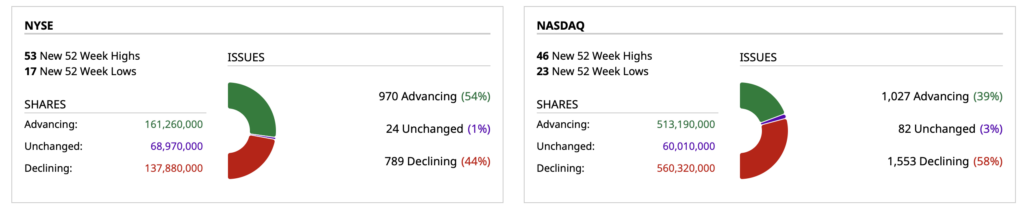

Late Morning Market Stats and Charts

– NYSE volume 10% above its one-month average;

– Nasdaq volume 5% below its one-month average;

– VIX index: up 0.19% to 16.08

Positions: None.

– NYSE volume 10% above its one-month average;

– Nasdaq volume 5% below its one-month average;

– VIX index: up 0.19% to 16.08

Positions: None.

From Peter Boockvar:

The data center buildout is keeping the US economy afloat, its beneficiaries are continuously taking the stock market to new highs, and the technological advancements are exciting but we are being reminded again how expensive and capital heavy it all is, especially for the major hyperscaler spenders.

Google/Alphabet seems to have all the building blocks to monetize its development of Gemini and further grow its cloud business but it sure is costly. This company generated about $73 billion of free cash flow in both 2024 and 2025, bought back $62 billion of stock in 2024 and $46 billion in 2025 and spent $52.5 billion on CapEx in 2024 and $91.4 billion in 2025. Now, they are raising $80 billion of equity, just the second equity raise since it went public in 2004, as they sold some shares in 2005, as they need help financing $186 billion of expected CapEx in 2026 and almost $250 billion forecasted for 2027 and as their free cash flow is expected to decline this year to ‘just’ $21 billion and $16 billion expected in 2027. Back in February, they raised $32 billion in debt sales which as of 3/31/26 took their long term debt to $90.5 billion when including lease liabilities, that is up from $22.5 billion on 3/31/25. Asset light no longer.

Further quantifying all the CapEx on the data center buildout, Chris Wood at Jefferies had this chart last week which dates back to post WWII. It speaks for itself the size at which companies are investing. None of this is to say it all doesn’t work out from a monetizable perspective for the builders and the technological wonders for its users, aka, the rest of us, but just to highlight, again, the ever-rising costs of it and its current tremendous economic contribution.

Competing with Dell, HP Enterprise reported a blowout quarter too and its stock is responding in kind to the upside. They said of note:

“Demand was even stronger than revenue growth. Orders more than doubled, significantly outpacing revenue, resulting in a record company backlog. Customer investments in agentic AI and AI inferencing accelerated. We also saw broad based demand strength across the portfolio, driven by ongoing investment in compute infrastructure modernization, unstructured storage data growth, and private cloud adoption for AI.”

“Sequentially, revenue grew 15%, reflecting higher average selling prices within our server business, driven by ongoing DRAM and NAND inflationary costs and supply constraints. We continue to work with our partners to secure long-term agreements while executing the pricing actions we discussed last quarter.”

While Dell talked about seeing some pull forward of ordering, HP is saying they don’t. “And customers, when you think about budgets, obviously they are challenged because of the price increases we have seen driven by the cost of commodities. But I can tell you, we have not seen any pull-in. We don’t see a cliff. And in many ways, I think customers are prioritizing getting access to technology now faster than ever before because nobody wants to be left behind when it comes down to deploying AI.”

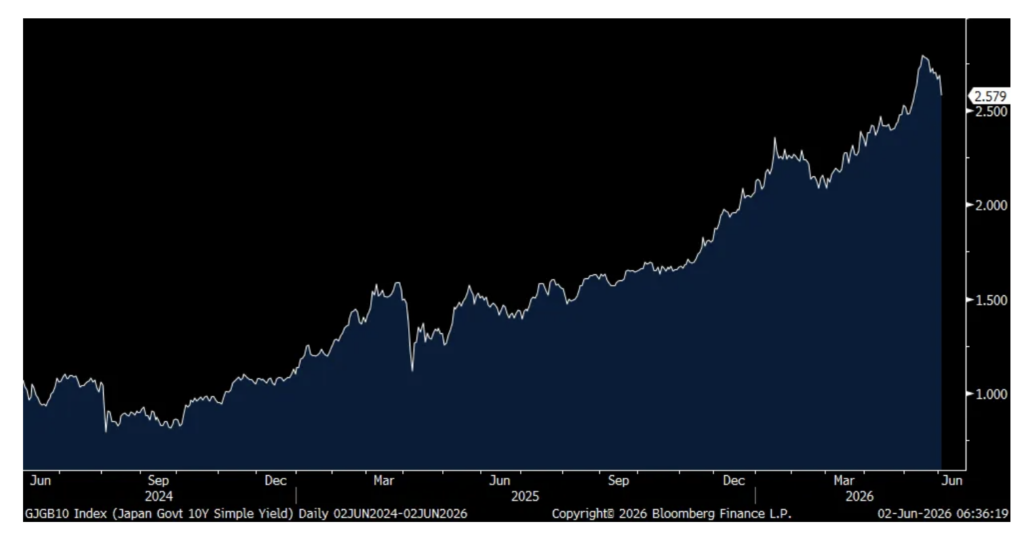

There was a big move lower in JGB yields overnight with the 10 yr in particular falling by 11 bps to 2.58% after a good 10 yr auction was conducted. The bid to cover of 3.53 was well above the previous 12 month average of 3.35, though down from 3.90 in May. With the yen back to 160 vs the US dollar, we watch to see if this market test will trigger another round of Japanese government intervention. I think all they need is another rate hike in a few weeks but we’ll see if it happens or not.

South Korean bonds rallied too even after they reported May CPI that rose 3.1% headline y/o/y, two tenths more than expected and a core rate gain of 2.5% which was 3 tenths above the estimate.

10 yr JGB Yield

After seeing individual European country inflation stats over the past few trading days, the May Eurozone CPI was higher by 3.2% y/o/y and 2.5% at the core. The headline was as forecasted but the core rate was one tenth above and both compare with 3% and 2.2% in April. Of note, services inflation accelerated to a 3.5% y/o/y increase, matching the quickest since April 2025 while non-energy industrial goods prices rose .9% y/o/y, still benign but that is the fastest rate of change since Q1 2024. As the data was basically as expected and we saw the big JGB yield drop, European sovereign bonds are rallying across the board with yields lower which in turn is helping US Treasuries with yields down. The ECB is expected to raise rates this month as REAL rates are now well negative.

Eurozone CPI y/o/y

Positions: None.

With S&P cash -9 handles I am adding to Index, ($GRNY) and ($JOET) shorts.

Positions: Short SPY M QQQ M GRNY M JOET S

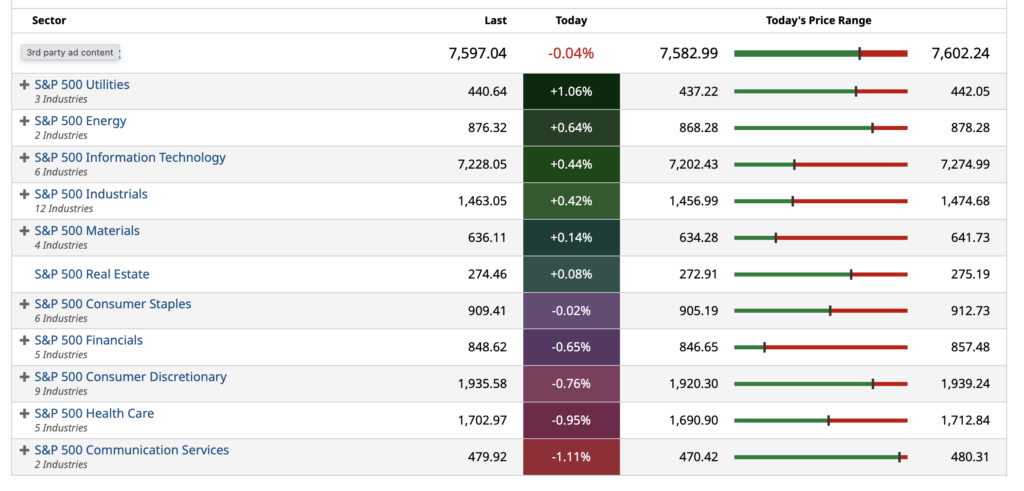

Chart from 9:37 a.m. ET.

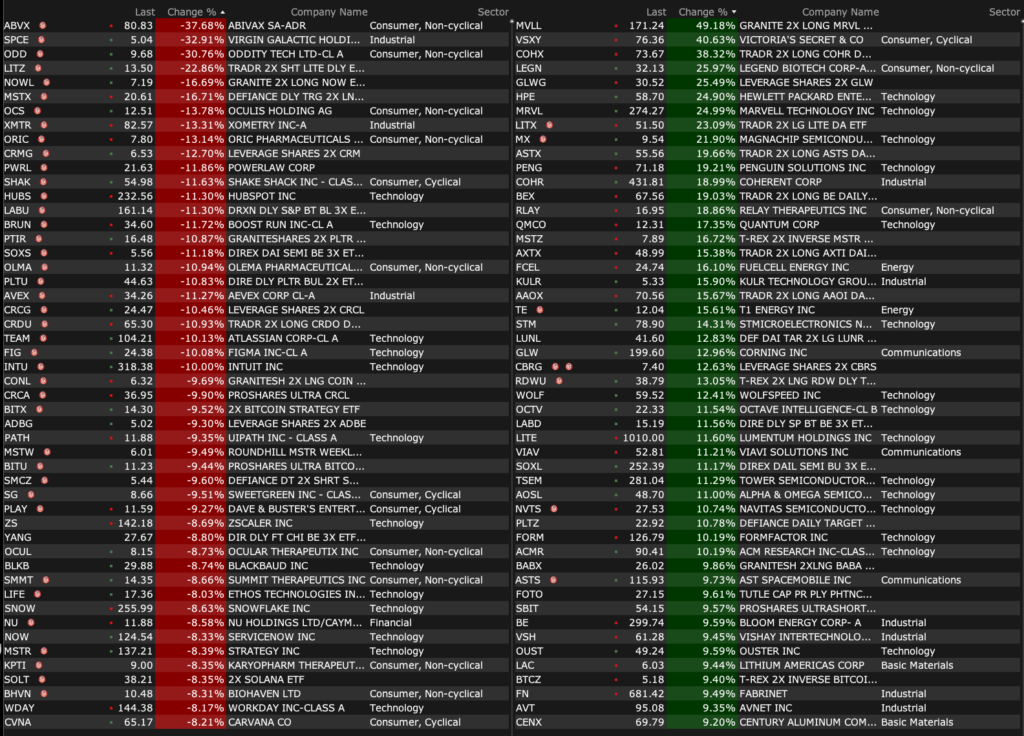

… a bit late, but still here:

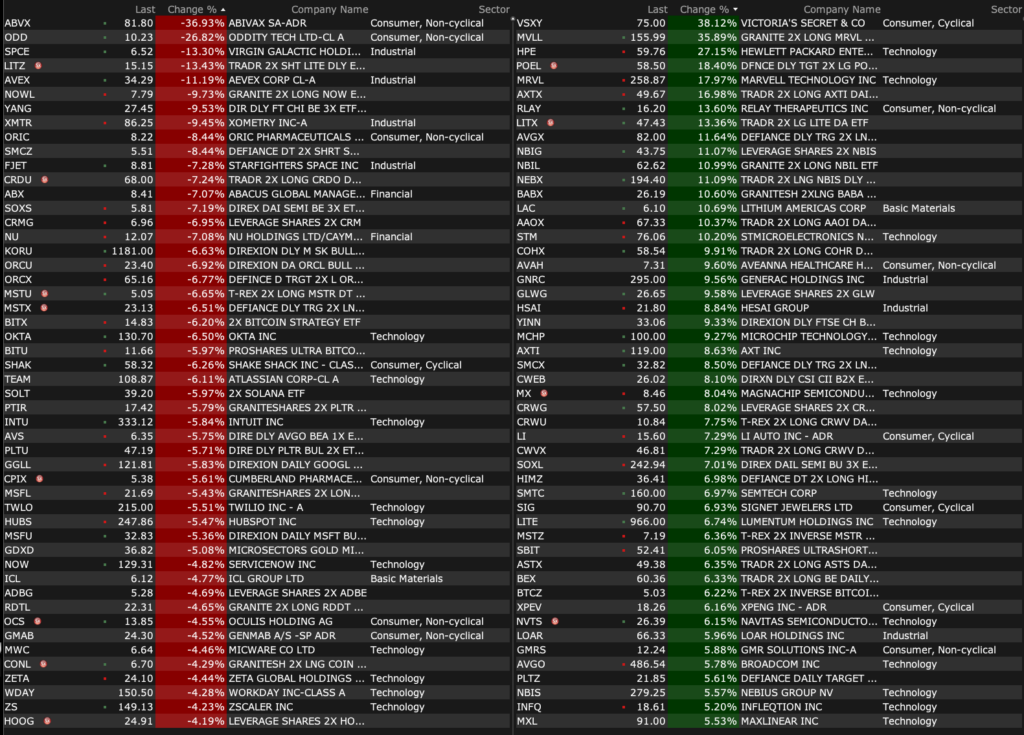

-BJDX +165% (partners with Argonaut Manufacturing Services to support Symphony platform)

-VSXY +32% (earnings, guidance)

-HPE +29% (earnings, guidance; appoints Christopher Hsu of Elliott Investment Management to Board of Directors)

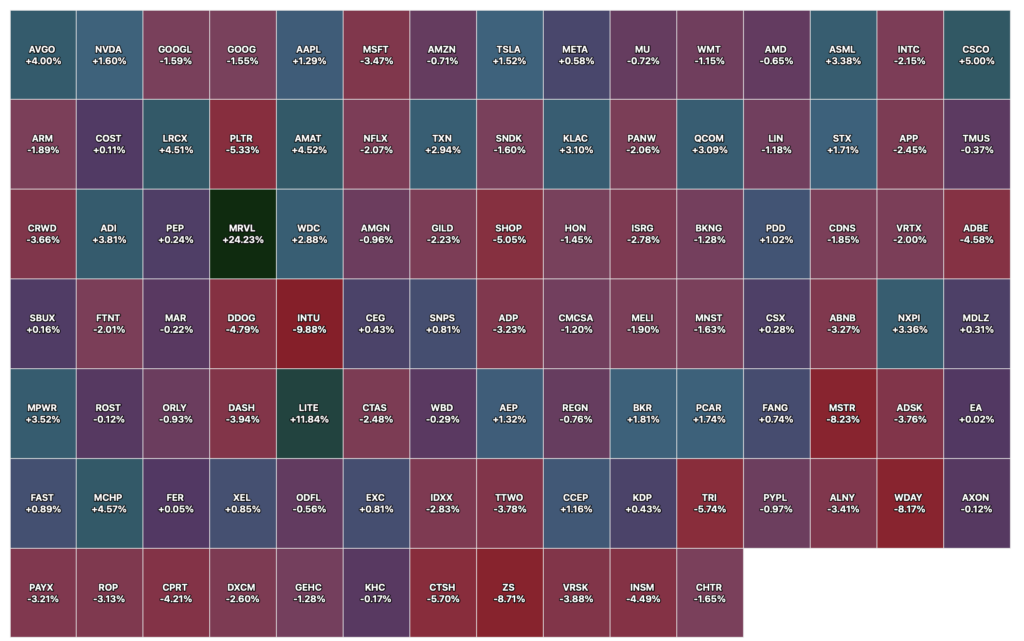

-MRVL +18% (Nvidia’s CEO says Marvell could be next to join $1T market cap club)

-CTRN +15% (earnings, guidance)

-CAMT +11% (receives $55M multi-system order and $50M+ Hawk system orders for 2027 delivery)

-GNRC +10% (signs global supply agreement with leading hyperscale data center operator to provide backup generators)

-STM +9.9% (raises data center revenue ambition; now about $1B in 2026 (prior nicely above $500M), could double in 2027 (prior well above $1B))

-MCHP +8.9% (Data center solutions unit revenue expected to grow 65% in 2026 to about $500M; Announces price increases)

-SIG +5.8% (earnings, guidance)

-DG +5.5% (earnings, guidance)

-SMCI +4.1% (showcases next gen AMD Helios rack-scale platform at Computex)

-TRIP +2.2% (Wedbush, Inc. Assumed TRIP with Outperform, price target: $19)

-HKIT -62% (raises $8M in registered direct offering of 4.0M shares at $2.00/shr)

-FULC -51% (discontinues pociredir for sickle cell disease; explores strategic alternatives)

-ABVX -36% (reports Phase 3 ABTECT maintenance trial data in ulcerative colitis)

-CELC -24% (reports detailed efficacy and safety results in PIK3CA MT cohort for Phase 3 VIKTORIA-1 gedatolisib regimens vs alpelisib plus fulvestrant)

-ODD -23% (earnings, guidance)

-XMTR -9.8% (prices previously announced $225M sale of 2.65M shares at $85/share)

-LPTH -9.4% (prices registered direct primary and secondary offering of Class A common stock; 7,142,800 shares at $14.00/share)

-NU -7.1% (appoints Rob Livingston CFO)

-SHAK -6.8% (cuts guidance)

-INTU -6.4% (Goldman Sachs Cuts INTU to Sell from Neutral, price target: $276 from $519)

-SNOW -3.6% (profit taking)

-CRDO -3.3% (earnings, guidance)

-GOOGL -2.8% (authorizes proposed $80B equity capital raise to expand AI infrastructure and compute)

Positions: None.

Jaw4860

15m ago

Doug ,You quote Marcus and others ,What are their track records ?

DDougie Kass

just now

they are research analysts not running portfolios

i believe, unlike some, that my job is to provide contrarian views/analysis – ergo gary marcus tweets/columns

others feel differently

bullish views dominate the markets (wall street, fin tv ,etc.), thoughtful outside of consensus, provides food for thought for investors and traders considering sectors and weighting those sectors

warren buffett has done poorly in the last 5-10 years vs the markets – so should i stop quoting him?

druckenmiller, the goat, is on a bad streak – should we stop listening to him?

lee is having a rough year – are his views worthwhile?

considering pros and cons, creating a ledger on ideas is reasonable

if we confided the dialogue and discourse to those who are right… well, that is sub optimal

Positions: None.

11:00 a.m.: Treasury Announces a 4, 8 and 17 Week Bill Auction;

11:00 a.m.: Treasury buyback announcement (liq support); 1

1:30 a.m.: Treasury hosts a $75B 6-Week Bill Auction

8:30 a.m.: Fed Bank of Cleveland President Hammack (Voter) gives remarks and participates in conversation on monetary policy co-hosted by the Cleveland Fed, the City Club of Cleveland, the Greater Cleveland Partnership, and the 50 Club of Cleveland, Cleveland, OH

Positions: None.

Positions: None.

Positions: None.