This is Part 5 of a multi-part discussion of the markets (Read Part 1 here, Part 2 here, Part 3 here and Part 4 here) …

Now, let’s wrap it up…

Bottom Line

“It is always well to accept your own shortcomings with candor but to regard those of your friends with polite incredulity.”

– Russell Lynes

As noted in a previous post It’s a Mad, Mad, Mad, Mad Investment World.

Today’s commentary shares my views and tries to attach empirical evidence and observations that support a skeptical market outlook.

I continue to be reminded of Warren Buffett’s quote:

“What the wise do in the beginning, fools do in the end.”

With the same intended message, Barton Biggs was more colorful when he said:

“A bull market is like sex. It feels best just before it ends.”

Citigroup’s CEO Charles Prince — in July 2007, only months before The Great Financial Crisis (and historic market decline) — had a different view (as reported in an interview he had with The Financial Times):

“When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.”

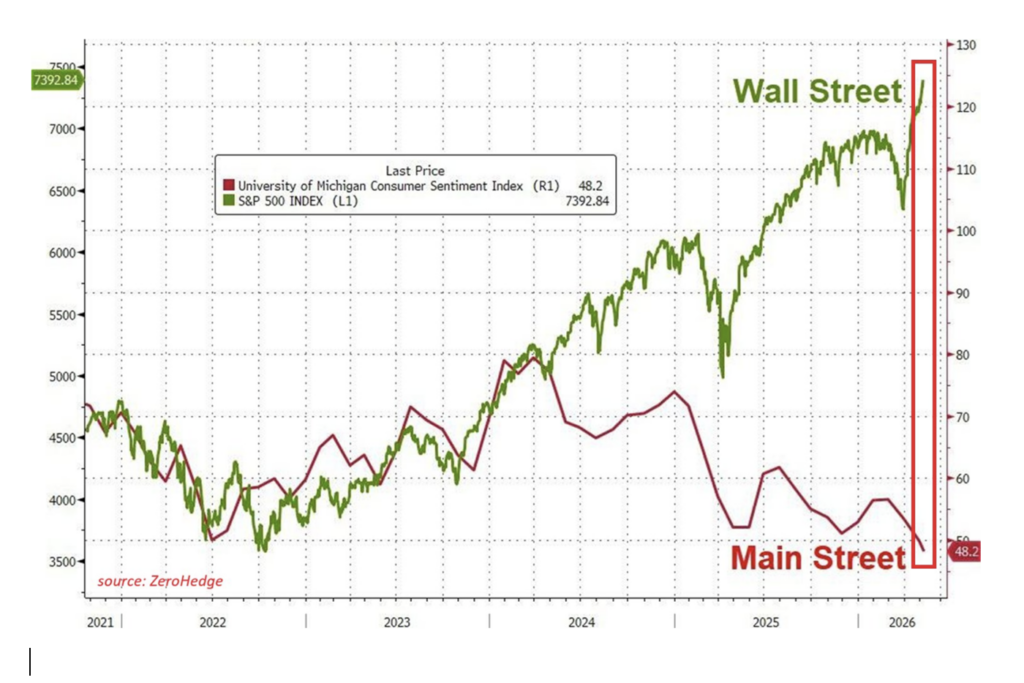

That said, with the S&P 500 making an all-time record in May — and despite my protestations — it is abundantly clear that, for now, neither the markets nor most market participants (human and machine) share my outlier, non-consensus and ursine outlook.

Market participants are still at the bacchanal — while I remain celibate.

Position: None