Boockvar on Price Data

From Peter Boockvar:

Quick data rundown

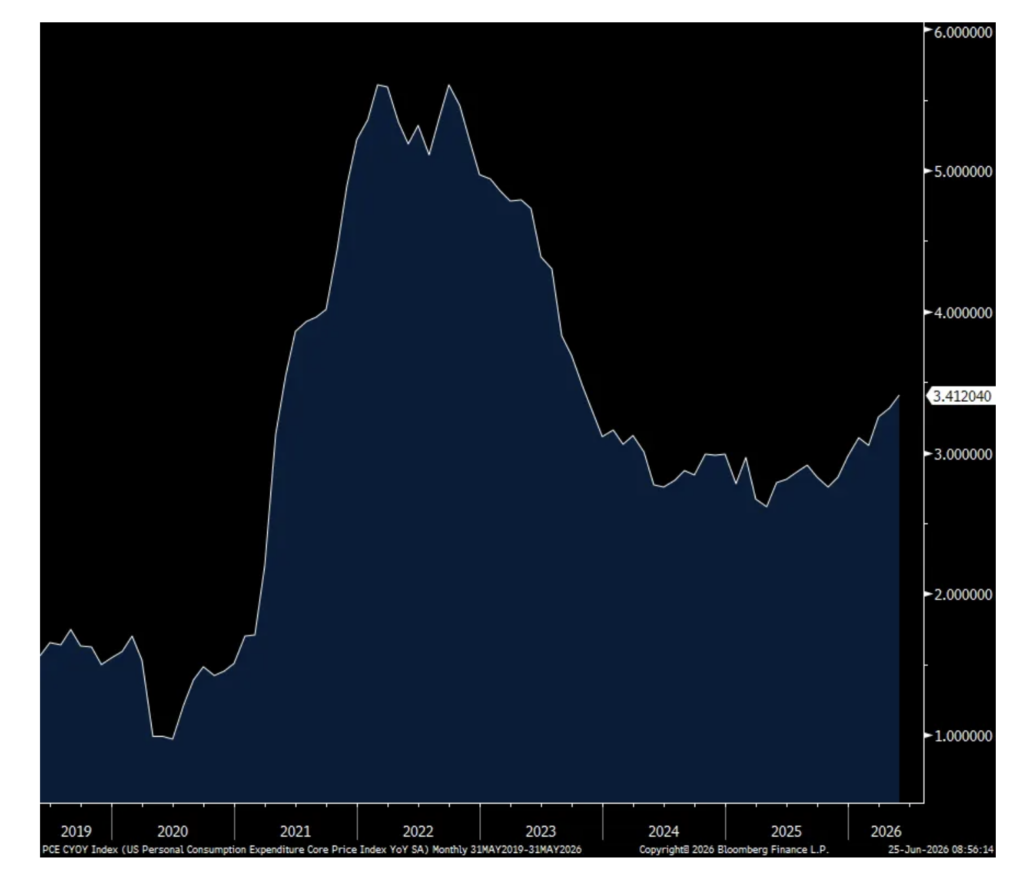

In May, the headline PCE rose .4% m/o/m and 4.1% y/o/y while the core rate was higher by .3% m/o/m and 3.4% y/o/y. Both about as expected due to rounding and up from 3.8% and 3.3% y/o/y gains seen in April. Of course oil prices have fallen sharply in June, making this data somewhat old news at the headline level. As CPI and PPI have already been seen, the PCE data rarely deviates from expectations.

Energy prices were up 4% in the month and by 24% y/o/y. Food prices grew by .6% m/o/m and 2.4% y/o/y. Goods prices for durable goods were up by 3.3% y/o/y. With services, prices were up by 3.8% y/o/y.

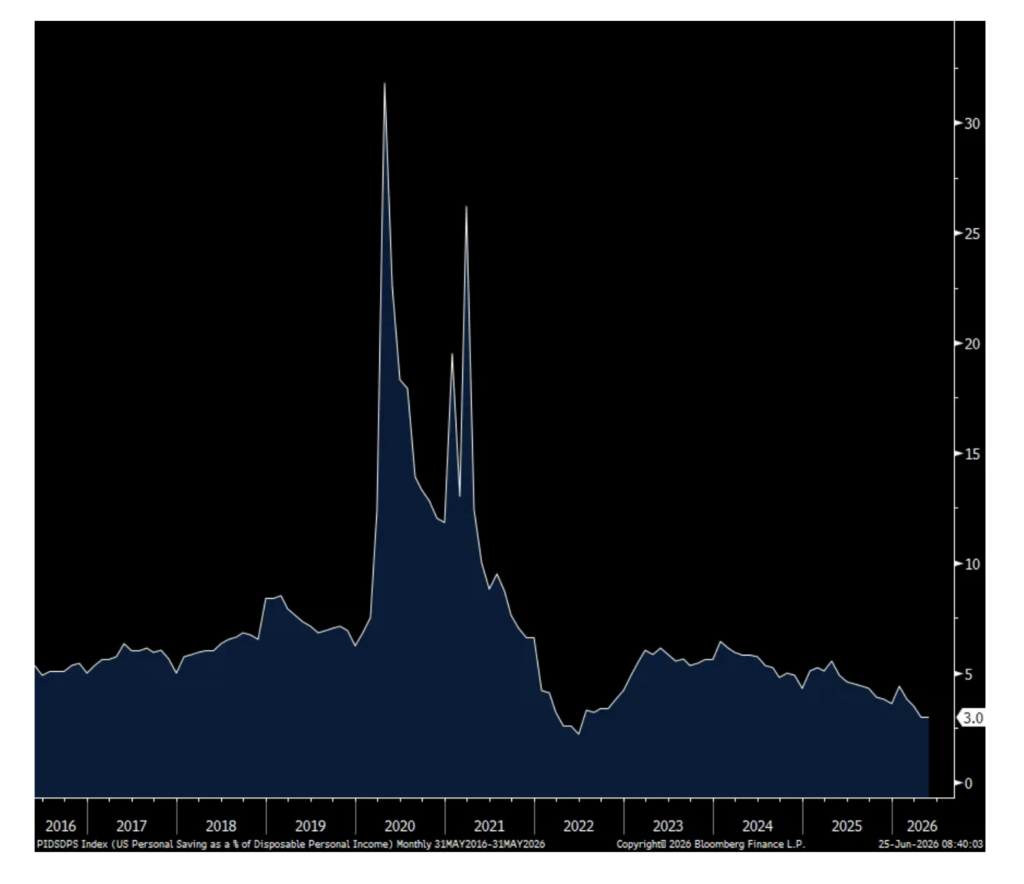

This matches up with an income rise of .7% m/o/m after no change in April while spending was higher by .7% m/o/m as expected when including the revision in the prior month. The savings rate at 3% combines this, unchanged with April but at the lowest level since June 2022.

With no surprise in the inflation stats and the anticipation of lower figures in the months to come, yields continue lower with the 2 yr yield now at 4.11%. That compares with 4.06% right before last week’s FOMC meeting and off the jump above 4.20% that followed. The 10 yr yield at 4.37% is now 6 bps below where it was before the meeting and further below the 4.50% key level.

Core PCE y/o/y

Savings Rate

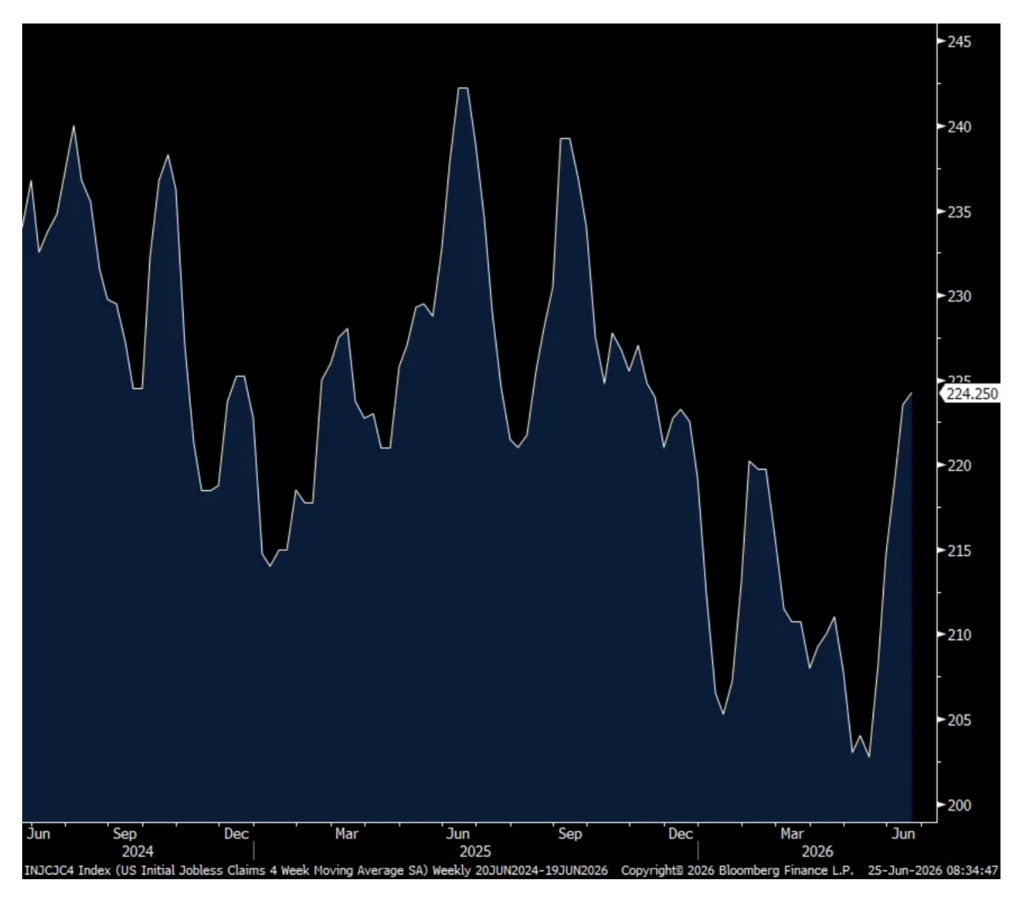

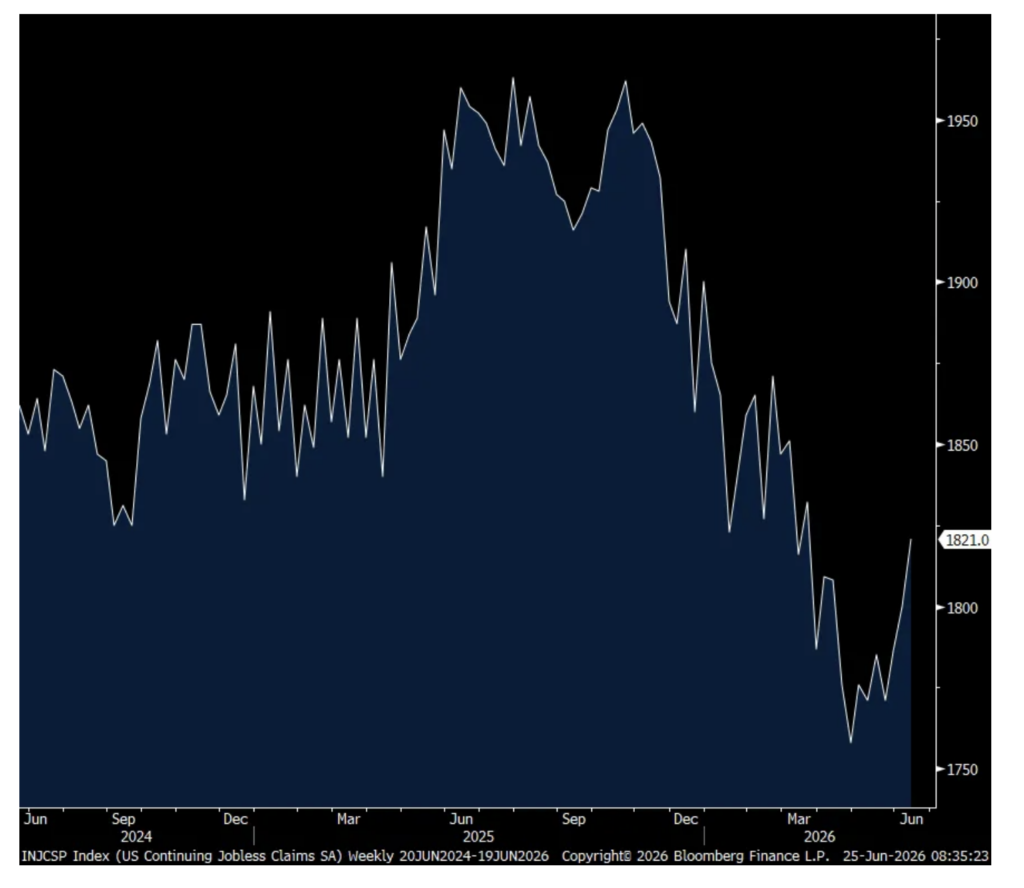

Initial jobless claims totaled 215k, 10k below expectations and down from 227k. Because of the holiday, we’ll combine this with next week’s print to smooth it out. Until then, the 4 week average of 224k is little changed with the previous week. Continuing claims, delayed by a week, totaled 1.821mm, up 21k w/o/w. That’s the highest since March but still well off its recent highs.

4 Week Avg Initial Claims

Continuing Claims

Core durable goods orders in May rose 1.6% m/o/m, well above the estimate of up .6% and follows a .7% fall in April (revised down from 1%). I still believe this includes some pull forward of orders. As part of the data center buildout, machinery orders were up another 1.9% m/o/m and 12.7% y/o/y. Orders for computers/electronics were up .3% m/o/m and 14.8% y/o/y. Electrical equipment orders rose .3% m/o/m and 5% y/o/y. Orders for metals too were strong in the month as you can’t build data centers without copper, silver, and other key minerals.

Shipments of core goods were as expected so won’t shift Q2 GDP estimates.

Positions: None.