Boockvar on Bank of Japan Rate Hike, Consumer Vs. Corporate

From Peter Boockvar:

The BoJ will hike/NFIB & two lane corporate & consumer highway/Other

As the BoJ likes to leak their intentions, it looks like they are going to raise interest rates next week. According to the Nikkei Asia news wire, “The Bank of Japan is set to raise its key interest rate to 1.0% from the current .75% at its upcoming policy board meeting on June 15 and 16, Nikkei has learned, as the Japanese economy faces upside inflation risks. The central bank is also considering pausing the tapering of its government bond purchasing program, starting in April 2027.” That would be the first rate hike in six months and a 1% overnight rate would be the highest since 1995.

The story was not enough to help the yen which is unchanged at 160, the level at which triggered intervention recently. The 2 yr JGB was flat and longer end yields are lower on that pause in the tapering part of the story, and maybe too why the yen didn’t rally. We should continue to have our eyes on the BoJ, the JGB market and the yen because of the global flow impact they all have.

https://asia.nikkei.com/economy/

After seeing the jobs section last week from the NFIB May Small Business Optimism, today they reported their full report and the headline index fell to 95.3 from 95.9 and that was the weakest since October 2024. To repeat, Plans to Hire fell to the lowest since May 2020 as did Job Openings Hard to Fill. Compensation was little changed m/o/m. Also of note, Higher Selling Prices rose by 6 pts to the highest since March 2023.

Capital spending plans fell 1 pt after rising by 1 pt in the month before. Plans to Increase Inventory rose 3 pts to 1% which is not much but matches the highest since December 2024 and gets to the pull forward of ordering I keep hearing about.

Those that Expect a Better Economy fell 1 pt but down for a 5th straight month and by 21 pts in that time frame. Those that Expect Higher Sales were down by 2 pts, lower for a 4th month and by 15 pts over that stretch. Good Time to Expand was unchanged at 7% after falling by 4 pts in each of the two months prior. Earnings trends improved by 4 pts to -15%.

The chief economist of the NFIB highlighted the two lane economy on the corporate side, “AI investment spending has contributed to some excitement in the economy. Despite the enthusiasm around AI, the overall picture is divided. More small business owners are struggling with significant and unpredictable hikes in fuel prices, which are more challenging for small businesses to pass on to their customers compared to their larger corporate competitors.”

Also, “In May 19% of small business owners reported taxes as their single most important problem, up 2 pts from April and ranking as the top issue. Reports of inflation as the single most important problem rose for the 3rd consecutive month in May. 18% of business owners cited inflation as their single most important business problem, up 2 pts from April and marking the highest reading since December 2024.”

I’ll add, I think it’s obvious that small business is just much less financially and logistically flexible to be able to absorb the cost shocks they keep enduring relative to their larger company peers.

NFIB Small Business Optimism Index

Plans to Hire

Higher Prices

On the consumer side, the NY Fed yesterday released its Consumer Expectations survey and we certainly know well of the two lane consumer highway as well and it’s reflected here. The report summed up the current household financial situation by saying this:

“Perceptions…compared to a year ago deteriorated, with a larger share of households reporting a worse financial situation, marking the highest reading since January 2023, and a slightly smaller share of households reporting a better financial situation. Year-ahead expectations about households’ financial situation also deteriorated, with an increase in the net share of households expecting a worse financial condition. The net share of households expecting a better versus worse financial situation in one year is at its lowest level since October 2022.”

More on rising business cost pressures and how the consumer is coping, this was from Campbell’s yesterday, a stock we own and one that is at the same level it stood at 23 years ago:

“So base inflation before the Middle East conflict, we were looking at base inflation of around 3%. So obviously with the price of oil where it is, and look, if oil stays around $100 a barrel, we’re looking at an additional 2% to 3% inflation on top of the core 3%. Also, as you probably know, there’s a driver shortage out there that not only are we having higher diesel costs, but that is causing higher inflation from a logistics and freight perspective as well.”

How will they counter this? “Elevated productivity is essential for us going into next year” but “if we need to take some pricing, that’s kind of a last resort, but obviously we’ll need to do that.”

And with the cost of eating out more expensive, “Within the meals & beverage portfolio, the at-home cooking consumer trend is resilient, and we expect that trend to continue.”

On how another company is managing its costs, Sonoco Products, a metal and paper consumer and industrial packaging company, said yesterday “it is implementing a $60 per ton price increase on all grades of uncoated recycled paperboard (URB) in the US and Canada, effective with shipments beginning July 8, 2026.”

A general manager there said “This necessary increase is driven by several factors, including robust demand across our markets and strong utilization in our paper mill network. Additionally, elevated inflationary pressures have significantly increased our operating costs.”

In addition, “Sonoco also will increase prices for all converted paperboard products by 7%, effective with shipments on and after July 8, 2026. This includes paperboard tubes, cores, cones, partitions, protective packaging, and other specialty products.”

Think toilet paper and paper towels when hearing tubes and cores while the URB is used in industrial markets.

Overseas, China reported its May trade data and note here too the likely inventory stocking mentality of those placing orders. Exports grew by 19.4% y/o/y, above the estimate of 15%. Imports jumped by 27.4%, just above the forecast of 26% growth. Their monthly trade surplus of $105 billion is still quite astonishing. About half of the growth of both imports and exports were tech related, particularly chips and computer hardware with a lot from price rather than volume. Auto exports were strong too as we know China cars are flooding other markets.

Some pull forward of ordering was also likely seen in the somewhat dated April trade data out of Germany where exports rose .9% y/o/y vs the estimate of down .5% while imports grew by 1.2% vs the forecast of a decline of 2%.

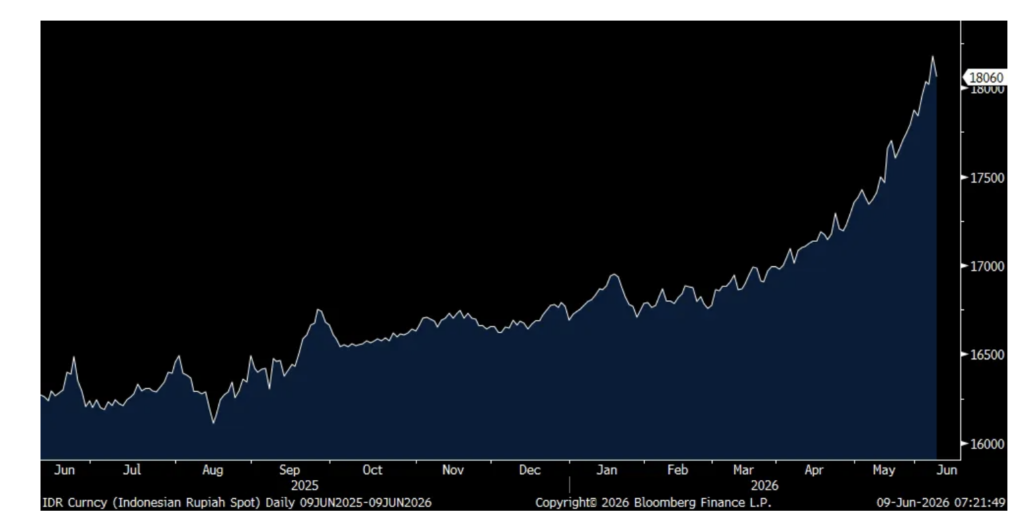

In order to stem both the rising inflationary pressures but also the weakness in its currency, the Bank Indonesia unexpectedly raised rates by 25 bps to 5.50%. This was NOT a scheduled meeting and they now have hiked by 75 bps since April 22nd when they last left rates unchanged. After a long run of weakness, the rupiah is rallying in response but not by much, not even getting back Monday’s weakness.

Bad economic policy from the Prabowo government helps explain the currency weakness and certainly the huge decline in the stock market his year to date by 33.5% for the Jakarta index.

Rupiah (higher the weaker vs USD)

Positions: None.