Boockvar on Rising Default Rate, Treasuries

From Peter Boockvar:

Default rate update/Treasuries & other sovereigns/Home Depot

Fitch updated us with their April default figures yesterday for companies they follow in private credit. It rose to 6% which is the most since they started doing this in August 2024. That’s up from 5.7% in March. We know that there is so much focus on software but it wasn’t that at all that caused the rise. Fitch said they “recorded 10 private credit default events in April. Issuers in the industrial and manufacturing sector accounted for four events, followed by business services general with two. The consumer products, transportation and distribution, pharmaceuticals, and cable sectors each accounted for one event. Of the 10 private credit default events, six were new unique defaulters and four were serial defaulters.” Note, no mention of software.

Defining what qualified as a default, “Seven of the 10 default events involved maturity extensions under stress, while the remaining three involved the introduction of PIK interest in lieu of cash interest.”

Lastly on this, and to the point that software is not an issue here right now, “Healthcare providers remained the sector with the highest number of unique defaulters in the April TTM period. Twelve unique defaulters produced a 7% default rate, up from 6.9% in March 2026 and 5.8% in April 2025.”

Bottom line, private credit should still be a focus but as said, the software worries right now are not showing up in the data yet. Also, we have to differentiate the good underwriters from the not so good and not paint the whole sector with a broad brush. And finally, also differentiating a loan given to finance a private equity deal vs a loan lent to a borrower that wants to expand a business.

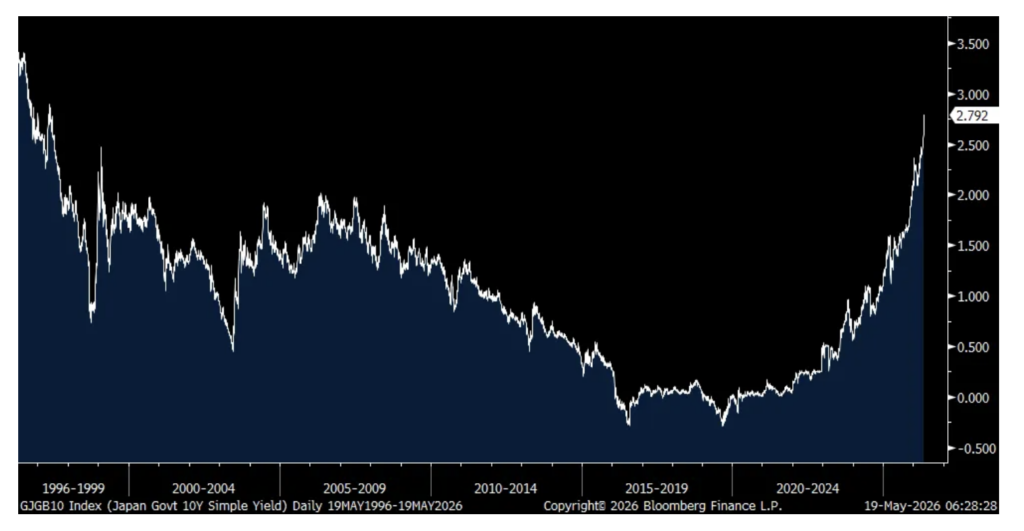

JGB yields jumped again overnight with the 10 yr yield up another 6 bps to 2.79% and we’re getting close to 30 yr highs. The chart is beginning to look vertical. I keep highlighting Japanese yields in particular because this was the original home of modern day interest rate suppression with ZIRP and QE and then they followed the Europeans into NIRP. And they remain the largest foreign holder of US Treasuries.

Speaking of those holdings of US Treasuries, Japan’s stock in Treasuries in March fell by $47.7b (including maturing T-bills not reinvested and changes in value). China’s holdings fell by $41b. Foreigners in the ‘foreign official’ category sold another $38b in total in notes/bonds. It was the $51.5b of ‘private’ buying that helped to offset that with ‘private’ including hedge funds in the Cayman Islands and their basis trades. UK holdings data are likely part of this too via UK banks.

If we include T-bills and those maturing and not reinvested, foreign holdings in total fell a large $138.4b worth with some of that due to falling values.

Bottom line, the US Treasury is relying more and more on US domestic savings and the basis trade to finance itself.

10 yr JGB Yield

Japanese holdings of US Treasuries, $1.192T

UK gilt yields are backing off a bit but not for good reason. In April, the ‘payrolled employee’ count fell by 100k, well worse than the estimate of down 10k. The caveat is that the ONS said there could be some beginning of the tax year distortions. Let’s hope so. The biggest job losses were seen in retail and leisure/hospitality. Also, jobless claims rose by another 26.5k. In the three months thru March, their unemployment rate rose one tenth m/o/m to 5%.

With respect to wages ex bonus, weekly earnings rose 3.4% y/o/y thru March which is not much above the rise in CPI. Tomorrow’s expected April CPI is expected to be up 3% y/o/y.

Home Depot had mixed results, beating top and line estimates but slightly missing Q1 comp forecasts. They said this in their earnings release of note ahead of their conference call:

“The underlying demand in our business was relatively similar to what we saw throughout fiscal 2025, despite greater consumer uncertainty and housing affordability pressure.”

In an interview, the CFO said that its customers “continue to defer large projects. They have told us that they have a higher degree of uncertainty.”

They reaffirmed its guidance with 2026 comps expected to be flat to up 2%.

Positions: None.