The Market Bacchanal Rages On — While I Remain Celibate

This is Part 1 of a multi-part discussion of the markets…

* Investors are ignoring a number of clearly defined and intensifying fundamental and valuation headwinds

* Investor sentiment and expectations are inflated — market risks are being underappreciated

* Equities remain overvalued — perhaps materially so

* The stock market is a church with a casino attached to it — the casino has grown much more active in recent months

* It feels like deja vu all over again

The magnitude and strength of the recovery in the major indexes during the past month have been anathema to me (and to others who have a taste for value and don’t have a momentum-based orientation). The size and the rapidity of the market’s rally (especially since March) have likely been momentum-driven (due in part to market structure changes over the last decade in which passive products and strategies have dominated the investment landscape).

This backdrop of momentum based machine-driven dominance — in which buyers buy strength (and, ultimately, sellers sell weakness) — has, in turn, led to a great deal of fear of missing out (FOMO). These factors and others (including a strong belief in an AI productivity miracle) have contributed to a record pace of recovery, producing another “V”- type rally from the March 2026 lows.

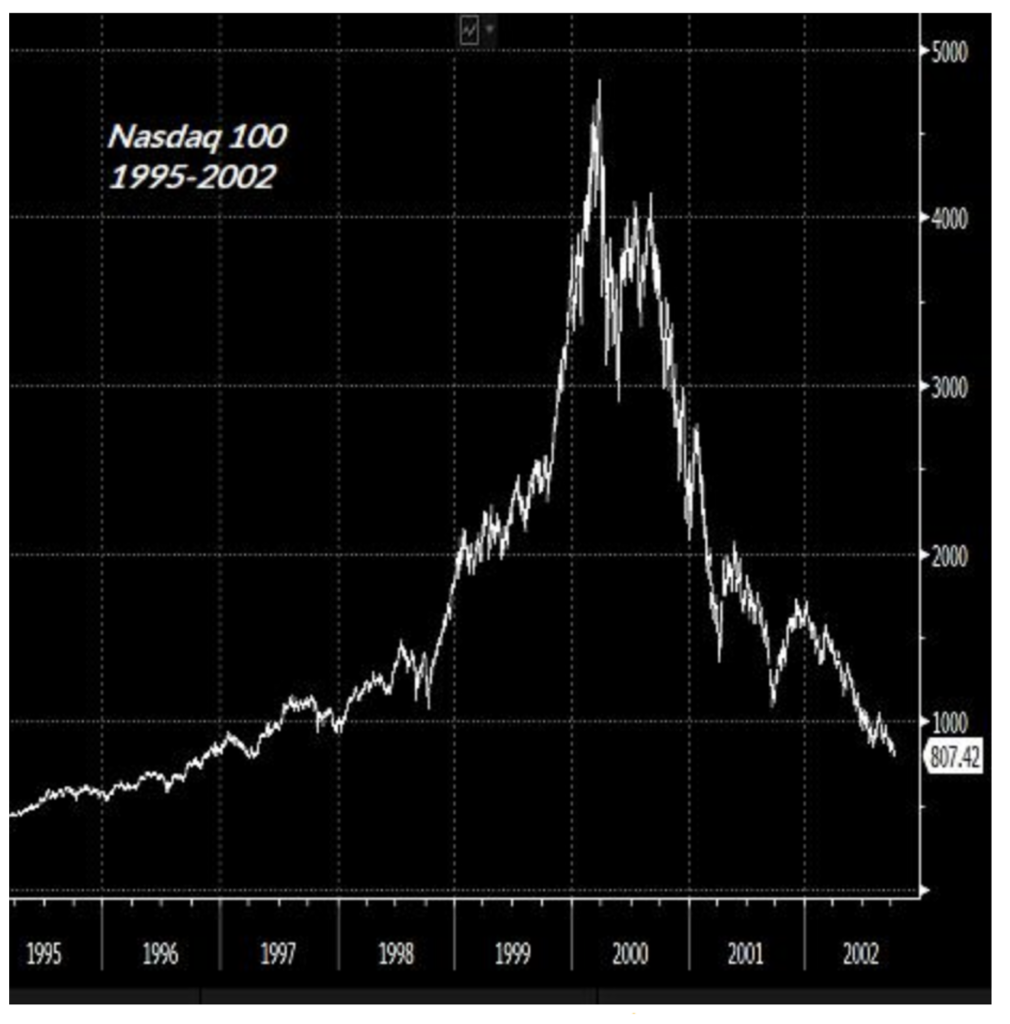

I did not see the extent of this rally coming and remain skeptical of it continuing. Indeed, despite the growing optimism of the consensus, I now see stunning similarities between today’s equity market and previous market tops. Most noticeable is the comparison to the dot-com top in 2000 (a similar period of narrowing/concentrated market leadership and the belief in technology’s new big thing (the internet) to deliver robust revenue/profit expectations (which failed to pan out)):

At times like this I am reminded that incredulity robs us of many pleasures and gives us very little in return! Or as Samuel Johnson wrote:

“To revenge reasonable incredulity by refusing evidence, is a degree of insolence with which the world is not yet acquainted; and stubborn audacity is the last refuge of guilt.”

In today’s opening missive I have several points to make:

* Though it may appear — to Samuel Johnson (in his above quote) and others — that I am in stubborn denial of the facts (and the market’s amazing advance), I feel I have many justifiable reasons to maintain our doubt and skepticism. I have discussed my reasoning and evidence in my past Diary commentaries and I will expand on those reasons again today.

* Though bullish market participants seem to disagree, it is an unusual and potentially threatening period for the global economy, our markets, our society and for innovation (in which AI is distorting stock prices and profits). I have had a lot to say about this in the past and I will continue in this missive and in the future.

* Main Street and Wall Street have diverged dramatically.

* I will further explain why — despite growing ever more bearish — I have maintained a relatively small net exposure on the short side (and have no current plans to meaningfully expand my short portfolio further).

With the fear of missing out reverberating, there is growing pressure to speculate today. Nonetheless, I will not abandon my disciplines nor forget the lessons of history.

Before expanding on our market view, I wanted to recite a relevant quote from Georg Hegel and cite two examples of differing behavior towards the end of the dot-com boom in 2000:

”What we have learned from history is that too many have not learned from history.”

Below are examples of Berkshire Hathaway’s ($BRK.A, $BRK.B) avoidance of the dot-com bust and Stanley Druckenmiller’s emotional purchase of tech stocks at the height of the dot-com boom.

1. The stock market, to paraphrase Warren Buffett, is a church with a casino attached to it. In the last several months the casino has become very active!

At the top of the dot-com bubble (and before a -81% drawdown in the Nasdaq), a Berkshire Hathaway shareholder asked Warren Buffett and Charlie Munger “to just speculate” in technology:

2. An example of the consequences of succumbing to speculation (and emotion) occurred around the same time when Stanley Druckenmiller (arguably the greatest modern-day investor) acquiesced to the markets and, within hours of the dot-com top purchased billions of dollars of technology stocks.

Here Stan recounts his investment boner in March 2000, when he purchased $6 billion in tech stocks at the peak of the dot-com bubble, which resulted in losses of about $3 billion in only six weeks:

Another Technology Victim; Top Soros Fund Manager Says He ‘Overplayed’ Hand – The New York Times

Druckenmiller on his $3B loss.

Stay tuned for Part 2…