Boockvar on Oil, Micron, Shipping

From Peter Boockvar:

Oil prices/Incredible Micron quarter/Shipping costs

With WTI crude oil now just about $3 from where it was before the Middle East conflict began, the 14 day Relative Strength Index is now at the lowest since September 2020, when we were slowly coming out of Covid but before the vaccine news. The Daily Sentiment Index is down to just 12 (range of 0-100), according to my friend Helene Meisler. I still think prices eventually settle out in the $80s but no question I’m very surprised at how much they’ve fallen. By the way, the Daily Sentiment Index for gold and silver are now down to just 10 and the DXY is up to 83. All stretched readings.

The Dallas Fed released its quarterly energy survey and said this:

“Activity in the oil and gas sector jumped in second quarter 2026, according to oil and gas executives responding to the Dallas Fed Energy Survey. The business activity index, the survey’s broadest measure of the conditions energy firms face in the Eleventh District, increased from 21.0 in the first quarter to 46.1 in the second quarter, marking the strongest reading since second quarter 2022. The survey was in the field June 9–17 as the U.S. and Iran negotiated a memorandum of understanding about ending hostilities.”

And, “Oil production advanced modestly in the second quarter, while natural gas production saw only minimal gains, according to executives at exploration and production (E&P) firms. The oil production index increased from zero in the first quarter to 15.0 in the second quarter, whereas the natural gas production index remained relatively unchanged at 3.7.”

With input inflation, “Costs increased at a faster pace relative to the prior quarter. Among oilfield services firms, the input cost index surged from 34.9 to 64.4, with no respondents reporting a decrease in costs. Among E&P firms, the finding and development costs index increased from 22.3 to 40.0. Meanwhile, the lease operating expenses index rose from 30.0 to 43.7. All cost indexes were above their series averages, suggesting costs are growing at a faster-than-average pace.”

And where respondents think prices settle out at, “On average, respondents expect a West Texas Intermediate (WTI) oil price of $81 per barrel at year-end 2026; responses ranged from $60 to $150 per barrel. When asked about longer-term expectations, respondents on average said they expect a WTI oil price of $78 per barrel two years from now and $82 per barrel five years from now. Survey participants foresee a Henry Hub natural gas price of $3.36 per million British thermal units (MMBtu) at year-end 2026.” I bolded.

Micron certainly crushed it with their quarterly earnings, though I still wonder to the extent they’re seeing double and triple ordering. Coincident with the booming business we know is the also high level of speculation particularly in the South Korean Kospi (up 5% overnight) and the trading in Samsung and SK Hynix where each now have 2x leveraged ETFs and margin debt there is at a record high (as it is in the US at 4.5% of GDP).

If you didn’t see, this was an article in yesterday’s FT, “South Koreans pour AI stock windfalls into overheated property market.” It said, “Securities sales proceeds were used in 13.2% of home purchases worth more than Won1.5bn ($974,000) in April, according to data from the land ministry, the first time the figure reached double digits and nearly triple the monthly level in most of the past five years.”

“For years, South Korea’s government has struggled to convince its citizens to invest more in domestic equities and less in the overheated property market, which it blames for rising inequality and plunging birth rates as elevated housing costs deter couples from starting families.”

“Despite the (equity) rally, property still accounts for 75% of household wealth, far above levels in other rich countries and dwarfing the 9% held in equities,” according to Morgan Stanley.”

https://www.ft.com/content/4a7137ff-903f-4246-96bf-4919ccb53543?syn-25a6b1a6=1

Back to Micron, this of note from their earnings call:

“DRAM and NAND industry demand continues to significantly exceed industry supply. We expect tight conditions to persist beyond calendar 2027, as a result of AI driven demand across all segments, coupled with structural supply.”

“We are excited to announced that we have now signed 16 strategic customer agreements or SCAs, which we expect will fundamentally transform our business model. The memory industry has been structurally transformed by the proliferation of AI.”

With regard to these SCA’s, Micron is saying that they “cannot be canceled…These are designed to be take-or-pay agreements outside of automotive.” And, “There are annual volume commitments for each of those years (5)” and “they are obligated to pay for the price times the volume. The price itself for a lot of these large agreements has a price band. There is a price ceiling and a price floor. The price gets negotiated every quarter based on market conditions. The price cannot exceed the ceiling no matter what, cannot go below the floor no matter what, and consequently the value of these agreements can be readily determined.”

“We now expect supply demand conditions for both DRAM and NAND to remain tight beyond calendar 2027. In DRAM, we expect industry DRAM bit shipments in calendar 2026 to grow in the low-to-mid 20s percentage range, slightly above our prior outlook. In NAND, we expect industry NAND bit shipments in calendar 2026 to grow approximately 20%, unchanged from prior expectations.”

The operating margin of 81.2% is astonishing, “up 12 percentage points sequentially and 54 percentage points y/o/y.” The gross margin was 85% and they expect “approximately” 86% in the current quarter. I’ll add, incredible but will be tough to increase them further from here.

They did get a question about the competition from the Chinese, CXMT and Yangzte, something I mentioned this week. “I mean, certainly those two companies have grown over the years in terms of their capabilities and share. Most of their output, the overwhelming majority of their output tends to be sold within China. We haven’t really seen much by way of their product or competition from them outside of China.” I’m sure that will change in the coming years though.

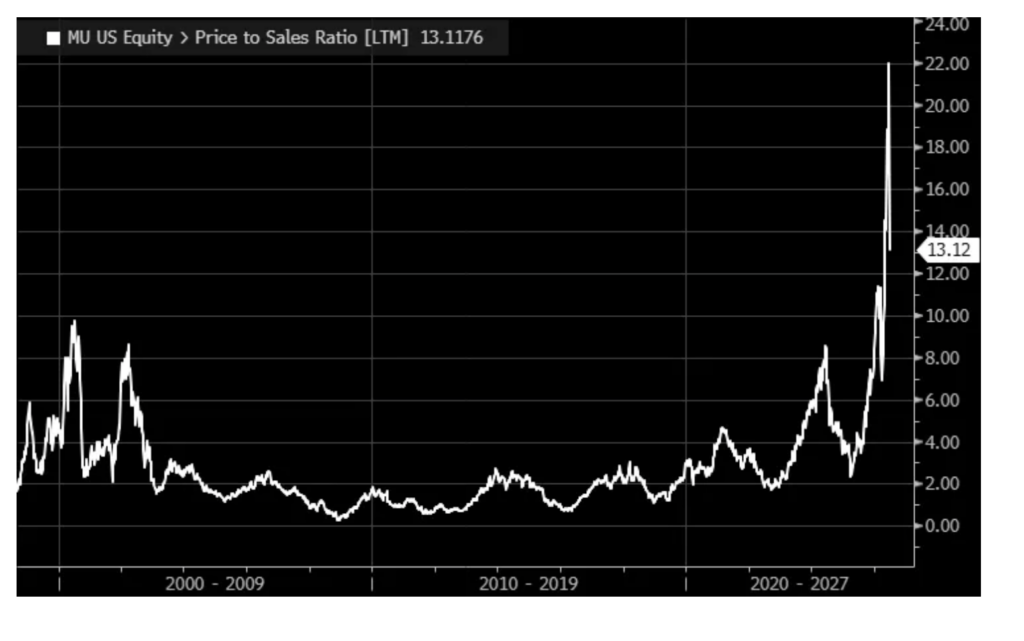

I will finish with Micron on the valuation debate. When analyzing a highly cyclical business and looking at a one year P/E ratio, it is a very incomplete picture when margins are very high, typically temporarily. I believe a better view is looking at Price to Sales and for Micron that sits at about 10x for their expected fiscal year. For perspective, it peaked at 10x price to sales in 2000.

Maybe this time is different and their business is structurally more sound. I have no opinion on that nor on the stock but just wanted to widen the debate on valuation because a P/E ratio on one year of earnings for a highly cyclical business is something I saw in 2005-2006 when I heard about how cheap homebuilder stocks were then. That of course was because they were dramatically over-earning.

Ignore the spike below as it’s calculating LTM and I’m talking about full fiscal year figures.

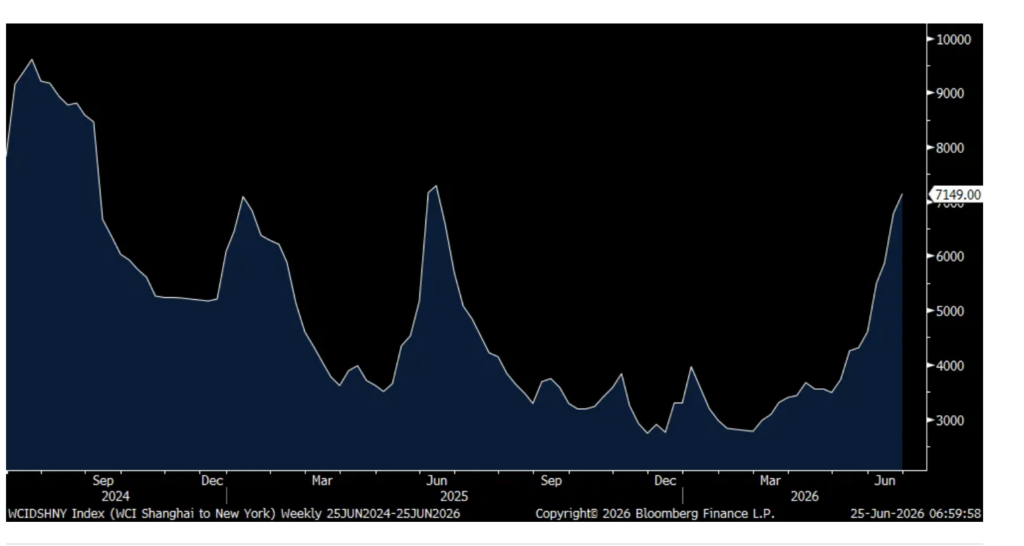

Hopefully we’ll get some relief soon with the Strait reopening but at least thru 6/25, container shipping prices continue to jump. The Shanghai to NY trip rose another 5.6% w/o/w, up for an 8th straight week to $7,149 for a 40 foot container. That’s the highest since last June. The price for the route to LA rose by a similar amount and less so to Rotterdam.

Shanghai to NY

Positions: None.