Boockvar on ISM Services Data, Inventory Stocking

From Peter Boockvar:

ISM services, helped by inventory stocking

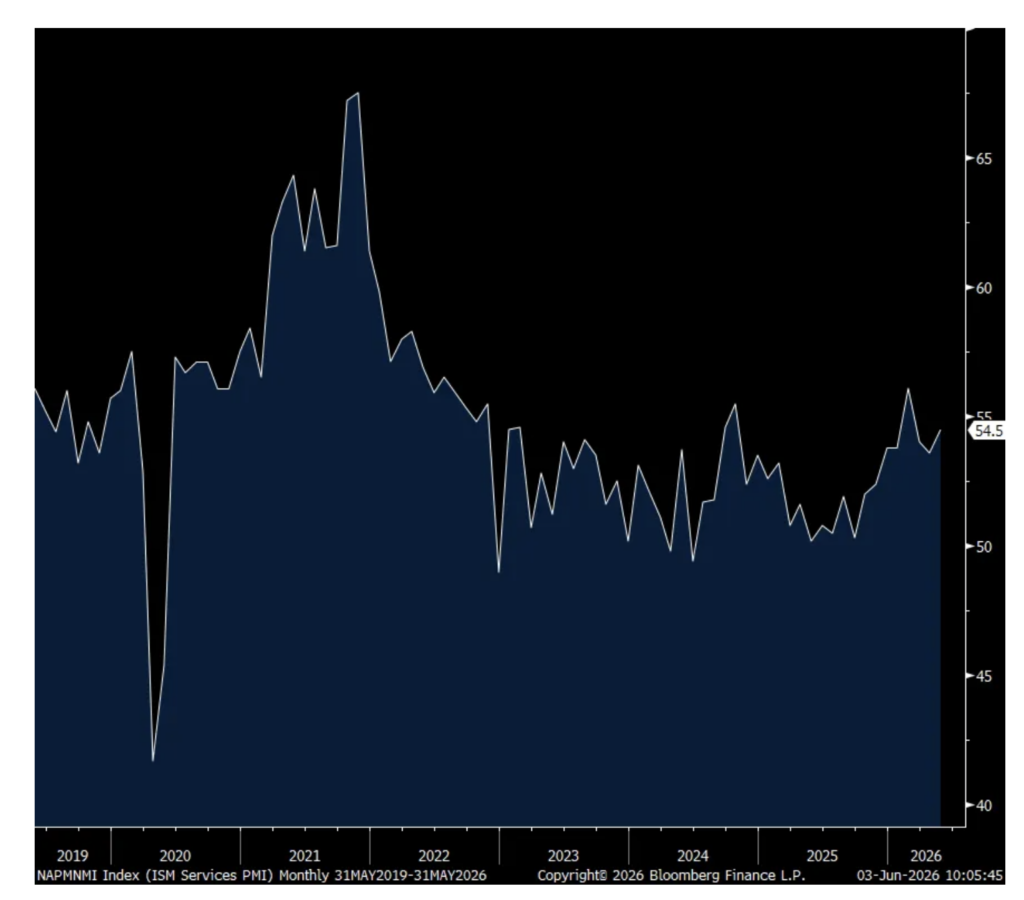

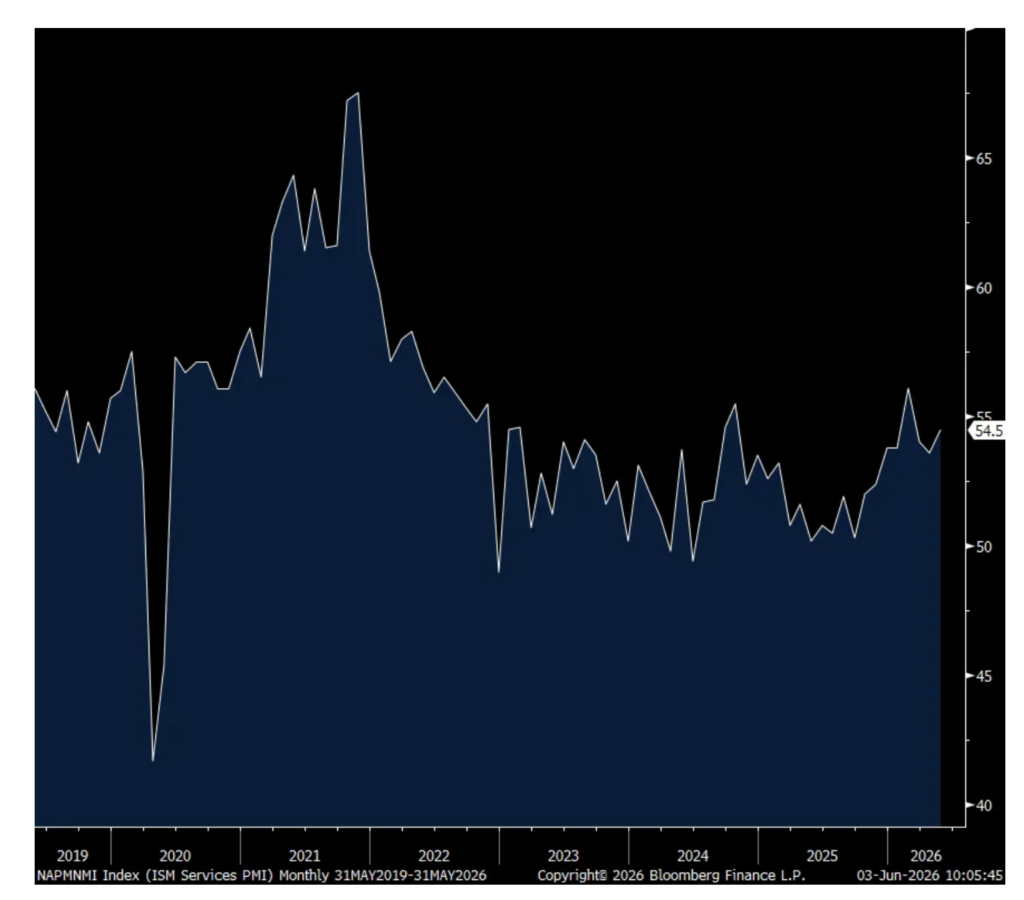

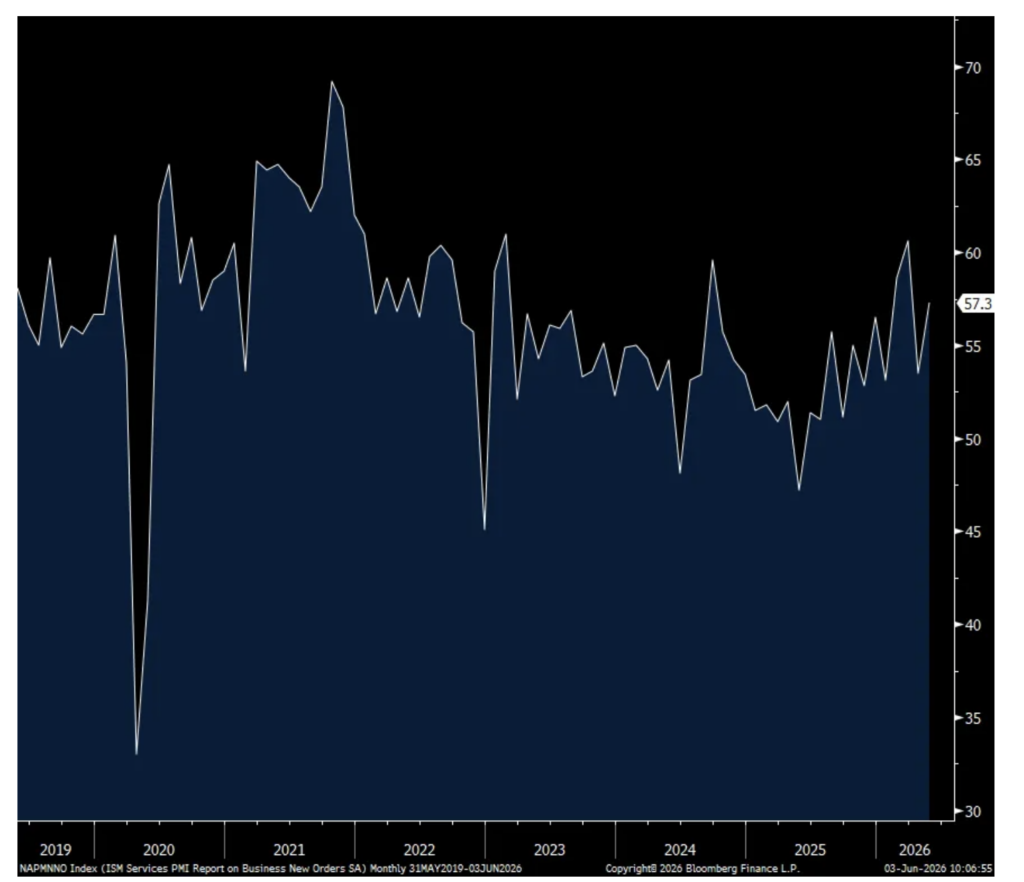

The May ISM services index rose to 54.5 from 53.6 and that was above the estimate of a slight gain to 53.8. New orders rose to 57.3 from 53.5 after falling by 7 pts last month. Backlogs were above 50 for the 4th straight month at 51.3. Likely reflecting the pull forward of ordering I keep hearing about, the inventory component jumped by almost 10 pts to 62.5 matching the highest on record dating back to 1997 with this survey with May 2010 the only other time. I bolded to highlight.

One comment from a respondent of note, “Strong orders fueling need to supply projects as well as replenish stocking inventory.”

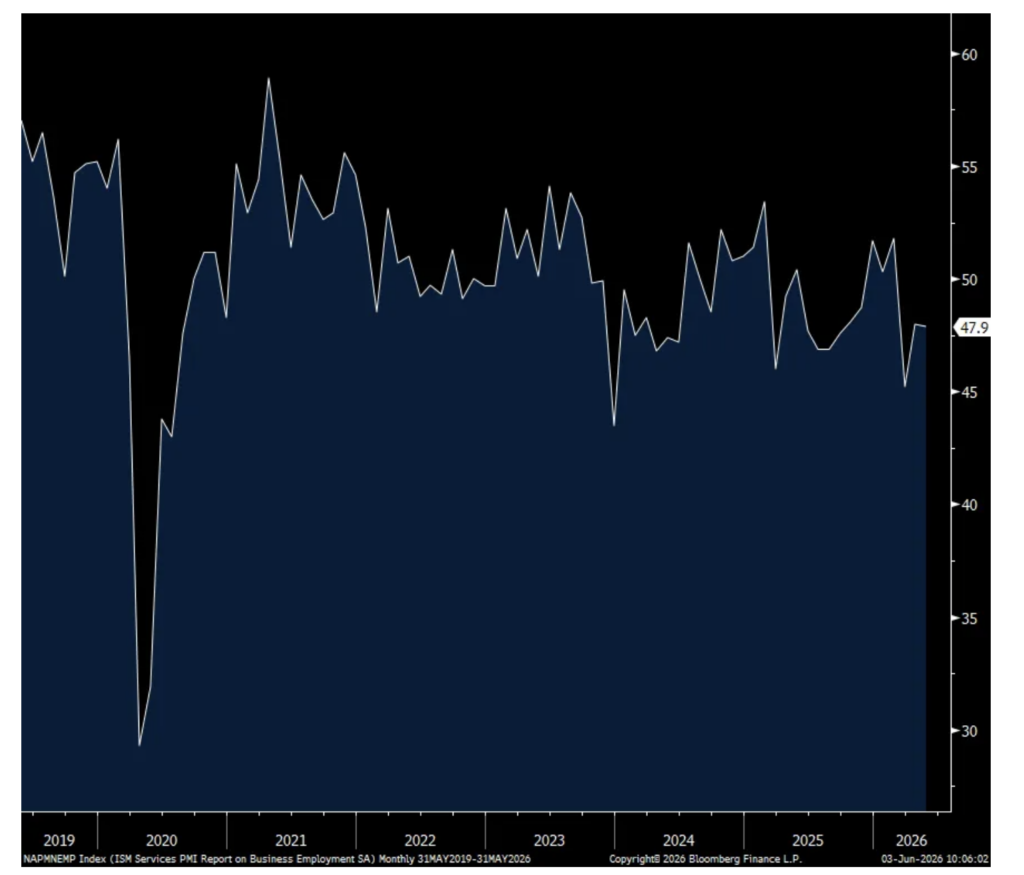

Employment remains a drag coming in at 47.9, little changed m/o/m but below 50 for the 3rd straight month. The ISM said “Respondents commented frequently that their companies had instituted hiring freezes or were not backfilling vacated positions, however, most industries reported that they were holding flat in employment month over month.”

Supplier stress remains but a bit less so as the Supplier Deliveries component slipped to 55.2 from 56.8 and vs 53.9 in February. ISM said, “Comments from respondents include: ‘Freight capacity limitations cited’ and ‘Significant lead times for products like electrical equipment, generators and some mechanical and control systems.’ “

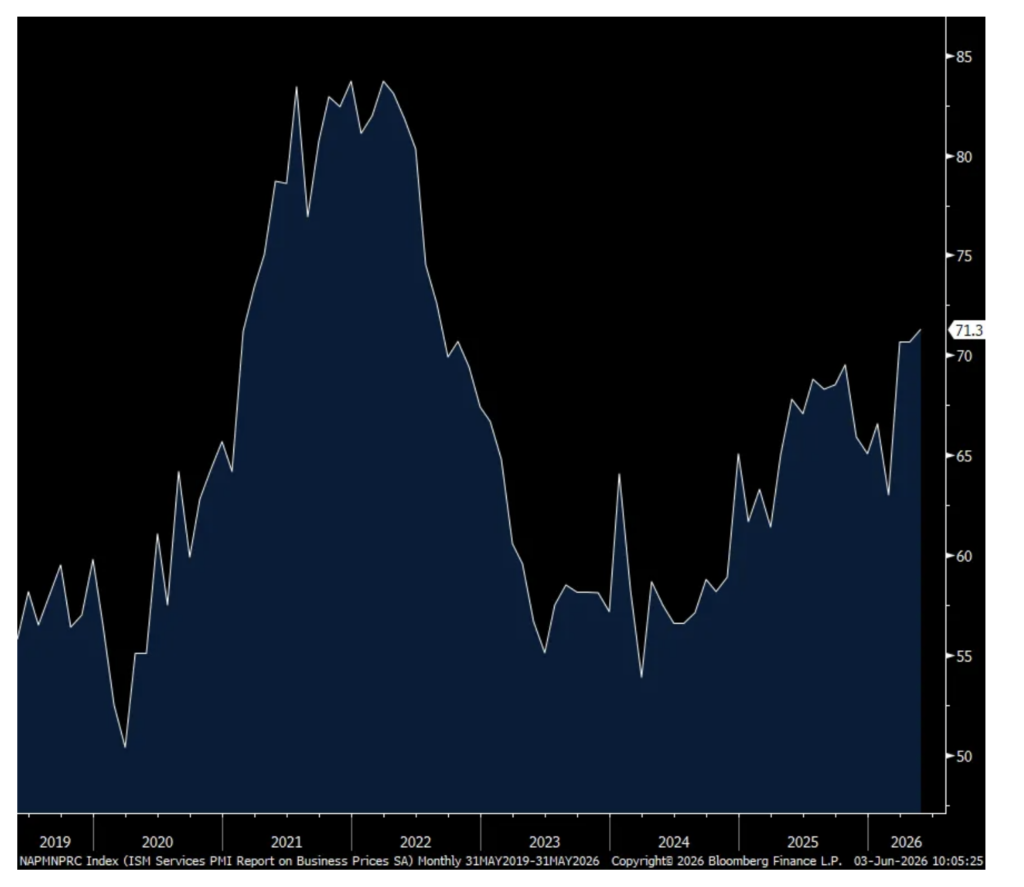

Prices paid remained high, rising by another .6 pts to 71.3 which is the most since August 2022. ISM said, “For the third month in a row, no commodities in the report listed as down in price, with multi month runs of being up in price for aluminum, copper, diesel, gasoline, software licensing and transportation.”

With regards to sector breadth, 17 of 18 industries saw growth in May while just one experienced a contraction, that being in ‘real estate, rental & leasing.’ That compares with 14 industries seeing growth and 3 a downturn.

Bottom line, we know where the strength in the US economy is coming from, AI data centers and all the peripheral beneficiaries, even hotels as workers building the data centers are spending their income, according to Hilton and Hyatt, aerospace & defense, upper income spend and beneficiaries of still massive government spending (defined as a budget deficit as a % of GDP at around 5.5%), particularly healthcare and defense. Here was another respondent comment, “business activity is increasing amid demand for data centers, commercial growth and infrastructure, we are researching increasing generation capacity and new technologies.” And, as stated and seen mostly in manufacturing, the stocking up of inventory is helping too ahead of expected price increases and/or supply issues.

ISM Services

Inventories

Prices Paid

Employment

New Orders

Positions: None.