Tweet of the Day (Part Four)

Position: None

Position: None

Potential “outside day” for $MS and $GS.

Both made all-time highs and are now lower on the day.

Position: Short MS (M)

I shorted more $GRNY at $27.32.

Position: Short GRNY (M)

From Peter Boockvar:

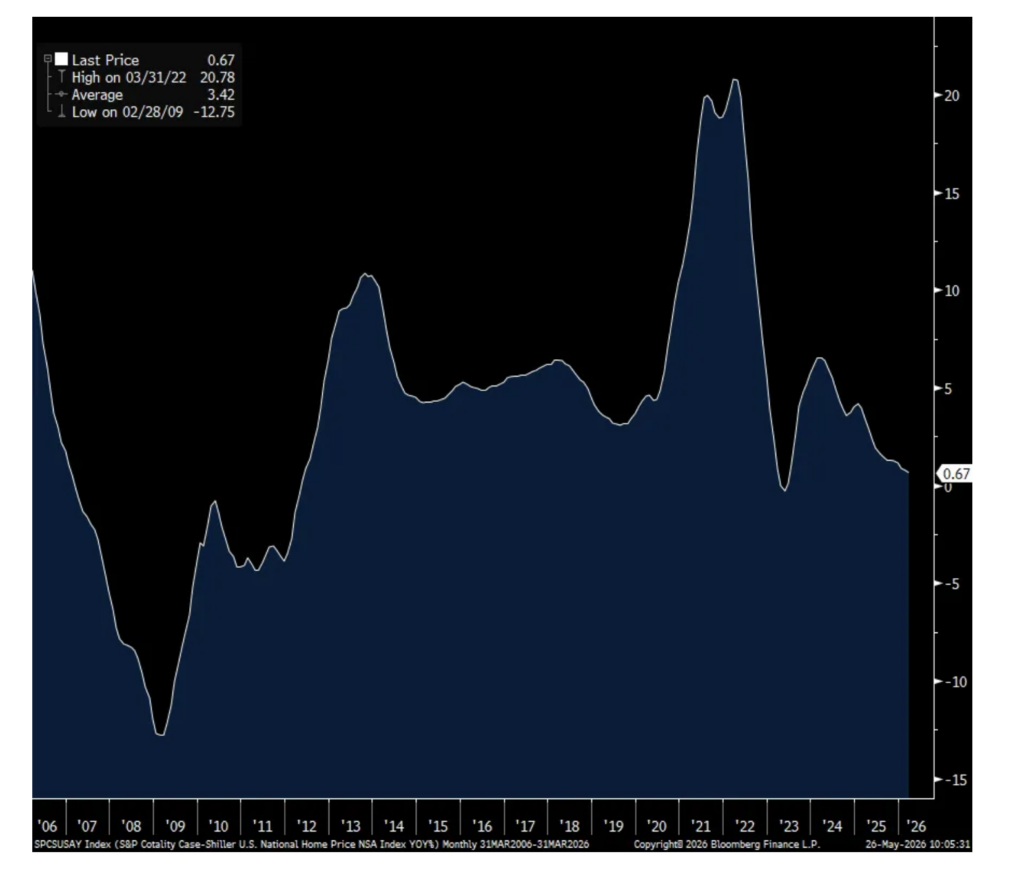

Home price growth in March (so somewhat dated and doesn’t reflect recent inflection up again in mortgage rates) rose .67% y/o/y, vs .75% in February. That’s the slowest pace since June 2023 and I think the moderation in price increases is a good thing as it allows wage growth to catch up and hopefully improve affordability and the chances of a rise in transactions that is still hovering around 30 yr lows.

The overheated and now a bit over supplied sunbelt states are seeing the biggest weakness with home price declines in Tampa, Phoenix, Las Vegas, Atlanta and Dallas. Throw in Denver also on the extra supply side. Weakness was seen too in LA and Seattle.

On the flip side, NY, Chicago, Cleveland and Boston saw the biggest price increases and that have more limited supply.

S&P Global said “More than half of the 20 major US housing markets recorded y/o/y price declines in March, reflecting a broadening and deepening housing slowdown.”

S&P Cotality Case-Shiller Home Price index y/o/y

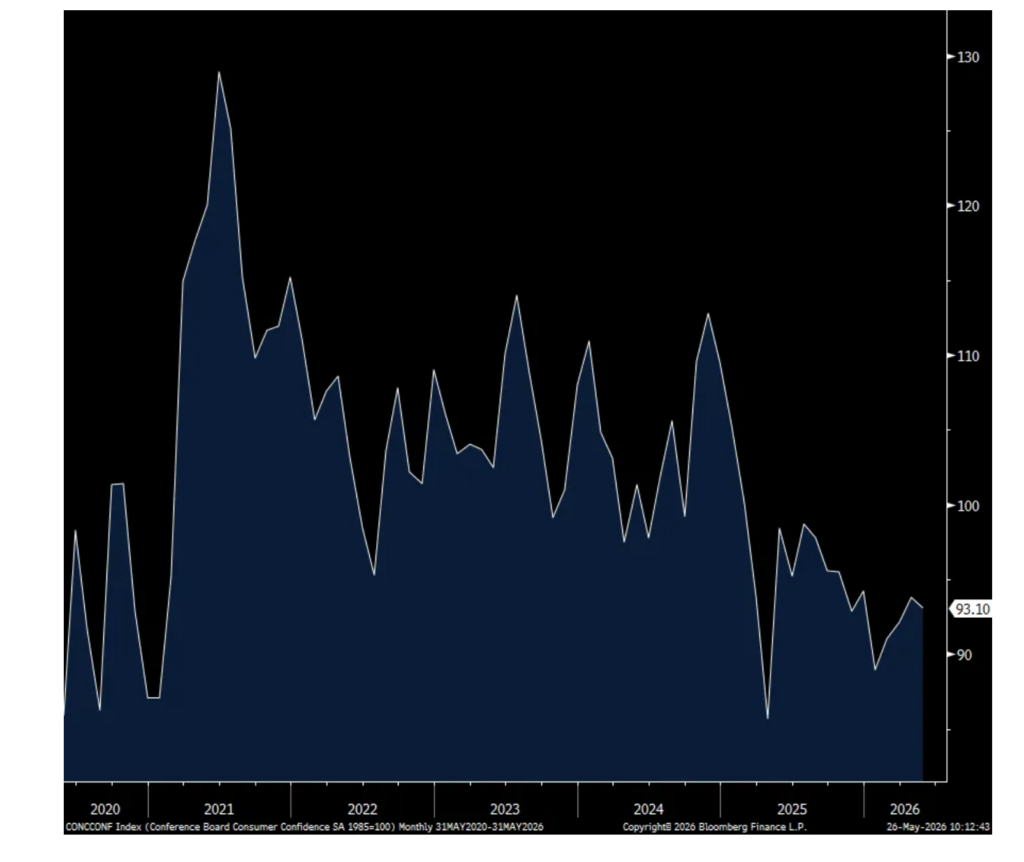

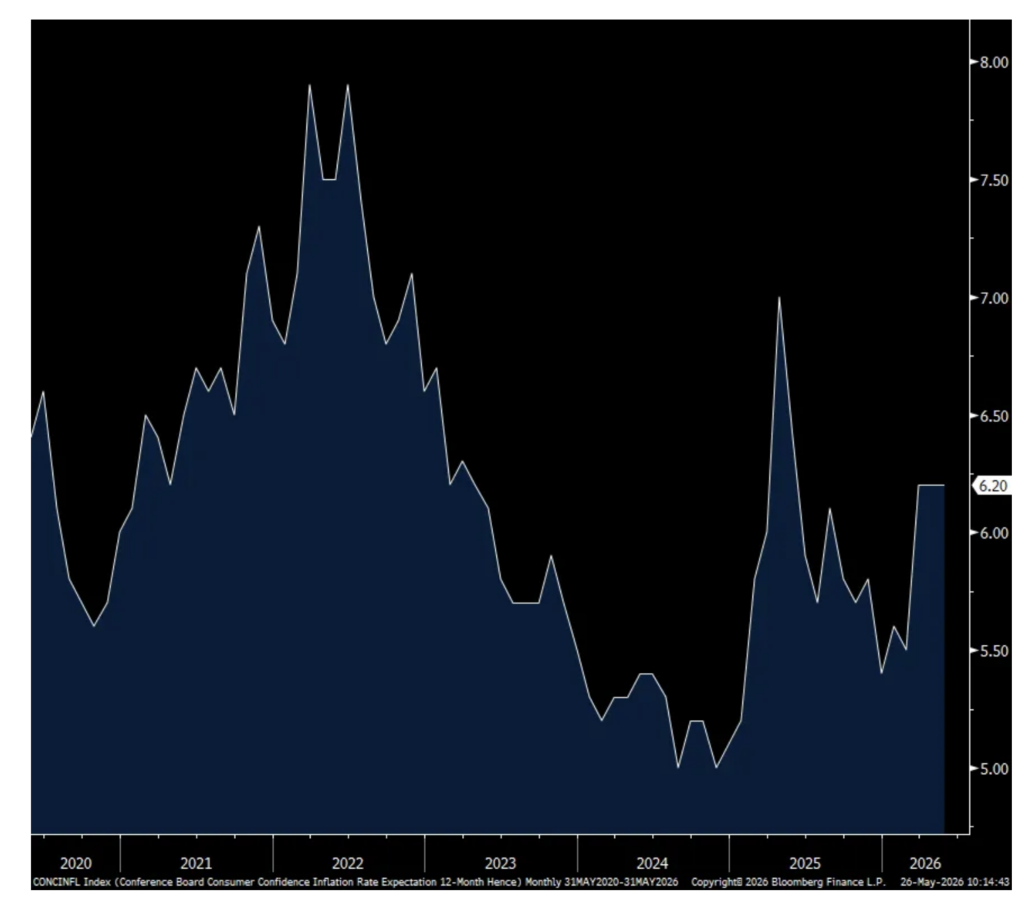

As measured by the Conference Board, their consumer confidence index in May fell slightly to 93.1 from 93.8 and vs 92.2 in March and 91 in February. The internals were mixed as the Present Situation fell to a 3 month low but the Expectations component rose 1 pt m/o/m to a 5 month high. One year inflation expectations was at 6.2% for a 3rd month and that stays at a one year high.

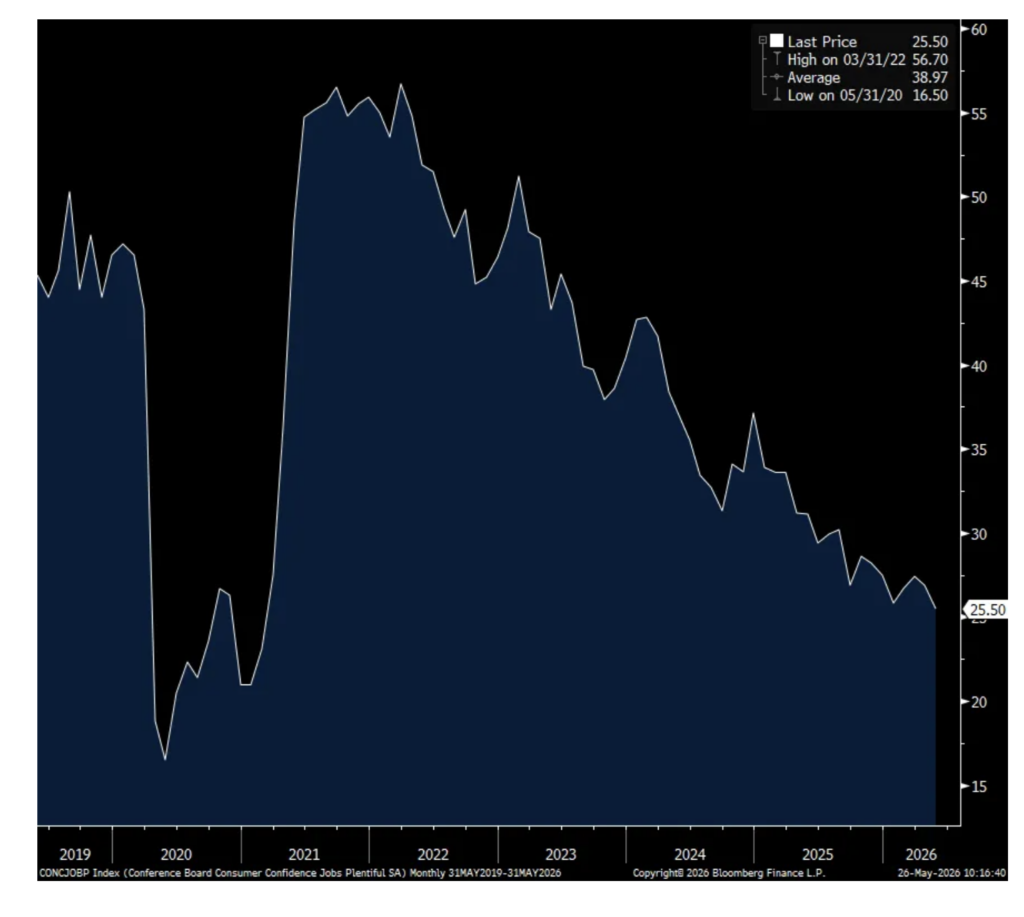

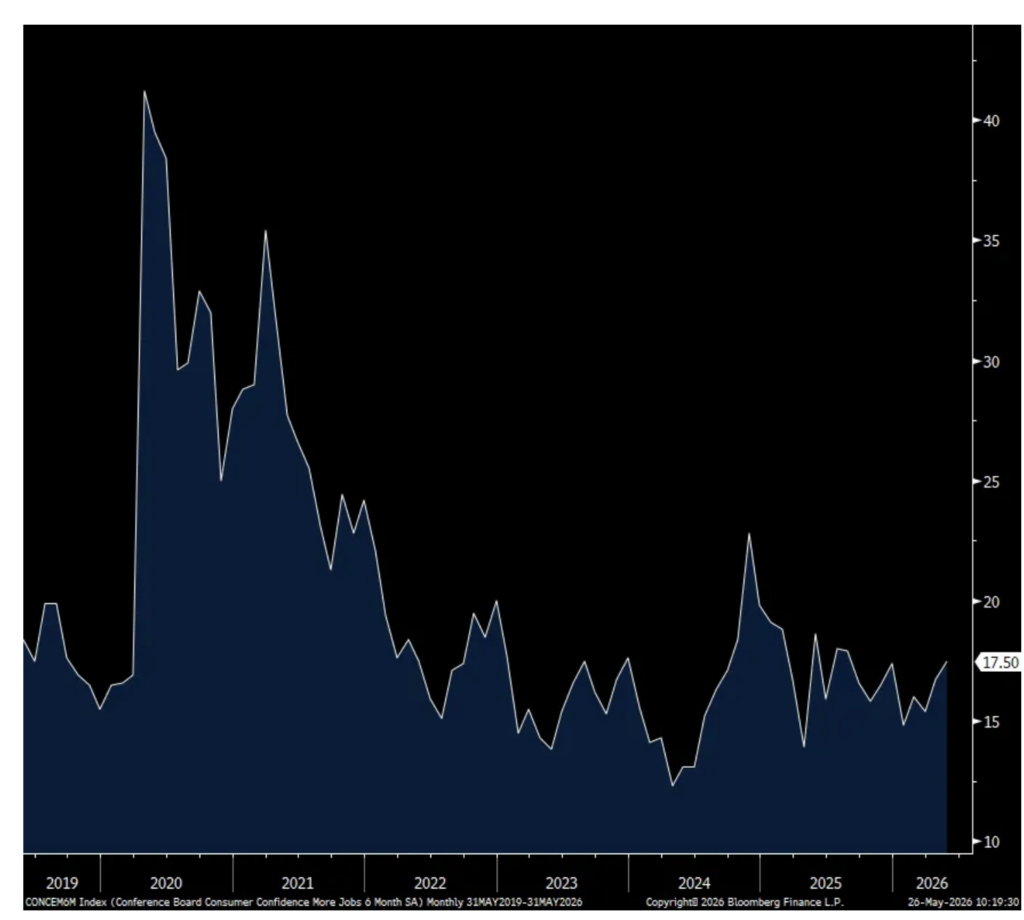

The answers to the labor market questions were mixed as those that said jobs were Plentiful fell to the lowest level since February 2021 but those that said they were Hard to Get declined to the least since last October. And helping to boost the overall Expectations question, the 6 month outlook for ‘more’ jobs rose to the highest since last August though is still bouncing along the bottom as seen below. Expectations for income growth also improved but did too for those that expect it to decline (a fall in those that expect it to stay the same).

Spending intentions pulled back after the rise in April, particularly for autos and vehicles. With respect to spending on services, the Conference Board said, “Consumers planning more spending on services over the next six months shifted from “yes” and “maybe” to “no” in May. Future spending plans on services were mixed. Consumer spending trends in 2026 remained focused on “cheap thrills” and necessary services, but there was some increase in demand for discretionary services like personal travel, fitness, amusement parks, and gambling. Among all service categories, restaurants/bars/take-out, streaming/internet/mobile services, and beauty and personal care, remained among the top three spending targets.” And, “Travel intentions for six months ahead ticked up in May, and consumers continued to favor domestic destinations over international travel.”

The Conference Board said what we’re well aware of in terms of the bottom line, “Consumer confidence edged downward in May as the inflationary impacts of the war in the Middle East intensified…Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism in May. References to prices and oil and gas increased in frequency for a second consecutive month, while mentions of war, geopolitics, and conflict remained elevated – likely signaling consumers’ underlying concerns about the inflationary impacts of the war in the Middle East on their wallets.”

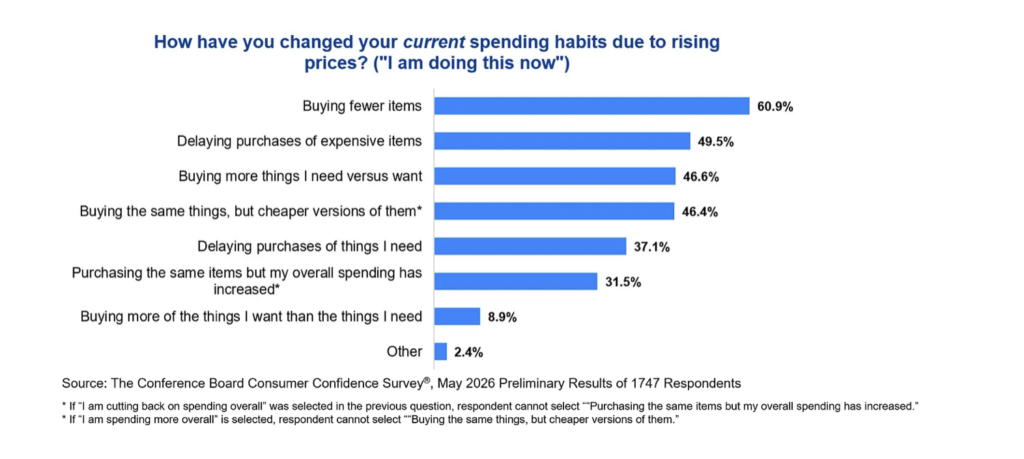

Finally, the Conference Board had some special questions for the respondents in May and summarized by them with this:

· “Two-thirds of consumers cited cutting back on spending overall due to rising prices, as of May

· Most who are cutting back bought fewer items and delayed expensive purchases

· Many who said they are delaying purchases of items they want rather than need, plan to buy them in the next six months

· Consumers planned to economize on clothing and footwear, hobby items, and games/toys”

Consumer Confidence

One yr Inflation Expectations

Jobs Plentiful

Expect ‘more’ jobs in coming 6 months

Positions: None.

Dougie Kass

Big reversal GS/MS

Dougie Kass

Aggressively shorted MS today, now medium sized.

Dougie Kass

Buying MSOS and individual weed stocks aggressively.

Dougie Kass

Position: Long CURLF (VS), VRNO (S), GTBIF (VS), MSOS (M); Short MSOS (M)

Its that time again.

11 a.m. with Market Call (with Carter, Liz, Guy and Dan) – where transparency and honesty are the foundation of the podcast and the watchwords of their investing/trading faith.

Run, don’t walk to watch.

I am!

Positions: None

With S&P cash up by over 60 handles, I am becoming aggressive on my index shorts:

* $SPY $751.74

* $QQQ $730.16

Position: Short SPY (M), QQQ (M)

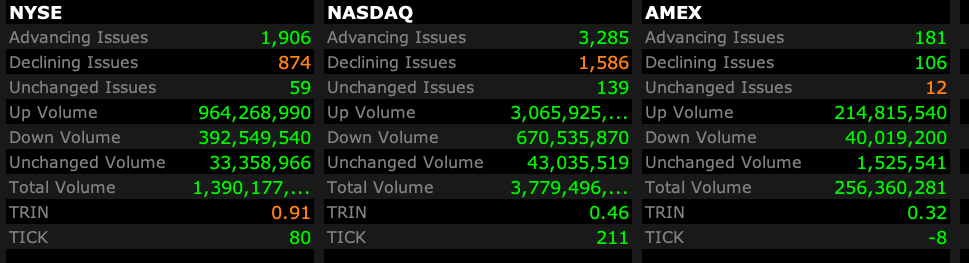

– NYSE volume 16% above its one-month average;

– Nasdaq volume 16% above its one-month average;

– VIX index: up 1.44% to 16.94

Positions: None.

* But for how much longer?

* Bottom line: It’s not different this time…

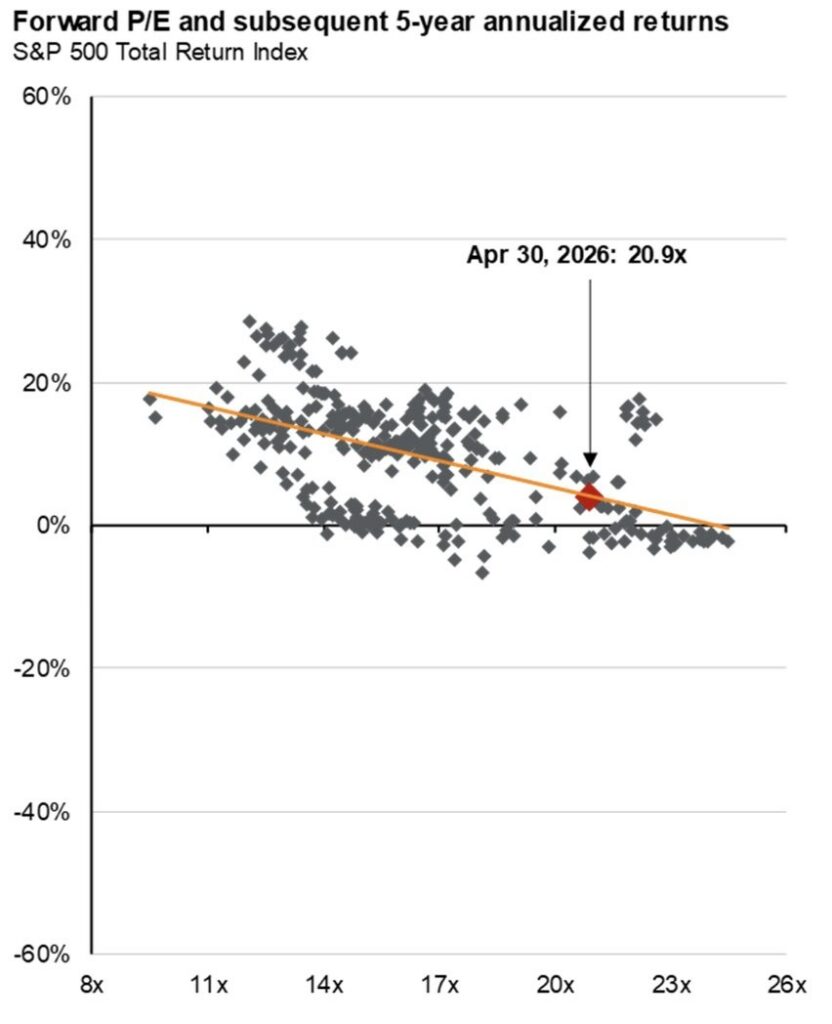

For nearly three years the markets and its participants have ignored elevated valuations.

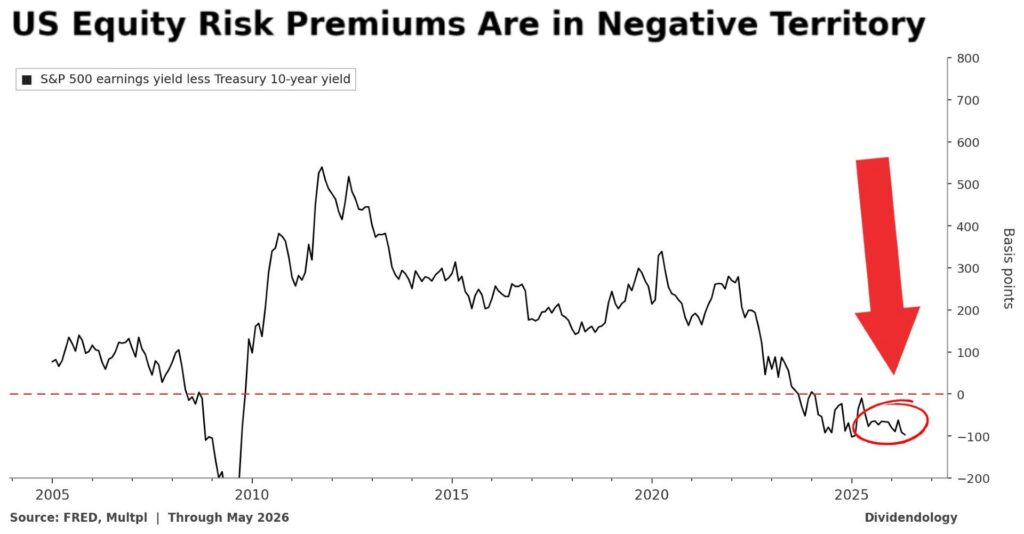

How much longer can the S&P 500 and the other major indices deliver upside when price-earnings multiples and equity risk premiums are in the 95th percentile or higher?

With consensus (I think overly optimistic!) 2026 S&P EPS at $330/share, the senior average trades at 23x and the equity risk premium is negative.

On projected 2027 S&P EPS consensus of $375/share (I think overly optimistic as well) the S&P trades at 20.5x and the equity risk premium is only at 50 basis points, both in the 93rd percentile.

The steady decline in the equity risk premium is a metric I pay very close because. Historically, it has been an excellent indicator future investment returns…

My focus on the ERP has contributed importantly to my wrong-footed market view and a missed opportunity set on the long side.

Let’s examine the equity risk premium, which is the difference between the S&P earnings yield (the inverse of the P/E ratio) and the risk free rate (the 10-year Treasury note yield is typically used):

The equity risk premium tells us how much excess return investors are being paid to own stocks over a risk free Treasury bond.

Historically, equities typically offer a three-to-four percent premium over Treasuries. Such a premium makes sense because it compensates investors for volatility, drawdowns and uncertainty.

Right now, according to the chart above, the investor is being paid negative in equities vis a vis bonds. The ratio is saying that holding bonds is more risky than owning stocks — this is a radical notion, at an extreme! Again, this means:

1. Investors are not being paid extra to take on risk in stocks.

2. Stocks are offering similar or worse “yield” than bonds.

3. Valuations are materially stretched relative to interest rates.

Stated simply, this means that holders of equities are taking more risk for less reward (than bonds). When this has happened in the past (most notably during the dot-com bubble and leading up to The Great Recession in 2007-09), forward returns have been somewhere between non-existent and negative:

It is hard to understand why stocks have been impervious to elevated valuations (a record high in overvaluation in both the Buffett Indicator and a near record in Shiller’s CAPE ratio), as well as an equity risk discount.

One answer is the dominance of passive products and strategies that worship at the altar of price. They know everything about price and nothing about value.

Other explanations are the euphoria in AI and the fear of missing out (FOMO).

Nonetheless, excessive valuations, excesses and the idea of a “new era” are nothing new — we have seen these at the top of other cycles (for reasons of overenthusiasm/heated speculation).

Finally, it is our strong view that the components of the equity risk premium suggest even more of a discount as 2027 EPS estimates come down and interest rates likely rise.

Let’s not forget when Berkshire Hathaway’s ($BRK.A) ($BRK.B) shares were suffering in late 1999 and many were questioning Warren Buffett’s investing philosophy (as they are currently with his near $400 billion cash hoard) — right before a more than -80% drawdown in the Nasdaq.

To me, it’s not different this time.

I continue to choose the weighing machine over the voting machine.

Position: None