Boockvar on Iran Deal, Wages, Inflation

From Peter Boockvar:

Finally this time?!/Exciting day ahead/Wages/RH and Lennar talk housing

It seems that the pressure on reopening fully the Hormuz Strait took on another level after hearing from the executives at Exxon and Chevron a few weeks ago when they talked at a conference about heading towards dangerous levels of inventories. And then I saw the article yesterday in the Washington Post titled “Oil Executives Warn White House That Gas Prices Will Get Worse” and which said “Oil and gas executives have warned the White House that gasoline prices could surge in coming months as fuel inventories fall to critical lows…Industry officials say they are doing everything they can to sound an alarm that prices are about to soar as the commercial and government inventories that have mitigated price rises so far are rapidly depleting, according to multiple people familiar with the conversations…Some inventories could be wiped out within weeks, the executives have warned, coinciding with the peak summer travel season.”

Unfortunately with an eventual deal though, I still don’t think we’re going to get everything we want but that’s the situation we’re in dealing with a regime like Iran. We’re just going to have to accept a deal that is not ideal it seems.

With regards to oil and gas stocks, the XLE will open less than a buck from where it stood on the February Friday before the conflict began. Believing that oil prices, after the price correction upon a deal fully runs its course, are not going back to pre-war levels and we still have the big picture challenge of slowing US production growth, we remain long the group.

A deal and full Strait reopening would be good timing for new Fed Chair Kevin Warsh as he would be able to better analyze the economic backdrop with more clarity and much less fog. I was never of the belief that the Fed should respond to the rise in oil and commodity driven inflation triggered by the war because at any moment the war could end and hopefully that’s the case now.

Today we celebrate coming to the public market of one of America’s technological wonders and one of our greatest entrepreneur’s. The reusable rocket has to be on the top 20 lists of greatest inventions in world history. The Starlink business is finally a satellite based telecommunication company that actually makes money (I remember Iridium, Globalstar, etc..). As for xAI, your guess is as good as mine on whether data centers in space can happen and if so, done in a cheaper fashion than on the ground and where a fix can take place if something breaks without sending technicians on rockets there every time. And, it’s growing more clear how competitive and costly providing cloud infrastructure is and how tough competing with Gemini, Anthropic, OpenAI and others globally is going to be. As for all the other moonshot hopes, I hope it all happens.

As for the valuation and how it trades in coming days/weeks/months, I have my popcorn out as I’ve never seen as much investor excitement to ‘get in’ than this. Speaking generally about the GenAI business, because of the hugely capital intensive nature of building out the GenAI infrastructure and likely continued high levels of maintenance CapEx, I believe the benefits in the future will more accrue to the users of the technology rather than as major profits and high returns on invested capital for the providers of it.

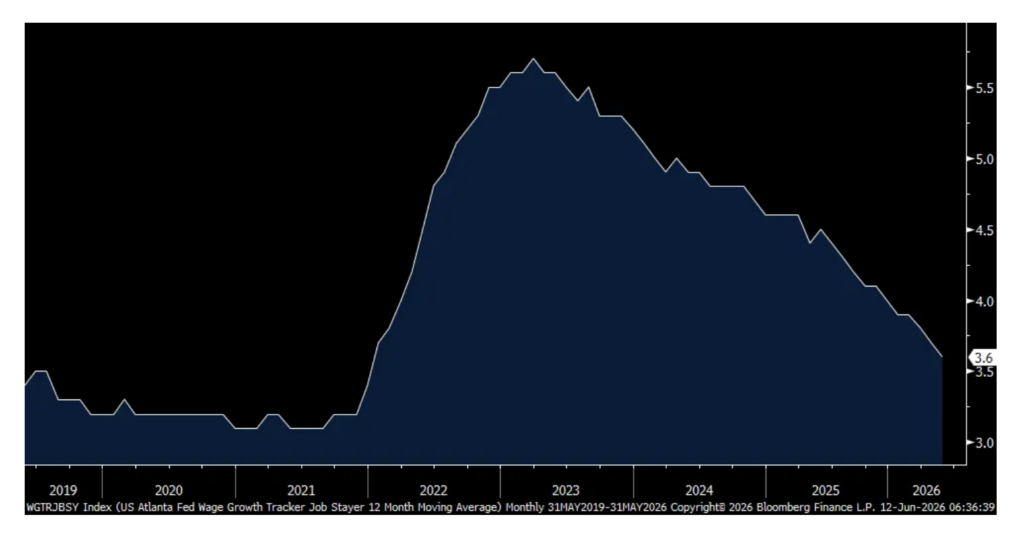

On the heels of seeing headline CPI for May rise 4.2% y/o/y, the Atlanta Wage Growth Tracker out yesterday showed a 3.5% y/o/y rate of growth and highlights the economic squeeze that continues on for many. For the ‘job switcher’, wages were up 4.3% y/o/y, holding the April gain. For ‘job stayers’, they were up higher by 3.6% which continues to decelerate.

Atlanta Wage Growth Tracker y/o/y

Job Switcher y/o/y

Job Stayer y/o/y

RH is always one of my favorite conference calls as CEO Gary Friedman gives us his 2 cents on things. They of course cater to the higher end consumer but have also dealt with the challenges of a tough housing market. From him:

“I think as we’ve moved past the peak investment cycle this year we believe our top line is going to inflect, that kind of irrelevant of what the external market does unless it really, look, if we get into a war that massively impacts the economy, the inflation, so on and so forth, it’s going to put pressure on everyone where those things happen, but we don’t need a big move in the housing market to grow. We don’t even need a move in the housing market. I’m not counting on the guidance we just gave everyone. I’m not counting on the market getting any better. I mean, the market can get worse, and I’d be surprised if we don’t beat those numbers.”

From Lennar who reported too and with numbers that missed expectations and they lowered their Q3 delivery guidance:

“Our second quarter of fiscal year 2026 was defined by the same stubborn headwinds that have challenged the housing market for the past several years – persistently elevated mortgage rates, constrained affordability, and cautious consumer sentiment, exacerbated by geopolitical uncertainty creating a resurgent inflation reading of 4.2% driven by higher energy prices.”

“Our average sales price was $371,000, reflecting approximately 12.9% in incentives, along with base price adjustments necessary to sustain volume in a market where affordability remains the defining constant.”

Positions: None.