Boockvar on Russia, Iran, China Inflation

From Peter Boockvar:

Yes, kinetic activity again in the Middle East but watch what’s going on in Russia too

While we’re back to watching the kinetic activity in the Middle East and how that might again impact energy markets and shipping thru the Strait, I’m beginning to believe that the oil product situation is getting worse because seemingly every day Ukraine is blowing up a Russian refinery and energy infrastructure there.

After months of attacks, it seems that they are happening more frequently and Russia is feeling it big time. Yesterday I’m reading this from The Independent, “Ukranian drones have reportedly targeted Russia’s largest oil refinery in Omsk, deep within Siberia, in what Kyiv’s military and Russian local authorities confirm was one of the longest range attacks of the ongoing conflict. The strike this week underscores Ukraine’s expanding reach. These persistent drone assaults are now intensifying fuel shortages across Russia, leading to widespread reports of escalating prices and lengthy queues at petrol stations throughout numerous regions.”

This followed a July 2nd attack on NORSI, Russia’s 4th largest oil refinery, owned by Lukoil.

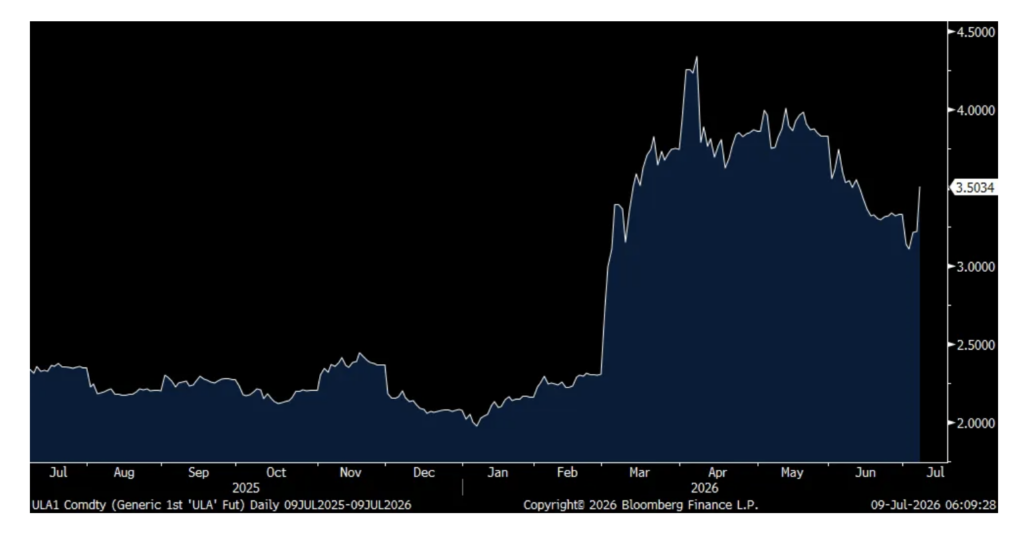

And in response yesterday, I see diesel futures spiking after reading “the Russian government announced a short term export ban on diesel…The export ban, which will last until July 31, came after Ukraine pounded Russian oil refineries with long range drone strikes, which caused a spreading fuel shortage and long lines at gas stations.”

As to why that matters here? “Until recently, Russia was the second biggest exporter of diesel after the US. Last year, the country supplied about 11% of global seaborne diesel, according to ship tracking company Vortexa.”

Diesel futures ended up 9% yesterday on the CME. In Europe, they jumped by 12%.

US Diesel Futures as of yesterday’s close

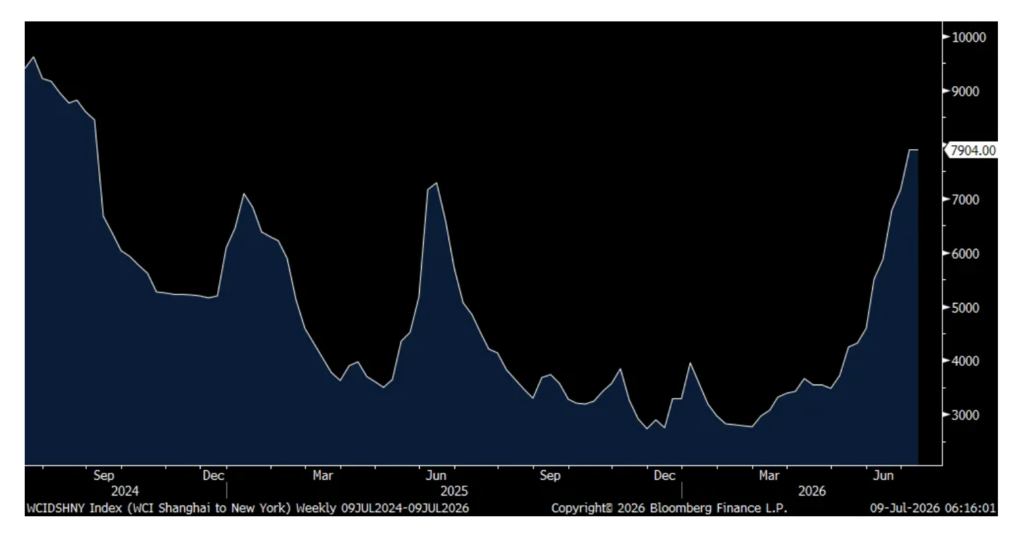

With respect to container shipping rates, which I’ve been highlighting for the past few months the consistent rise in costs, they were up slightly this week, though holding its gains. The Shanghai to NY at $7,904, up $2 is at the highest since September 2024. Shanghai to LA saw the price rise by $133 w/o/w, or by 2% to $6,482.

Shanghai to NY

As part of our holdings of a bunch of consumer staples stocks, we own Pepsi that just reported where they beat top line but missed bottom line by a penny. This from their earnings release ahead of this morning’s call:

“Net revenue increased 6.4% due to 2.4% organic revenue growth, a 2.2 percentage point benefit from FX translation and a 1.8 percentage point net benefit from acquisitions and divestitures. Organic revenue growth reflects the benefits associated with effective net pricing and a contribution from organic volume growth.”

From the Levi Strauss conference call and whose stock is down pre-market because of seemingly more conservative 2nd half guidance:

“Our international markets continue to demonstrate strong momentum, led by a 12% increase in Asia, while the US delivered a 6% increase.”

“Our consumer continues to be resilient. And has reflected another quarter of strong results. It’s broad based across channels, geographies and categories. So, you think of the beat, it’s geographically, it came from the US and Asia. Europe was as expected. It came from wholesale and came from women…we are seeing strength across value, core and premium.”

They continue to be hurt by tariffs. “The tariff environment continues to be uncertain and our updated guidance continues to assume incremental US tariffs on imports from China at a 30% rate and the rest of the world at 20%. Our guidance does not assume any benefit from potential tariff refund, which are approximately $80 million paid to date.”

Inflation stats out of China were about as expected. PPI rose 4.1% y/o/y while CPI was higher by 1% ex food and energy. The former reflects cost pressures being felt everywhere while the latter has been subdued for the past few years, good for a consumer that is being weighed down by the drop in wealth in residential real estate.

Positions: None.