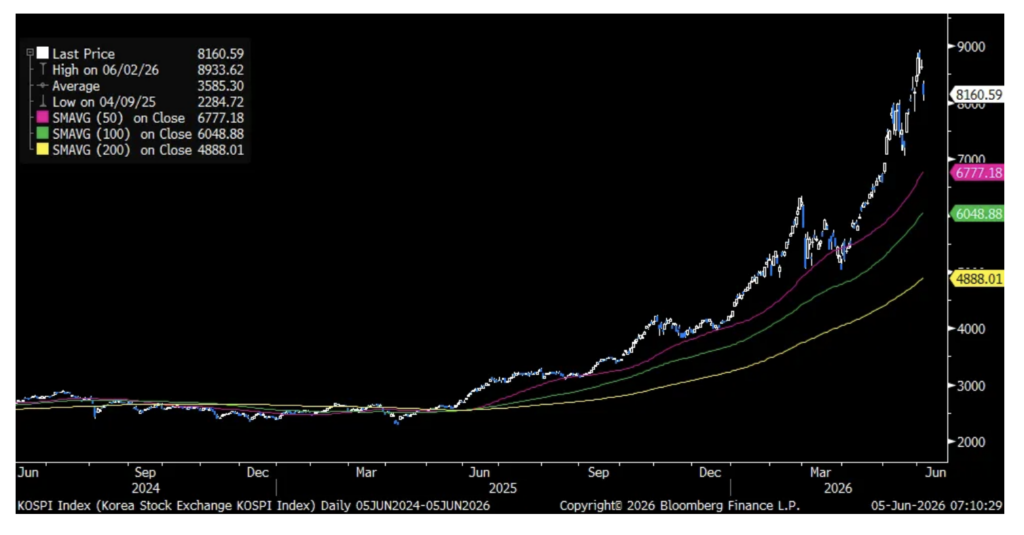

Wake up, check Kospi/Hiring plans falter/Shipping prices up/Platinum/Resilient? It depends

After waking up each day for a while to see first thing what JGB yields were doing overnight, it’s now watching how the South Korean Kospi traded. It fell by 5.5% after falling by 2.8% Thursday but still is up 94% year to date because of Samsung and SK Hynix which dominate the index, as we know.

Kospi

Ahead of today’s May jobs report, the NFIB yesterday released its small business May Plans to Hire in the coming 3 months figure and it unfortunately fell to 9, down 4 pts m/o/m to the lowest level since May 2020 and matching the weakest since August 2014 before that. Also, job openings that could not be filled dropped 5 pts to also the lowest since May 2020 at 29%.

The chief economist at the NFIB said, “Concerns about rising labor costs increased significantly to the highest reading in the survey’s history. Small business owners are facing mounting pressure to retain workers, and many firms are navigating costly new state mandates. While current conditions restrict Main Street’s already thin profit margins, compensation measures remain steady for now.”

Plans to Hire

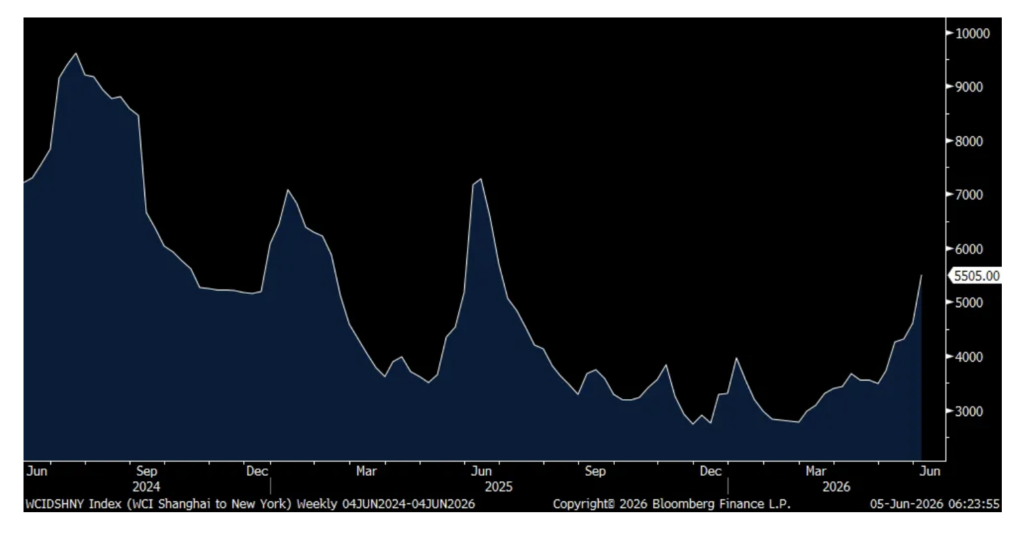

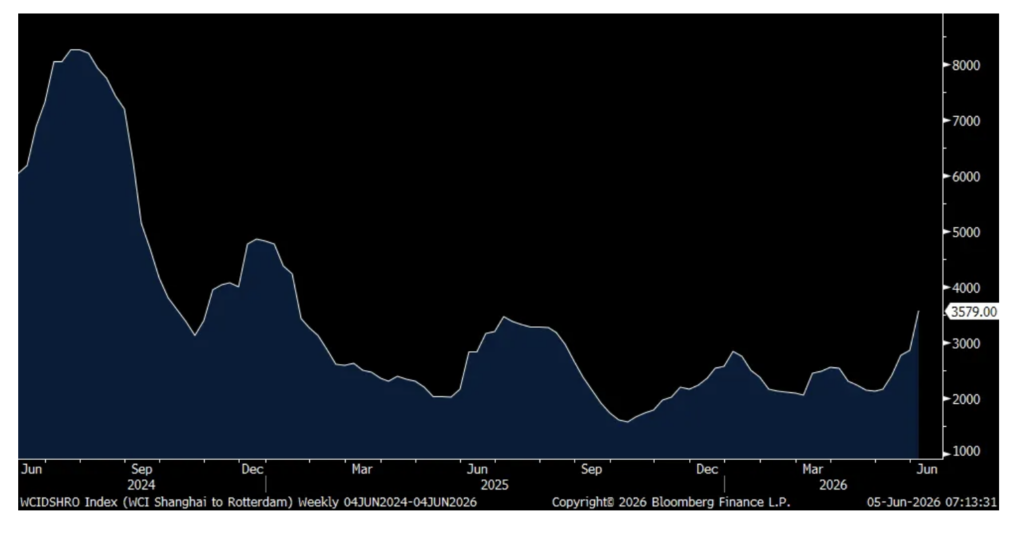

Container shipping prices jumped again according to the World Container Index. The Shanghai to NY route saw prices sharply higher by 20% w/o/w to $5,505, the highest in a year. The Shanghai to LA trip was 31% pricier w/o/w to $4,565, also the highest since June 2025. The price of a container from Shanghai to Rotterdam is the most since January 2025, up 25% w/o/w.

Shanghai to NY

Shanghai to Rotterdam

I’ve expressed my positive stance many times on certain commodities/stocks and want to again mention platinum after the article in the WSJ I read yesterday titled “Sticker shock at the pump fuels a surge in hybrid sales.” The article said “Hybrid cars and trucks are now hotter than ever. Elevated gas prices…helped drive a 33% jump in hybrid sales in May compared with last year, according to data from Motor Intelligence – a bright spot in the otherwise stagnant new-car market.”

Why does this matter for platinum? A hybrid vehicle uses 10-15% more platinum than that used in an internal combustion engine auto. We are long platinum.

Platinum

Something I mentioned a few months ago that the current situation in the Persian Gulf and Hormuz Strait was going to completely alter the logistical waterway to make sure the current situation never happens again. And when done, Iran will lose all its leverage over the Strait of Hormuz. In case you didn’t see this article in the WSJ yesterday titled “The Hormuz squeeze is redrawing the oil map for good.” The piece said, “Across the Gulf, governments are pouring billions into new oil pipelines, rail corridors and energy storage hubs to bypass the waterway in what is set to become one of the most durable outcomes of the conflict. The new energy links are part of a broader redrawing of the region’s logistics map, shifting trade toward trucking, rail and new ports.”

“We saw encouraging signs in Q1 that reinforced we are moving in the right direction, but as we closed Q1 and entered Q2, we faced a few headwinds and a moderating sales trend. Based on our early analysis, there are two key factors impacting our trend. First, we experienced spikes of negative commentary in the media and on social channels with regard to our brand, which had an impact on traffic and overall top-line performance. And second, not all of our product launches have met our expectations.”

Coca Cola’s CFO had some interesting comments at the Deutsche Bank conference yesterday and a stock we own:

“I think the narrative on the consumer being resilient is a nuanced narrative because they’re not all the same. We have segments of our consumer base around the world that are under pressure, and we have a choice to stay relevant with them or not. Longer-term, the equation to have a more active and large consumer base, in our view, is the one that is going to create the most value longer term.”

“we have spoken for a couple of years now, under the general headline of the consumer is resilient, that seems to pop up every quarter, that some of them are not as resilient as you think. And so segmenting populations, whether it’s in the US or whether it’s in China, is a very important capability to build, so that you have the opportunity to evolve your portfolio, to stay relevant with those segments that are under the most pressure.”

“for people earning less than $50,000, $60,000 a year, when you take a step back and look at the cumulative impact of cost pressures on their typical basket of goods and services, the math is pretty obvious, it doesn’t work. They just don’t have the purchasing power to be able to, and so something’s got to go.” And a Coca Cola product they want to be the last to go.

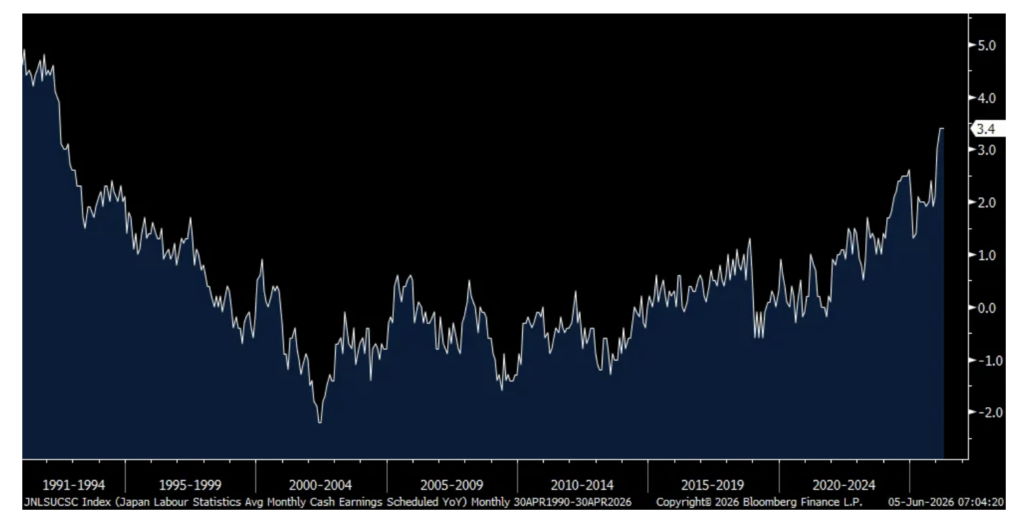

The Bank of Japan got another reason to hike rates after base pay in April rose 3.4% y/o/y for a 3rd straight month, staying at the highest since 1992. Nothing market moving though today as JGB yields and the yen are little changed.