Peter Boockvar on Shipping, Rents, the Consumer

From Peter Boockvar:

A source of funds/rents, shipping, and the consumer

Global sovereign bond yields are a definite focus but I do want to add another influence in addition to inflation worries, along with concerns with excessive country debts and deficits. That being, sovereign bonds in markets that foreigners own a big piece have been a source of funds as countries bring some money home to manage the energy price/volume shock some are experiencing.

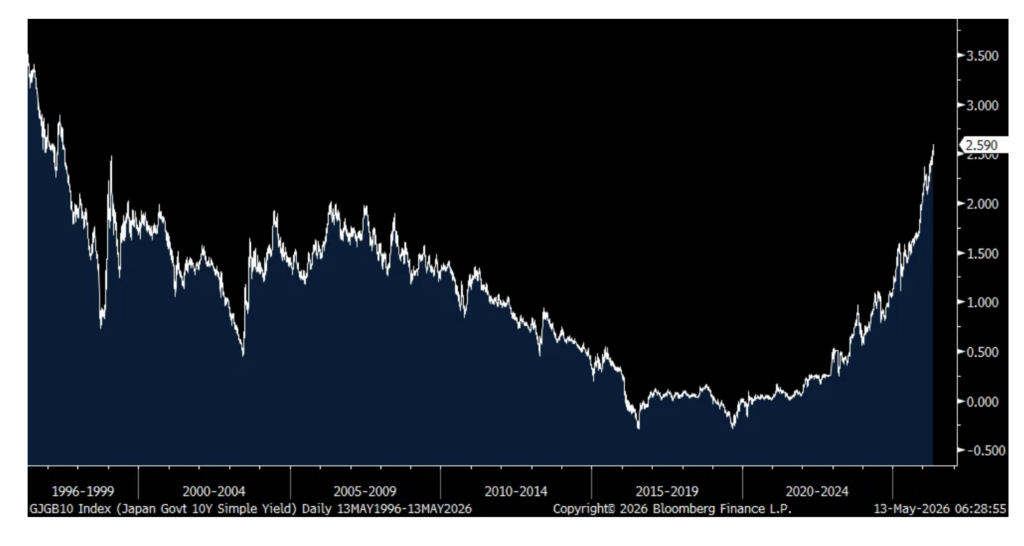

Foreigners own about 30% of the US Treasury market. According to Gemini, foreigners own 77% of the German bund market and about 50% outside the Euro area. Foreigners own about 50% of the French oat’s market. Of the UK gilt market, overseas investors held about 30%. It’s really only the Japanese JGB market that foreigners hold little but bond yields are rising anyway as the long end of their yield curve has taken over monetary policy from the BoJ. The 10 yr JGB by the way closed overnight at a fresh 29 year high, up another 3 bps to 2.59%. And with the Japanese the largest owner of US Treasuries, there is a JGB yield level where that money is going to come back home to the JGB market.

10 yr JGB Yield

We know rents/housing is the biggest component of CPI and I’ve been arguing that any moderation in new rent growth we’re currently experiencing, mostly in overbuilt sunbelt states, is only temporary as there is a sharp reduction in the pace of new supply that will start to show up in higher rents by the end of 2026 and into 2027.

I was at the Sohn Conference yesterday in NYC and heard one presenter pitch Camden Property Trust, a stock we own. It was Leslie Sturgeon from Maynard Capital Management and a key part of her bull case was her 2027 new lease growth estimate of 7% vs the Street which is currently at 1%. Her renewal lease growth rate forecast of 4% is in line with the Street and the combination brings a blended rate of growth of 5% vs the Street at 2%. If she’s right, and I believe she will be, the inflation story will continue on next year.

After hearing from Maersk last week, Hapag Lloyd reported today and said this of note on their earnings call:

With respect to the Middle East, “I think the thing which is a little bit special about that is while the conflict itself is geographically quite isolated and as such does not impact global flows all that much, the effect it has on costs, of course, have a global effect because with the surge of energy prices, we have seen significantly higher costs hitting us. I think if we look at what we have today, then we definitely look at $50, $60 million extra costs every week.”

“Of course, we try to pass that on, similar to when you go to the petrol station and you also have to a higher fuel price, but clearly that puts pressure on our business. As far as the militia is concerned, we still have a number of ships stuck there and we cannot go in and out of the Strait at this moment in time.”

Under Armour got roughed up yesterday, a stock we still own but still like believing in the turnaround that’s happening under the surface. A few things of note from them:

“as we look ahead to fiscal ‘27, we do expect to stabilize with revenue down slightly. That outlook reflects both continued consumer uncertainty and the deliberate choices we’re making to reshape the business. We are prioritizing revenue quality over volume, strengthening the foundation and positioning the company to return to growth with stronger profitability and a more consistent brand expression.”

North America sales were down but “In EMEA, the business remains solid and continues to serve as a stable anchor for the brand.” Sales are rising too in APAC with a particular focus on China.

They got hit hard from tariffs but are expecting some refunds. “This is a brand that has been navigating tariffs, softer consumer demand and supply chain disruption” in the Middle East.

Positions: None.