Boockvar on Samsung Earnings, Kospi, Buck, Rents

From Peter Boockvar:

Remember, awake, check Kospi/Cracks/US$, gold, shift continues/Rents/MSC and tungsten

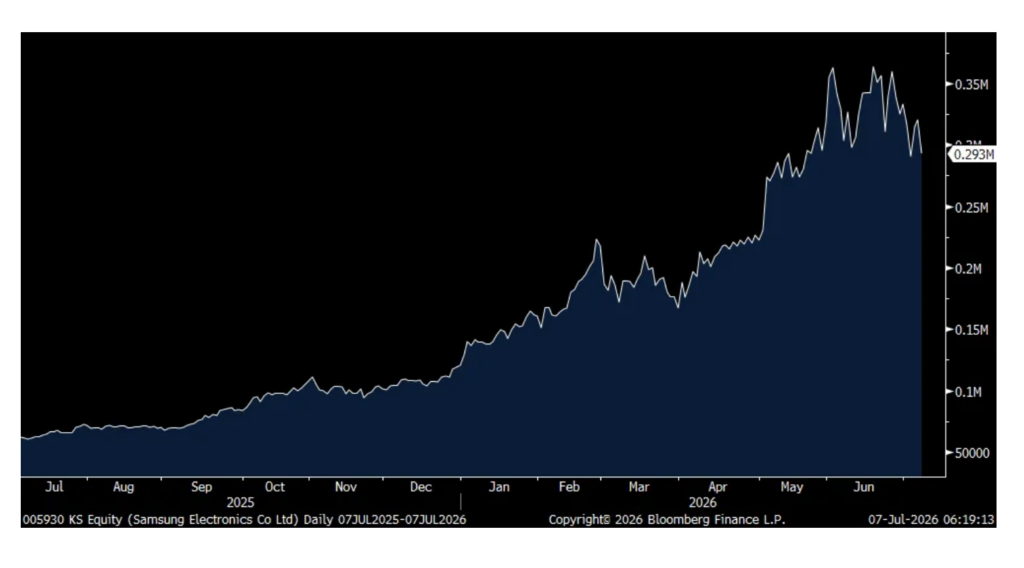

Remember, awake, check Kospi, especially after Samsung reports earnings. Great Samsung earnings, well above expectations, were not great enough as investors question whether this is as good as it gets. The stock fell 8.6% in South Korea. SK Hynix, about to list in NY, was down 7.6%. Kioxia Holdings in Japan dropped 11.3% in sympathy, ASML is down 5% in Europe and Micron is lower by 5% too pre market. The Kospi itself closed down 4.9% but still up 82% ytd.

Samsung

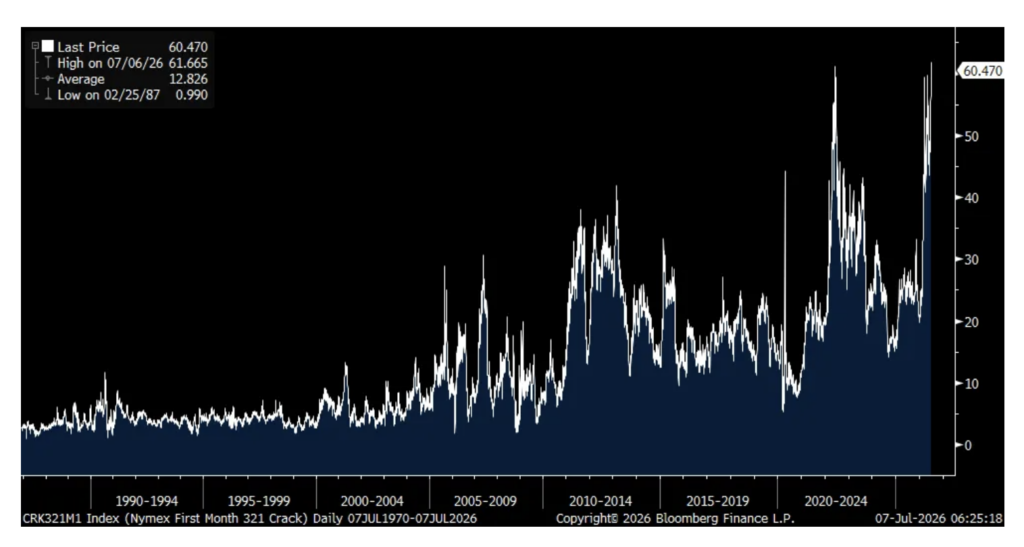

While crude has notably fallen, even with continued strikes in Hormuz Strait and supply nowhere near where it was pre war (we remain long oil/gas stocks), product prices remain elevated and refiners are having an earnings party. My Bloomberg has data on the 321 Crack Spread going back to 1986 and yesterday’s close of $61.67 was a record high, exceeding the previous peak of $60.99 in June 2022. For those unfamiliar, the 321 crack spread is the margin at which a refiner turns three barrels of crude into two barrels of gasoline and one into distillate.

321 Crack Spread

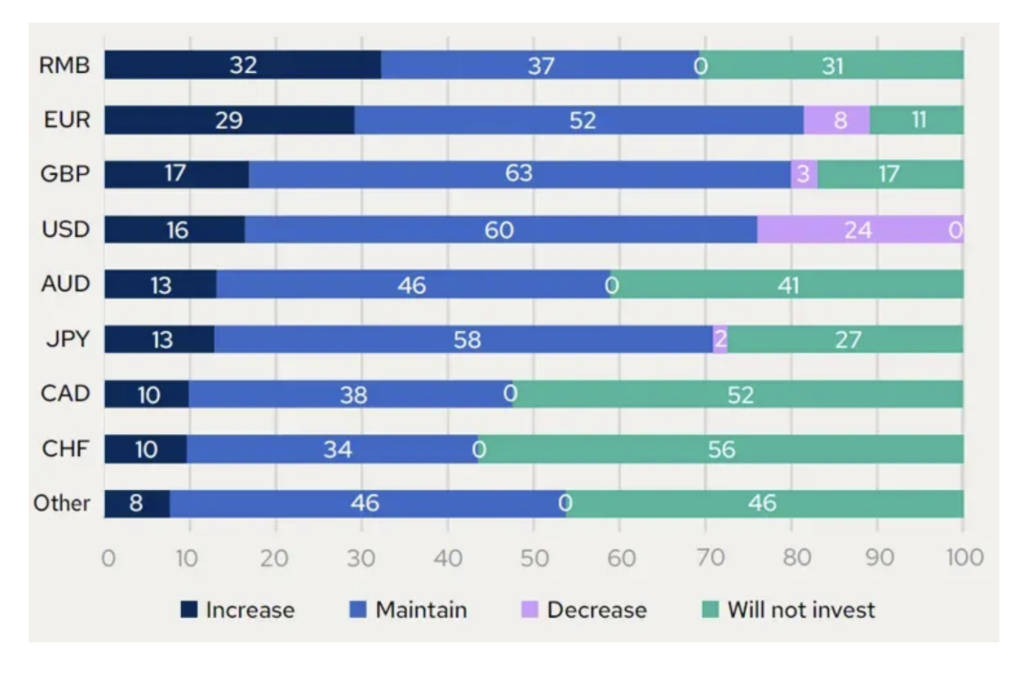

I want to talk US dollar and gold again. We remain long gold, but a bit less so since January with almost no silver with intentions of buying it back at some point. Last month I pointed out the World Gold Council survey of central banks where more planned to diversify their dollar holdings and increase their holdings of gold. This was followed by last week’s release of another survey from the Official Monetary & Financial Institutions Forum. It said this of note:

“The dollar continues to dominate portfolios and is still viewed as unmatched for safety and liquidity. But central banks increasingly expect to reduce dollar allocations over both the short and long term, especially in emerging markets. For the first time since the GPI series (Global Public Investor) began recording reserve managers’ long-term intentions in 2023, more central banks plan to decrease their dollar holdings than increase over the next 10 years. The euro and renminbi remain the main alternatives, while interest in smaller developed and emerging market currencies is rising. This year, 29% of respondents plan to increase euro holdings in the long term, up from 22% last year. However, neither the euro nor the renminbi fully solves reserve managers’ problem: the former lacks a single, deep safe asset market, while the latter remains constrained by market structure and geopolitical concerns.”

“Gold has become the clearest beneficiary of this uncertainty. It leads short-term buying intentions and has moved to the centre of reserve strategies as a hedge against geopolitical risk and concerns about the international monetary system. In 2026, 82% of central banks hold physical gold, up from 71% last year. A net 30% plan to increase their gold allocation over the next one to two years, while 61% expect the price to settle between $5,000 and $6,000 per ounce by June 2027. Only 28% say the current price is discouraging further purchases. The motivation behind gold purchases is increasingly strategic rather than purely financial. Protection against geopolitical risk is cited by 51% of respondents, up 11% from 2024.” I bolded to emphasize.

“Over the next 10 years, do you anticipate increasing, decreasing or maintaining your exposure to the following currencies? Share of respondents, %”

https://www.omfif.org/2026/06/central-banks-are-riding-the-wave-of-persistent-volatility

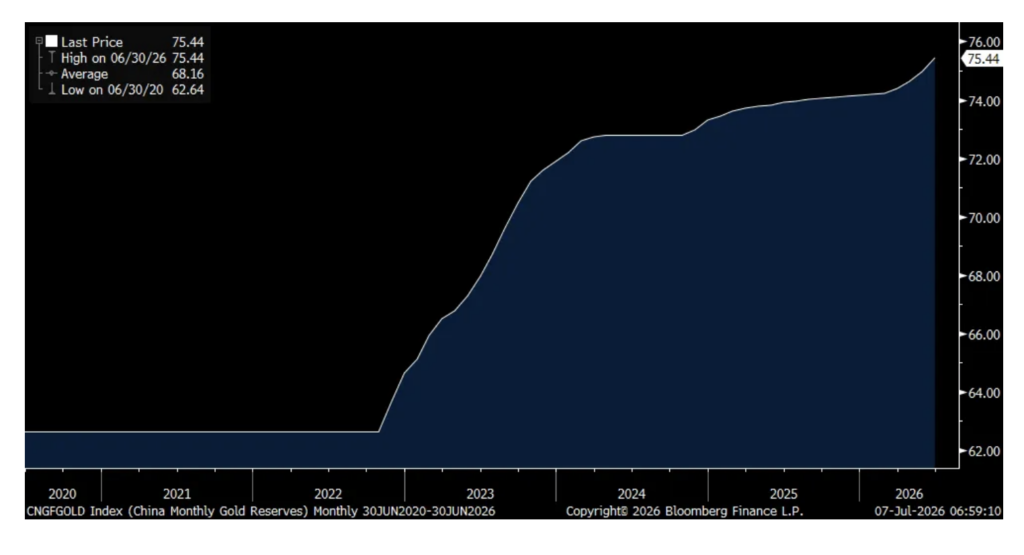

China reported its June reserve data and they keep buying gold. They now hold (that they report) 75.44 million troy ounces, or about 2,350 tons, as they continue to reduce their holdings of US Treasuries.

China Gold Holdings

As an equity owner of an apartment REIT, CPT, and a close watcher of everything macro, I’ve been arguing that in the latter part of 2026, the slowdown in rental growth, mostly seen in Sunbelt states, was going to start to reverse with a resumption of higher prices in 2027 because of a sharp drop in new construction and with still strong absorption rates. This was from the June Apartment List National Rent Report out last week and which measures NEW leases only, not renewals:

“The national median rent increased by .4% in June, and now stands at $1,385. This marks the 5th straight monthly increase, with the market now in the midst of the busy summer moving season.” New rent prices are still down 1.2% y/o/y but “has now ticked up for two straight months, after bottoming out in April at the lowest level that we’ve seen in our estimates going back to 2017.” New rents are off 4% from the peak seen in 2022.

The vacancy rate held at 7.2% with 7.3% being the high in this cycle seen in February. Surpassing Austin, San Antonio is now the weakest market in the country while San Francisco remains the strongest with coastal markets overall doing better than sunbelt.

Apartment List said, “we now appear to have hit an inflection point, signaling that the rental market may finally be stabilizing as construction slows and the recent influx of new units gets absorbed.”

And, “The construction boom peaked in 2024, when we saw over 600 thousand new multifamily units hit the market, the most new supply in a single year since 1986. Since then, deliveries of new apartments have slowed considerably, albeit while remaining fairly robust by historic standards. Despite being on the downslope of the construction boom for nearly two years, the market had been struggling to absorb the swell of new inventory. That may finally be changing, as we see multifamily occupancy also hitting an inflection point in tandem with rent growth.”

Rents/shelter are the biggest component of CPI (second to healthcare in PCE) and this is a must watch as the quarters unfold.

I forgot to mention yesterday the important comments from the MSC Industrial earnings call from last week. As they are a major distributor of a variety of products that feed into the industrial and manufacturing sector, it’s a go to for me.

“The growth of our installed base is showing the benefits of an improving macro environment that should result in higher sales across existing locations, an effect which we commonly refer to as the coiled spring. We started to see early signs of this in the third quarter, with daily sales trends on a per unit basis showing volume improvement.”

“we are seeing further signs of an industrial recovery taking shape with positive IP readings across most of our top manufacturing end markets and five consecutive months of MBI readings above 50.”

I’ll add, as I believe some of this is due to inventory stocking in response to concerns over supplies and price increases with Strait issues, we’ll see in coming quarters how sustainable.

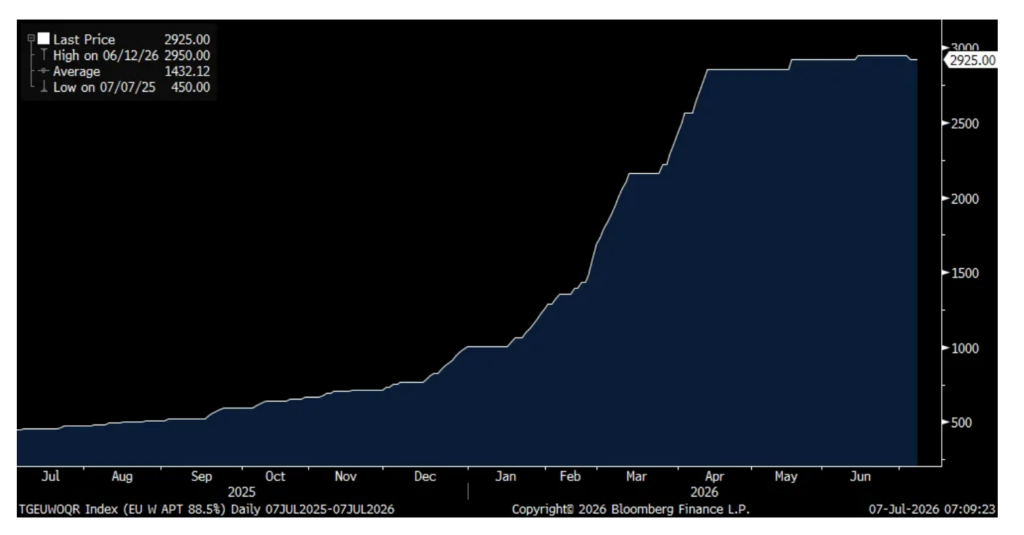

They raised prices by 7.2% y/o/y by the way. “Tungsten is still the largest driver of our inflation, and I think we’re not done.” Tungsten prices are up 500%.

And some more on the macro that they are seeing, “we are starting to see changes in behavior. So, the most notable that we haven’t sized yet, but we’re watching closely, is summer shutdown patterns are changing significantly. So, whereas we would have had pre-planned shutdowns, particularly in automotive, those are being canceled, or they’re not being announced as they would have been. So it’s still spotty, but it’s real.”

The price of Tungsten per dry metric ton

Positions: None.