Boockvar Notes on Peace Deal, Extended Moving Averages, Used Vehicles

From Peter Boockvar:

Just a few things

With further complications in the Middle East, understanding this was never going to be an easy thing to resolve and finish, I keep remembering the comments from Exxon and Chevron a few weeks ago about dwindling inventories. In both believing in the big risks to the upside in price and that whenever this gets fully resolved, and it will, not believing there is much risk to the downside, we remain long oil and gas stocks.

However Meta decides to raise more capital from here, from the story Friday, on the heels of the Google raise, we’re reminded again how expensive this build out is and these companies that were once cash flow gushers are no longer.

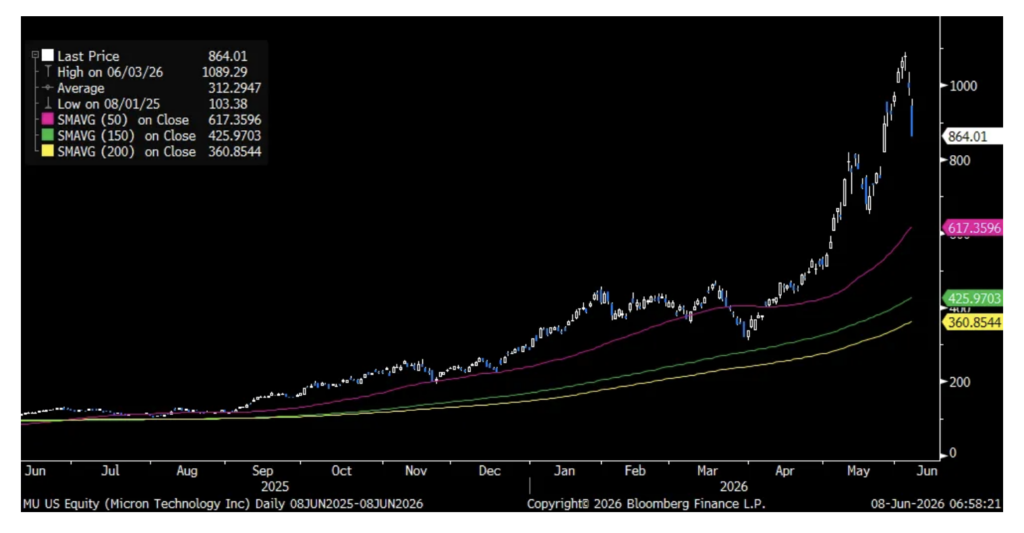

As for the stock market selloff, it doesn’t take a technician to see how extended above the moving averages we were in the semis and other parts of the AI infrastructure trade that just needed a catalyst to correct back. And considering we’re still well above the 50 day in many cases, there could be more to this in the short term.

Micron stock to use as one example:

Ahead of the May CPI report on Wednesday, Manheim released its May wholesale used vehicle index on Friday that rose 3.6% y/o/y and .3% m/o/m. They said, “Wholesale value trends continue to normalize from a strong start to the year, as we start to move into summer months and consumers continue to contend with higher gas prices. The Manheim Index overall remains higher against last year, yet it wasn’t as strong as we normally see within the month. As values were much higher in February and March, they started to normalize and depreciate in May, with non-seasonally adjusted prices falling a bit over one percentage point in the month. But the big picture shows good balance in supply and demand, with days’ supply sitting at pretty seasonal levels, even if it remains a bit below last year.”

Also, “we continue to see dealers bidding up the prices of EVs faster than Non-EV values at Manheim, consistent with gas prices that remain higher by 38% against last May.”

Lastly, “Affordability concerns continue, as we’ve seen higher appreciation in older units at Manheim this year – a trend we’ve been calling out recently. Additionally, some of the most affordable segments are showing the highest gains so far this year with compact cars higher by 12.3% in non-adjusted values since December, the highest of any major segment.”

Here were some macro tidbits from the ABM Industries earnings call Friday, a stock we own and up 6.8% in a tough tape, and a provider of a variety of services to many different end markets:

Offering janitorial services to office buildings in particular, “the prime office recovery continues to gain traction. Although as mentioned, the market is still experiencing some softness on the West Coast. The US office leasing is approaching 2019 levels. Net absorption turned significantly positive in the first quarter, the strongest since 2020 and prime vacancy rates continue to tighten. New supply remains extremely limited with the construction pipeline nearly 90% below its 2020 peak.”

West Coast markets they are referring to are LA, San Francisco and Seattle, “they’re probably two or three times worse than New York City. And if you were to think about those markets, think West Coast is kind of tech heavy, whereas East Coast is banking, legal. And from a return to work standpoint also as you guys know, like West Coast, when it comes to the tech sector, they’re not returning to work the same way financial services and legal is.”

Just one data point of note overseas and that was the somewhat dated April factory order number from Germany. It was weaker than expected, falling 3.8% m/o/m vs the expected drop of 2% and March was revised down by 5 tenths to a 4.5% gain. Declines were seen in auto, electrical equipment and machinery. The economy ministry said “There are growing signs that rising energy and commodity prices, as well as significantly heightened geopolitical uncertainty, are increasingly leading to lower demand, particularly for capital goods. Against the backdrop of rising costs and uncertainties, as well as growing supply chain bottlenecks, industrial activity is likely to continue to show only modest growth in the coming months.”

Positions: None.