Boockvar on Rally, Bank of Japan Rate Hike, Gold

From Peter Boockvar:

That was not a Strait reopening relief rally/BoJ hikes/Gold survey/Other notables

Yesterday was not a reopening of the Strait relief rally. It was just an excuse to renew the GenAI momentum trade that has not been impacted negatively at all since the conflict began. I say this because the stocks that should have rallied with a deal and lower energy prices did not and if they did, barely.

For example, XRT, the equal weight retail ETF closed red yesterday. Walmart, Costco, Target, to name a few all closed down even though gasoline prices should continue to fall in the coming weeks. If there was one sector that I would have bet would have rallied, it would have been retail stocks. Airlines rallied with lower jet fuel prices but consumer staples/ product companies whose costs have gone up notably did not. ITB, the home builders etf, rose all of .1% even though they should get raw material price relief. Toy makers use a lot of plastic and any relief in the price of resins and petrochemicals would be welcome but Mattel traded down with just Hasbro up, by 1.3%.

Bond yields too didn’t react much with longer term yields little changed on the day. I could go on but you get the point, it was a weird trading day under the hood.

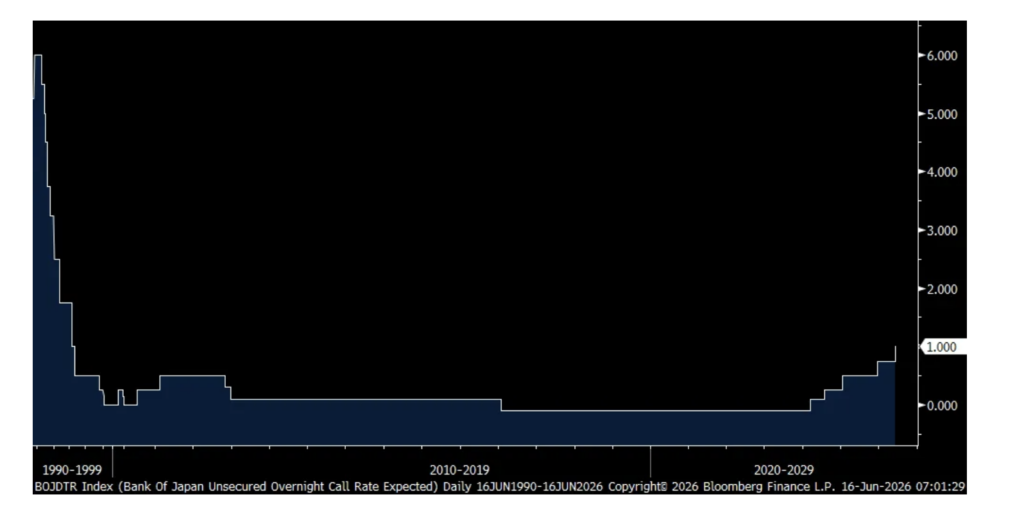

The big news today, though no surprise, was the Bank of Japan raised rates by 25 bps to 1.00%, a level last seen in 1995. The Deputy Governor Uchida held the press conference because Governor Ueda was ill. These were some of the things Uchida said of note:

“Compared with the previous meeting, the risk of a sharp deterioration in the economy has diminished. On the other hand, price rises are broadening, and there is a risk that underlying inflation may deviate from our target.”

“With underlying inflation approaching 2%, we need to be mindful of upward price risks. We will guide policy so that we won’t fall behind the curve.”

“Taking into account that medium and long-term inflation expectations have also continued to increase, there is a risk of underlying inflation deviating above our price target.”

“Wage growth is moving roughly in line with levels consistent with our price target.”

“We’re always watching currency moves closely. We don’t directly target exchange rates in guiding monetary policy. But we engage in monetary policy discussions on the view that currency moves have a crucial impact on economic and price developments. With companies’ wage- and price-setting behavior becoming more active, the pass-through (of the weak yen) may have a bigger impact on underlying inflation.”

As to when they might hike again, “We will look at economic, price and financial developments, particularly with an eye on the Middle East situation, for the time being. We’ll look at whether the economy and prices are moving in line with our forecasts, as well as risks. With underlying inflation approaching 2%, we need to be mindful of upward price risks. We will guide policy so that we won’t fall behind the curve.”

“The main difference between our previous meeting and this one is that downside risks to Japan’s economy have subsided significantly … Additionally, we have seen steady pass-through of costs in business-to-business prices, which led us to be more vigilant to inflation risks.”

They also as expected said they will pause the tapering of their bond purchases next April.

The yen initially rallied after the move and presser but is back to flat on the day. While it sounds like the BoJ is leaning to more hikes, the lack of any sense of timing explains the non-reaction in markets. Also to that, longer term JGB yields are moving higher and again, hiking rates for the BoJ rather than waiting for them to commit to another.

BoJ overnight rate

The Reserve Bank of Australia also gathered and left its rate unchanged as expected after previously taking it back up to the levels seen in 2022. Governor Bullock said that in response to the hikes, “You’ve got to expect a slowing in the economy, and when we see it, people shouldn’t be alarmed about that. That’s what actually has to happen in order to bring inflation down.” And she left the door open for more rate hikes, “If expectations of higher cost growth get embedded into price and wage setting decisions across the economy, this would lead to even higher and more persistent inflation, and it would require even more tightening in monetary policy to get inflation under control.”

As there were really no surprises from the RBA, the Aussie$ is little changed as was the 2 yr yield overnight.

With respect to gold and its place as a reserve asset, the World Gold Council today released its 2026 Central Bank Gold Reserves survey and conducted between February 5 and May 19th, thus capturing the attitudes pre and mostly post war. If you’re a bull and long such as we are, you’d be encouraged by the results.

1)”Respondents overwhelmingly (89%) believe that global central bank gold reserves will increase over the next 12 months.”

2)”This year, a record 45% of respondents expect their own gold reserves will also increase over the same period.”

3)”The majority of respondents (74%) see moderate or significantly lower US dollar holdings within global reserves over the next five years. Respondents also believe that the share of other currencies, such as the euro and renminbi will remain unchanged over the same period, while gold holdings will increase.”

Source: https://www.gold.org/

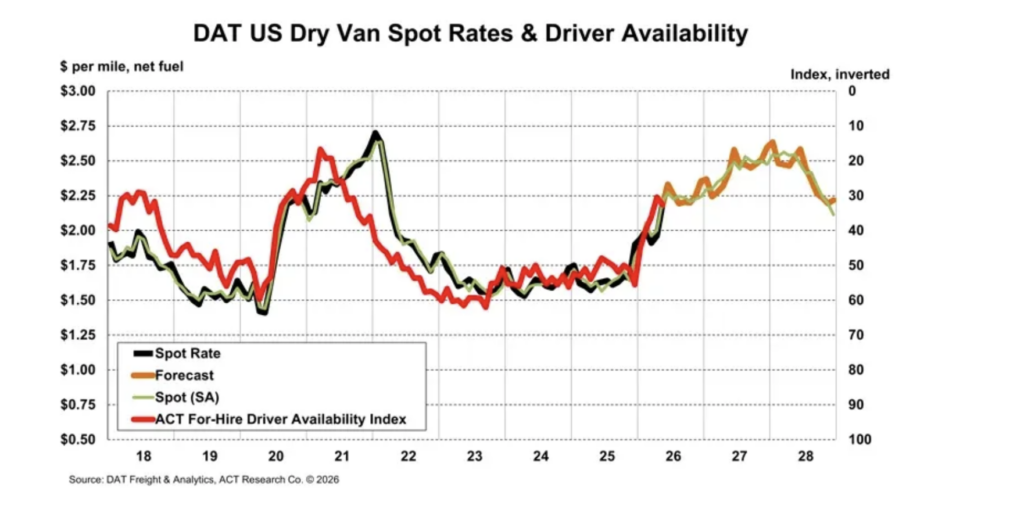

Higher trucking prices is something I keep talking about and Cass Freight yesterday had a good chart overlaying Dry Van per Mile spot prices with driver availability, aka, capacity and you can see the tight relationship. They said in their May report, “Volumes are beginning to recover, but it is mainly supply constraints supporting higher rates, in our view, both for equipment capacity and drivers.”

Back overseas, the June German ZEW investor expectations index in the German economy improved to +10.5 from -10.2 and much better than the estimate of -5.5. However, the Current Situation weakened to -81 from -77.8. The ZEW said “financial market experts expect the Iran conflict to be nearing an end. This is likely to ease the massive pressure on energy prices and inflation, which would benefit energy intensive industries and private households and would strengthen domestic demand.” Nothing market moving though with this data point.

The May economic data out of China was mixed again with still pressure on the consumer vs better performance on the industrial/manufacturing side. Retail sales fell by .6% y/o/y vs the estimate of a drop of .2%. Industrial production instead rose by 4.5% y/o/y, about as forecasted. Fixed asset investment remained weak with the downturn in residential construction. Positively though for housing, the pace of home price increases rose for a 4th straight month in the first tier cities like Shenzhen, Shanghai and Guangzhou, though fell again in Beijing. Prices were weak elsewhere though and this situation is an overall drag still on their economy but not getting any worse of note.

Positions: None.