Best Risk-Reward in Cannabis

Best long-term reward vs. risk in cannabis is $VRNO.

Position: Long VRNO (S)

Best long-term reward vs. risk in cannabis is $VRNO.

Position: Long VRNO (S)

Today I’m going to speak from the heart, and tell you that we’re ruled by f…..g imbeciles.

AI is a perfect storm of failed concepts and organizations, and the apex of the Era of the Business Idiot, an epoch where we’re ruled by people so thoroughly disconnected from the actual workforce that it was inevitable that a technology would be created specifically to grift them.

Just ask Aaron Levie, CEO of Box:

CEOs are uniquely prone to AI psychosis because they’re sufficiently distant from the last mile of work that still has to happen to generate most value with AI.

LLMs are dangerous for many, many reasons, but the under-discussed one is how well they play to a certain kind of executive imbecile. Generative AI is — to quote Mo Bitar — really good at doing an impression of work, much like most managers and c-suite executives, and even if it’s completely incapable of doing something, it’ll absolutely say it can and tell you you’re amazing for suggesting it.

And that’s why Business Idiots love it.”

– Ed Zitron

Here is more, read on:

Position: None

Thanks goodness that I heard on the noon show (Slink) that the consumer is well:

Position: None

I am adding to my cannabis exposure and buying July (monthly) $4 calls.

I like the risk/reward.

Position: Long MSOS common (L) and calls (S)

Position: None

Potential “outside day” for $MS and $GS.

Both made all-time highs and are now lower on the day.

Position: Short MS (M)

I shorted more $GRNY at $27.32.

Position: Short GRNY (M)

From Peter Boockvar:

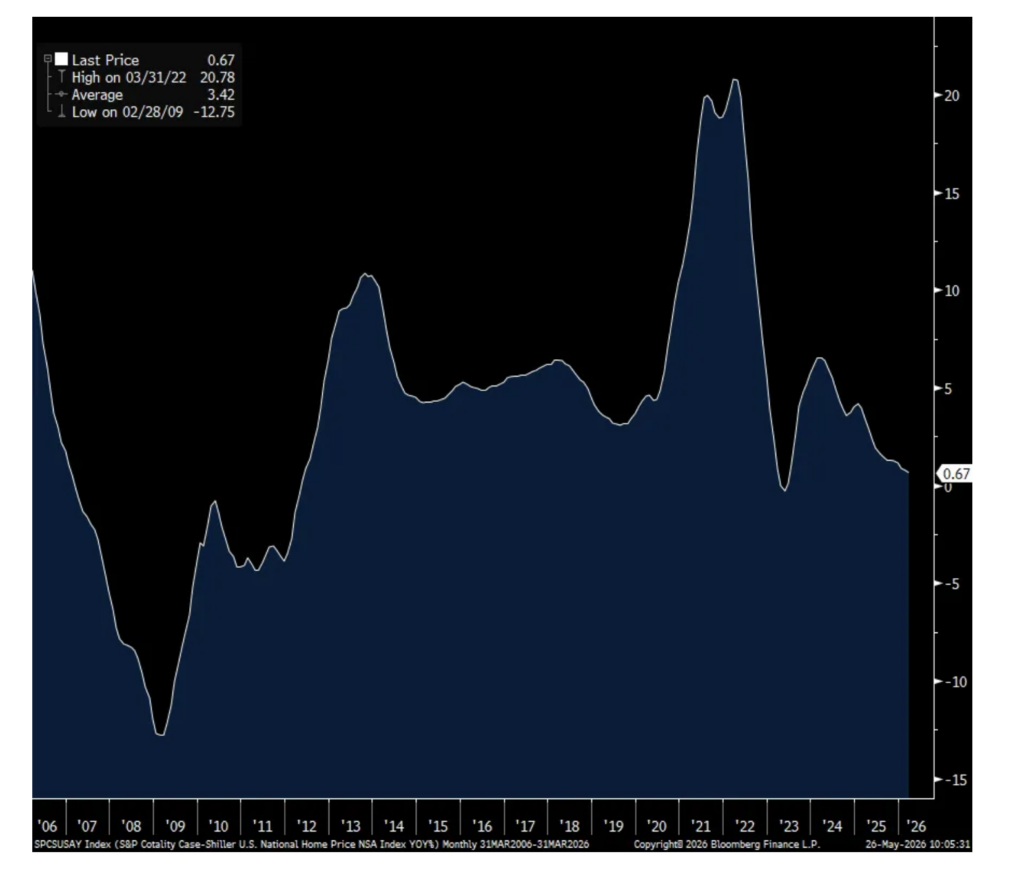

Home price growth in March (so somewhat dated and doesn’t reflect recent inflection up again in mortgage rates) rose .67% y/o/y, vs .75% in February. That’s the slowest pace since June 2023 and I think the moderation in price increases is a good thing as it allows wage growth to catch up and hopefully improve affordability and the chances of a rise in transactions that is still hovering around 30 yr lows.

The overheated and now a bit over supplied sunbelt states are seeing the biggest weakness with home price declines in Tampa, Phoenix, Las Vegas, Atlanta and Dallas. Throw in Denver also on the extra supply side. Weakness was seen too in LA and Seattle.

On the flip side, NY, Chicago, Cleveland and Boston saw the biggest price increases and that have more limited supply.

S&P Global said “More than half of the 20 major US housing markets recorded y/o/y price declines in March, reflecting a broadening and deepening housing slowdown.”

S&P Cotality Case-Shiller Home Price index y/o/y

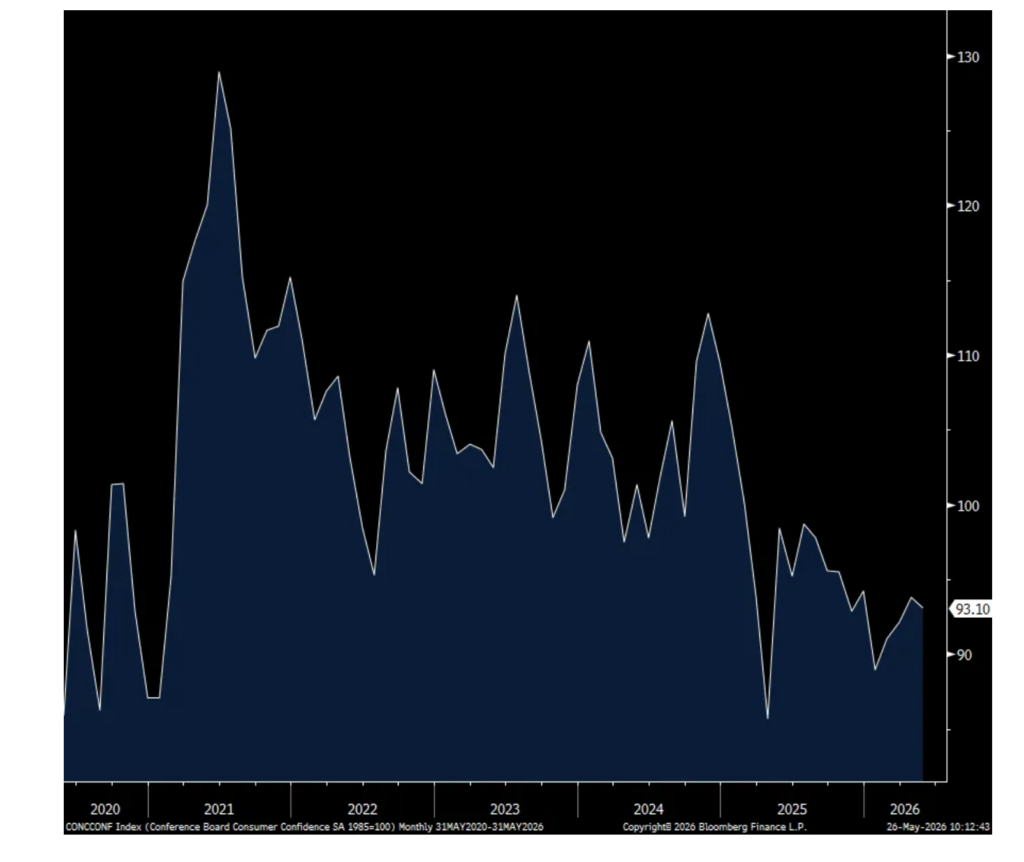

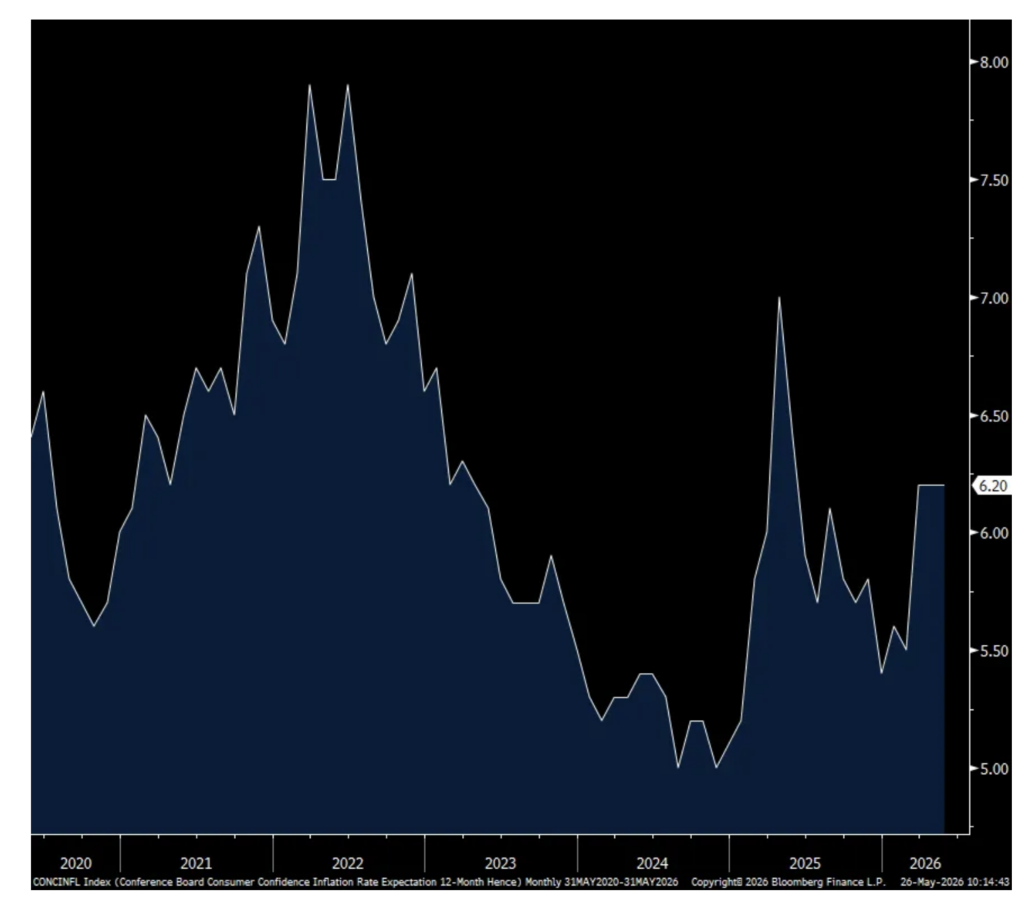

As measured by the Conference Board, their consumer confidence index in May fell slightly to 93.1 from 93.8 and vs 92.2 in March and 91 in February. The internals were mixed as the Present Situation fell to a 3 month low but the Expectations component rose 1 pt m/o/m to a 5 month high. One year inflation expectations was at 6.2% for a 3rd month and that stays at a one year high.

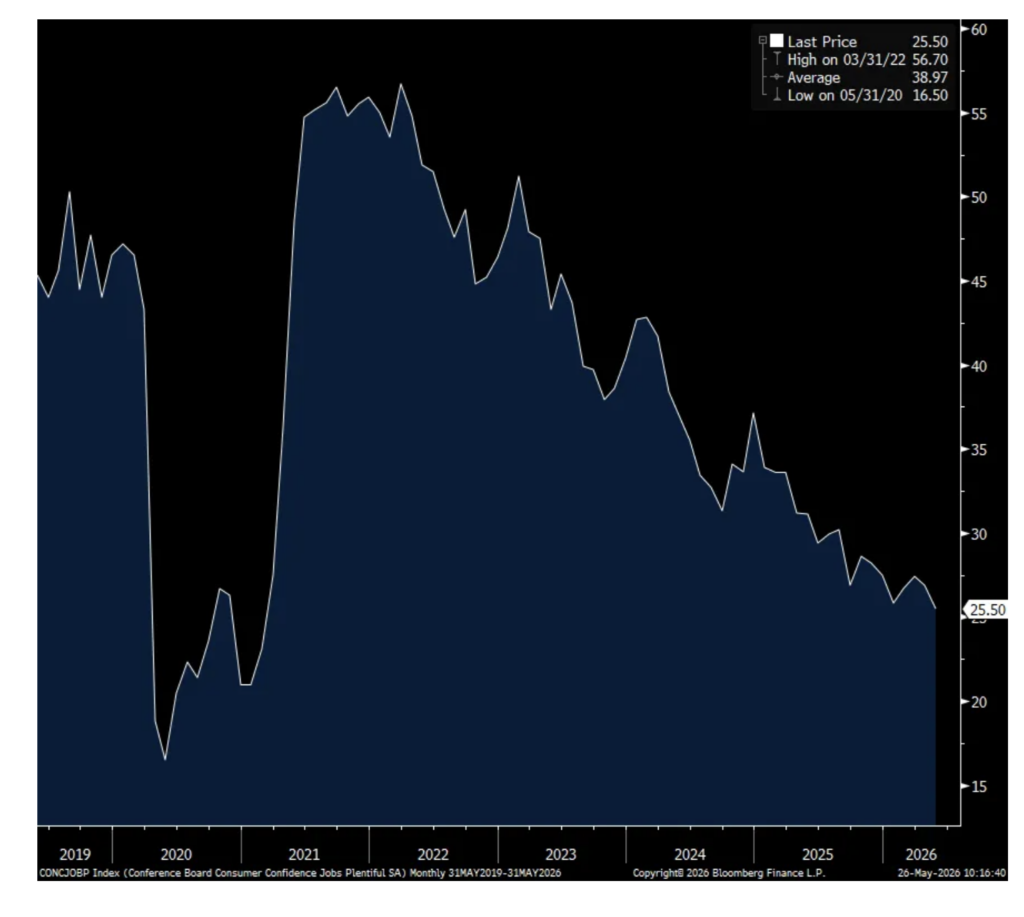

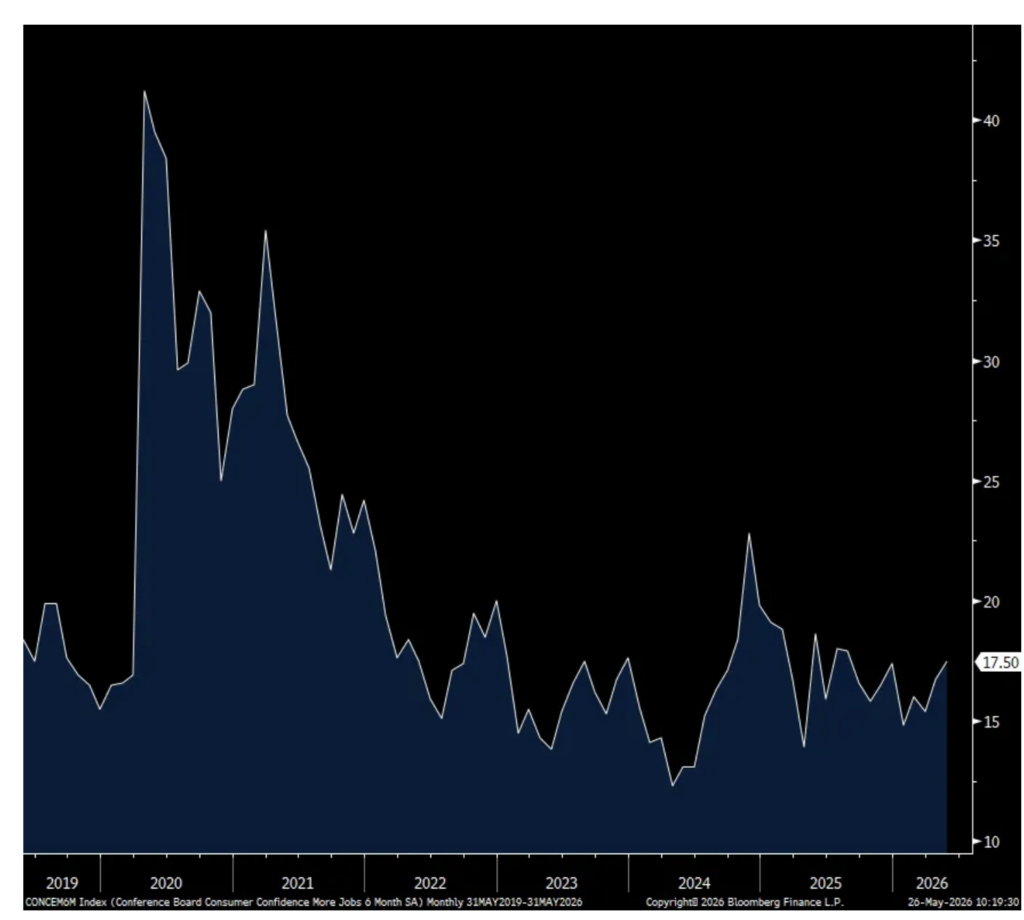

The answers to the labor market questions were mixed as those that said jobs were Plentiful fell to the lowest level since February 2021 but those that said they were Hard to Get declined to the least since last October. And helping to boost the overall Expectations question, the 6 month outlook for ‘more’ jobs rose to the highest since last August though is still bouncing along the bottom as seen below. Expectations for income growth also improved but did too for those that expect it to decline (a fall in those that expect it to stay the same).

Spending intentions pulled back after the rise in April, particularly for autos and vehicles. With respect to spending on services, the Conference Board said, “Consumers planning more spending on services over the next six months shifted from “yes” and “maybe” to “no” in May. Future spending plans on services were mixed. Consumer spending trends in 2026 remained focused on “cheap thrills” and necessary services, but there was some increase in demand for discretionary services like personal travel, fitness, amusement parks, and gambling. Among all service categories, restaurants/bars/take-out, streaming/internet/mobile services, and beauty and personal care, remained among the top three spending targets.” And, “Travel intentions for six months ahead ticked up in May, and consumers continued to favor domestic destinations over international travel.”

The Conference Board said what we’re well aware of in terms of the bottom line, “Consumer confidence edged downward in May as the inflationary impacts of the war in the Middle East intensified…Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism in May. References to prices and oil and gas increased in frequency for a second consecutive month, while mentions of war, geopolitics, and conflict remained elevated – likely signaling consumers’ underlying concerns about the inflationary impacts of the war in the Middle East on their wallets.”

Finally, the Conference Board had some special questions for the respondents in May and summarized by them with this:

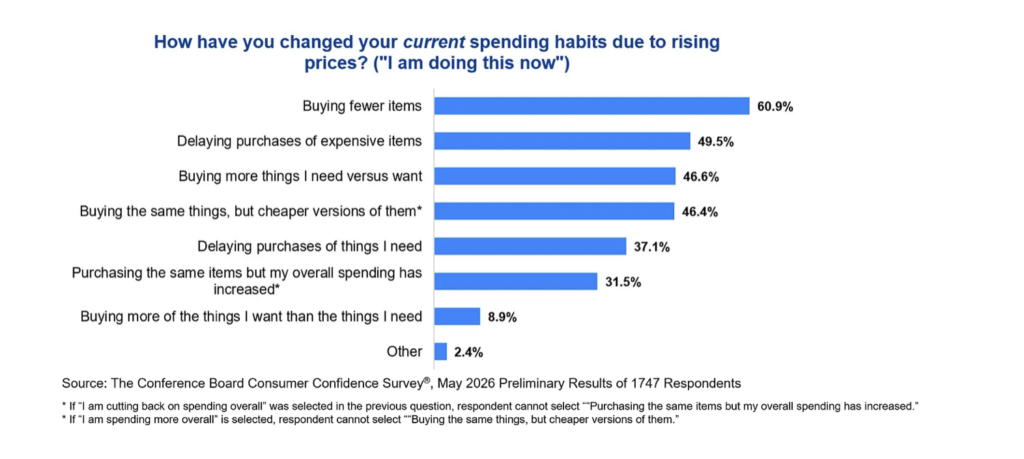

· “Two-thirds of consumers cited cutting back on spending overall due to rising prices, as of May

· Most who are cutting back bought fewer items and delayed expensive purchases

· Many who said they are delaying purchases of items they want rather than need, plan to buy them in the next six months

· Consumers planned to economize on clothing and footwear, hobby items, and games/toys”

Consumer Confidence

One yr Inflation Expectations

Jobs Plentiful

Expect ‘more’ jobs in coming 6 months

Positions: None.

Dougie Kass

Big reversal GS/MS

Dougie Kass

Aggressively shorted MS today, now medium sized.

Dougie Kass

Buying MSOS and individual weed stocks aggressively.

Dougie Kass

Position: Long CURLF (VS), VRNO (S), GTBIF (VS), MSOS (M); Short MSOS (M)