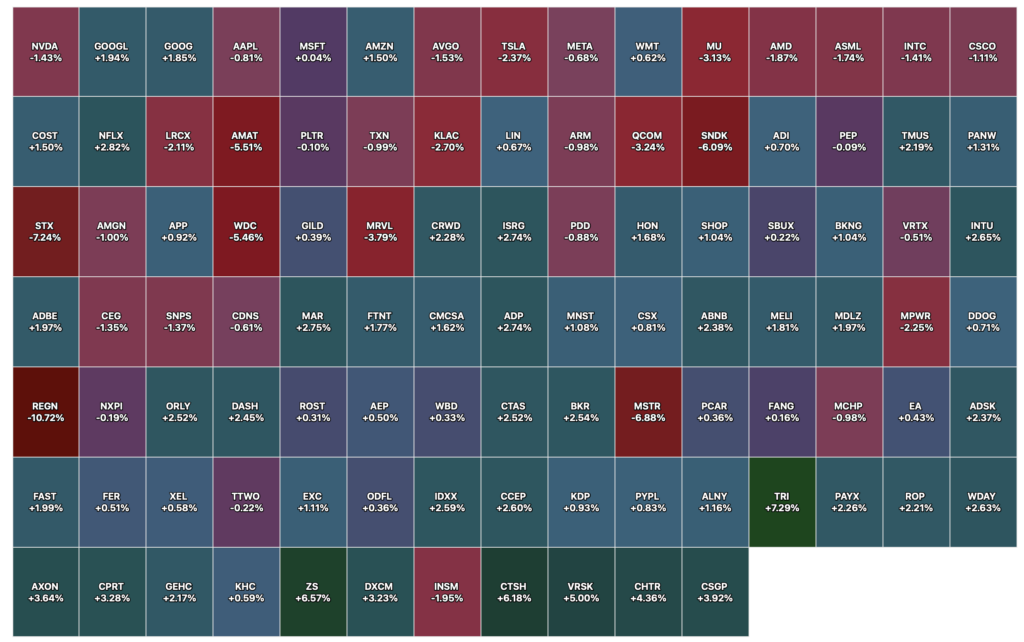

Charting the Late Morning Market Moves

Positions: None.

Positions: None.

Friday’s consumer staples paying off on Monday.

From Friday:

I have moved to medium-sized long (from small) in (PEP), (KMB) and (PG) this morning.

Positions: Long PEP M KMB M PG M

BY Doug Kass · May 15, 2026, 10:29 AM EDT

Positions: Long PEP M KMB M PG M

Chart from 9:45 a.m. ET

Positions: None.

I covered my Index shorts on the reversal for a quick and nice profit:

* SPY ($SPY) $738.43

* QQQ ($QQQ) $707.69

From earlier:

DDougie Kass

39m ago

Added to Index shorts:

SPY $741.03

QQQ $712.72

Positions: None.

From Peter Boockvar:

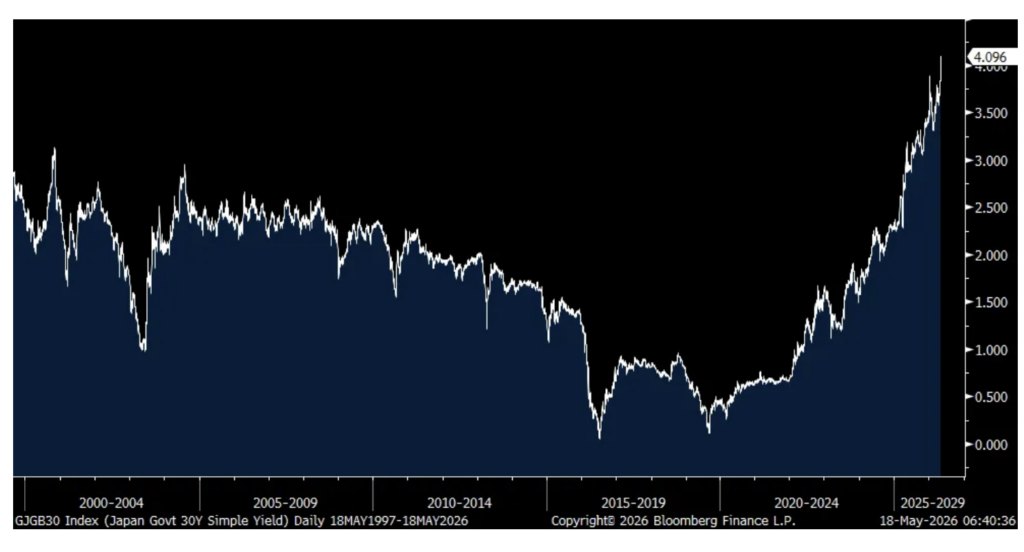

After the breakout in global bond yields Friday, they continue higher today, albeit more modestly. It started in Japan as yields there moved up again, particularly the longer end of their curve with the 30 yr yield up another 6 bps to 4.10% and the 40 yr yield higher by 9 bps to 4.34%. Evidence that excessive debts and deficits now matter, as one of the factors leading to higher yields, the move up today was in response to talk that the Takaichi government was going to ask for a supplementary budget to cover the extra subsidies for its people to cushion the blow of higher commodity costs, particularly energy. This would entail more bond issuance.

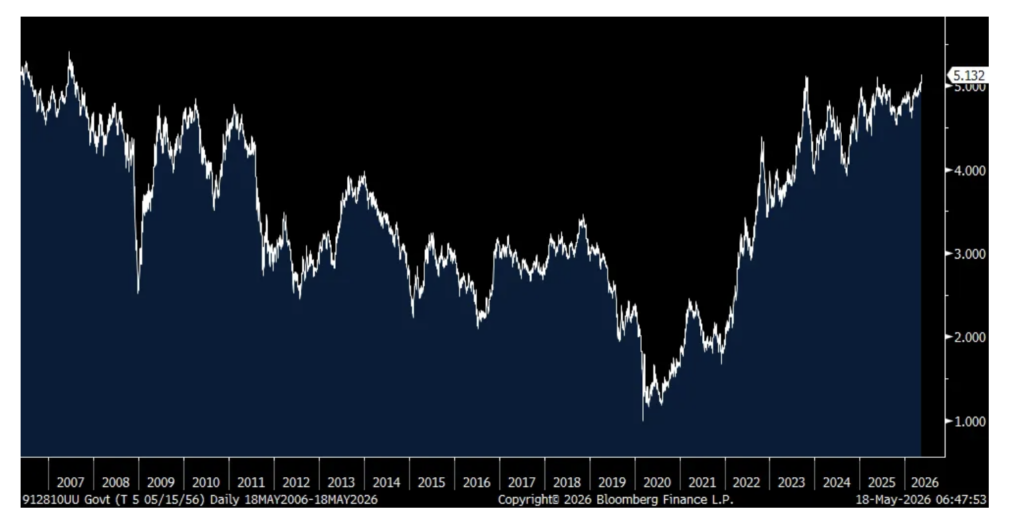

This is also helping to boost the US 30 yr bond yield to a 19 year high at 5.13%.

JGB 30 yr Yield

US 30 yr Yield

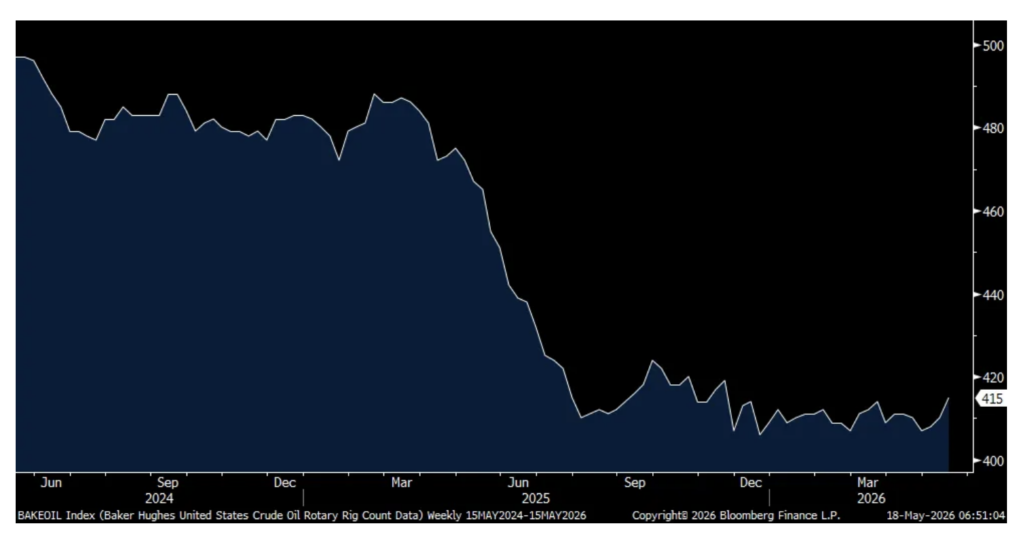

We finally got a lift in the Baker Hughes crude oil rig count of 5 rigs to 415, the most since last November but still well below the 465 seen one year ago and the 497 two years ago.

Crude Oil Rig Count

Soybean prices are rebounding by 2%, after falling last week, on news of Chinese purchases coming over the next three years. I believe we’re in the early stages of an ag bull market that will join industrial and precious metals along with energy.

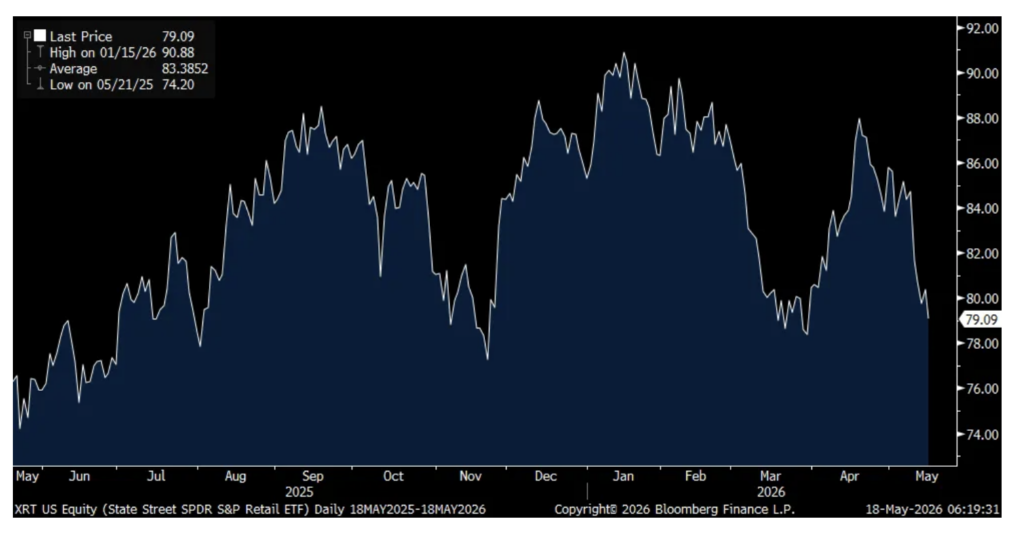

Good timing to start hearing from retailers about the state of their consumers just as the XRT, the equal weight retail ETF, is just off the lowest level since last November. Walmart, Target, Home Depot, Lowe’s, TJX, Ross Stores, and BJ Wholesale all divulge earnings this week. And of course Nvidia, whose earnings news and stock reaction could singlehandedly impact the sales of the above since it is so widely held with its $5.5 trillion market cap.

XRT

Speaking of the US consumer, this is what Simon Property Group, the major mall owner and operator said last week on their earnings call:

“Clearly, the upper end consumer is doing very well. You could look at the stock market, that should not be a surprise. And so, you’re obviously seeing that in the luxury business, with some of the brands, frankly, that might have been a little bit softer in the past couple of years, now starting to see some rebounds. But really, you’re seeing it in the hard luxury and jewelry and watches, really, really solid growth.”

They were also positive on the Gen Z customer and the stores that are catering to them.

But, “The only thing I would say that is a touch softer is on the food and beverage side, which is basically what’s flat from a comp perspective. And so, that’s probably not surprising seeing some of the earnings from the restaurant groups out there. But whether it’s a trading down effect, maybe one less trip out, that’s the only place we’re seeing it. But the rest of it is broad based growth. Obviously, athleisure is still very strong across the portfolio.”

“The only other thing I guess I could say on sales is the tourist market that really rely on the European and Canadian international traveler, that is a touch softer.”

These were some comments from International Flavors & Fragrances, a stock we own, from their call a few weeks ago but I highlight because of what they said on how they are managing the rise in cost inputs and the consumer price inflation that is to come:

“As a result of the ongoing Middle East conflict, inflationary pressures are expected to build over the course of 2026. We are proactively working with our customers to offset these pressures through pricing actions, starting with surcharges related to logistics and energy costs and then building to account for raw material inflation. In terms of phasing, we expect these inflationary trends to adversely impact profitability in the second quarter of 2026, where costs will begin to increase, and our pricing actions are not fully implemented. Post Q2, we expect this pressure to gradually ease through the back half of the year as pricing actions take full effect.”

“our pricing in our industry is a strong part of our algorithm in the sense that it’s the part of where we do business. And so consistent with historical inflationary cycles, we collaborate with our customers to fully offset any inflation, and usually it’s a 12-18 month period. I do not expect anything materially different this time around as we continue to engage and work with the customers there.”

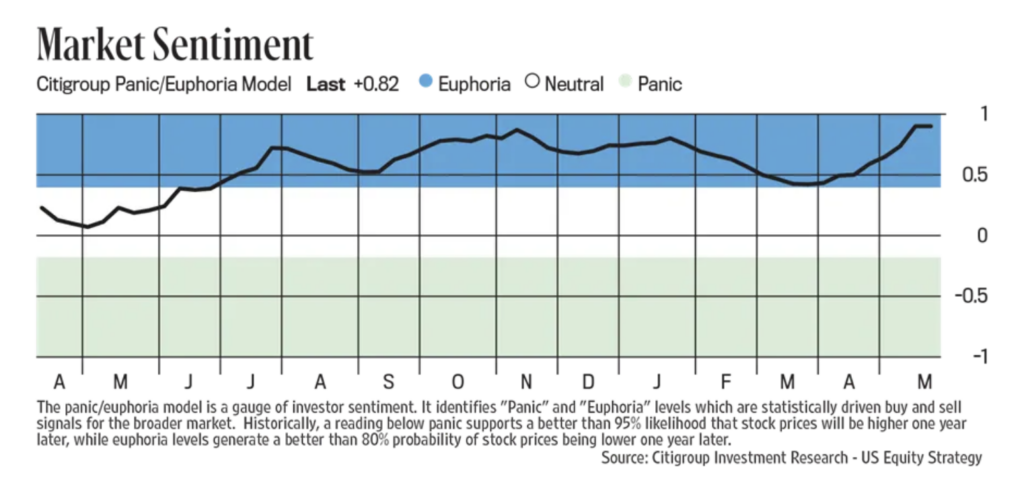

The Citi Panic/Euphoria index is now very Euphoric with this gauge now at .82, double the .41 Euphoria threshold. I had to go back to 2021 to find a reading above that. Assume this was taken before Friday’s selloff and worth noting and being aware of one’s sentiment surroundings.

China released its April economic data and it was weak across the board but with signs of hope that home price declines are lessening. Retail sales rose just .2% y/o/y vs the estimate of 2.0% and vs 1.7% in March. Industrial production slowed to a 4.1% y/o/y gain vs 5.7% in March and below the forecast of up 6%. Fixed asset investment ytd y/o/y declined and property investment fell by almost 14% (which is good from a supply perspective though).

With home prices, less bad is now the focus. With new homes, prices fell in 49 cities m/o/m vs 54 in March, 53 in February and 62 in January. With existing homes, 54 of 70 cities saw more m/o/m price declines vs 53 in March, 66 in February, 67 in January and in all 70 in December. Stocks in Shanghai were flat but down in Hong Kong by 1.1%. We’re still long some stocks in Hong Kong.

Positions: None.

Positions: None.

Positions: None.

Positions: None.

“Even a happy life cannot be without a measure of darkness, and the word happy would lose its meaning if it were not balanced by sadness.”

“Even a happy life cannot be without a measure of darkness, and the word happy would lose its meaning if it were not balanced by sadness.”

– Carl Jung

There is almost a gravitational pull for equities to move higher over time. Though a rise in stocks is only a coin flip on a daily basis — increasing in value about 55% of the time on all trading days — equities advance by about 70% of the time on a monthly basis and roughly 80% of the time on a rolling one-year period.

This means that calling a market top, like calling a generational market bottom (as I did in the first week of March 2009), is a low probability event that exposes one to criticism.

Nonetheless, I never shy away from public ridicule.

I have long written that owning equities creates wealth and being short equities protects capital.

The real purpose of calling a potential market top is to emphasize that the preponderance of negatives, when weighed against elevated share prices, suggests that we could be at a critical juncture for markets in which the downside risks may dwarf the upside rewards.

So, let’s start the week with a Ludacris Forecast (of a possible market top for this year) I made on Thursday:

This modifies my lengthy and ursine market view delivered in Wednesday’s five-part opener, earlier last week:

The Market Bacchanal Rages On — While I Remain Celibate

The Market Bacchanal Rages On — While I Remain Celibate (Part 2)

The Market Bacchanal Rages On — While I Remain Celibate (Part 3)

The Market Bacchanal Rages On — While I Remain Celibate (Part 4)

The Market Bacchanal Rages On — While I Remain Celibate (Part 5)

Position: None