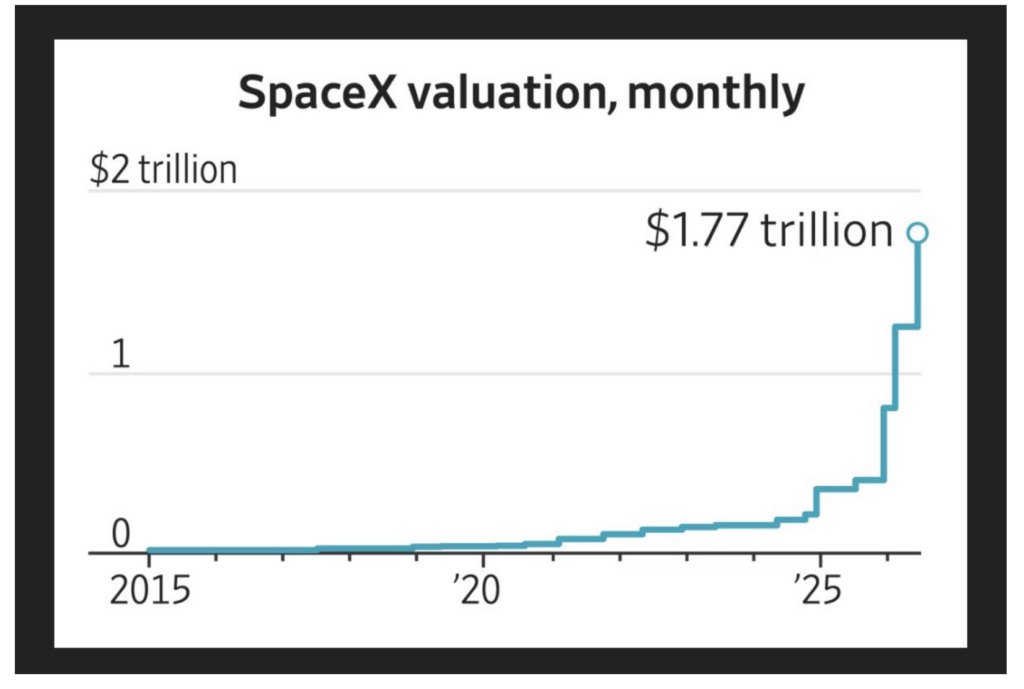

Chart of the Day from the WSJ

From the Wall Street Journal.

Positions: None.

From the Wall Street Journal.

Positions: None.

Positions: None.

My only individual equity purchase this morning was adding to MSOS ($MSOS) at $5.43.

Positions: Long MSOS VL

Anyone who has observed the market’s spectacular intraday volatility over the last four trading sessions should realize that something is amiss. The market is not behaving normally — it seems destabilized.

* Is it simply an overvalued market that is in the process of correcting?

* Is it an overvalued and concentrated market led by large-cap technology that is rotating into new leadership?

* Is it a signal that the AI revolution might face growing fundamental headwinds?

* Is the proliferation of leveraged ETFs and the growing acceptance of the market as a casino (with the ubiquitous presence of 0DTE options) undermining market stability, acting like an infant splashing around in a bathtub (violently moving from side to side)?

* Is it the consequences of the evolution of market structure (the tail wagging the dog), in which passive products and strategies dominate the investment landscape?

* Or, have the machines and algos “gone wild” (in dealing with a potential inflection point or price momentum change)?

To me, its all of the above — some of each.

We are likely entering a slippery slope — great for opportunistic traders, lousy for the buy-and-hold crowd.

Position: None

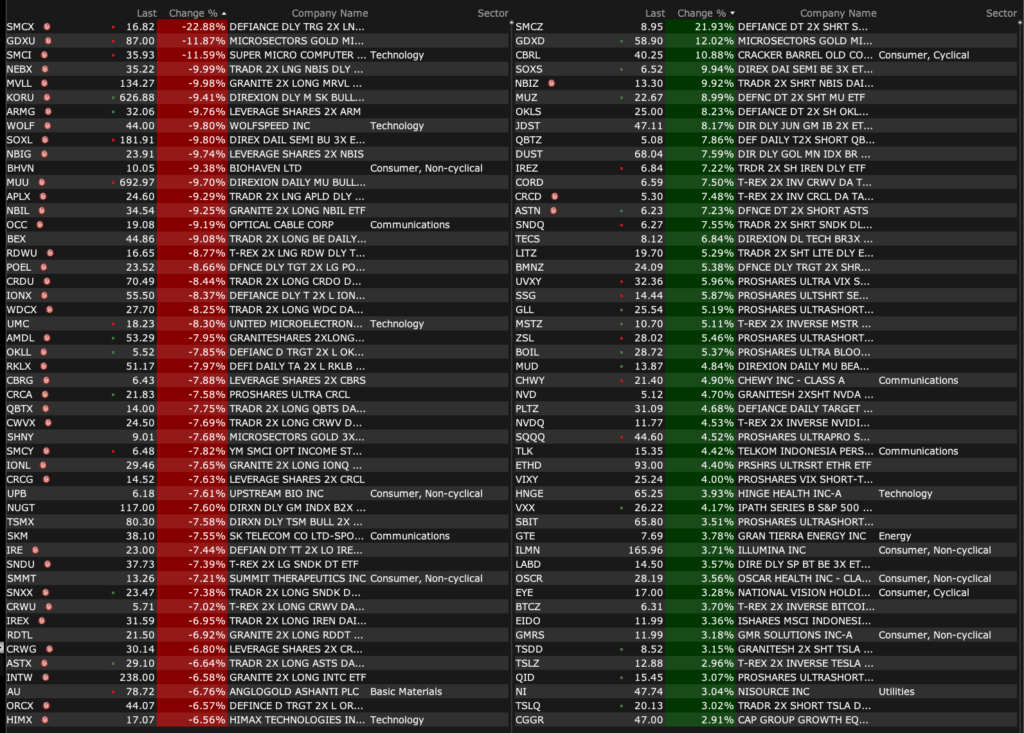

-CBRL +12% (earnings, guidance)

-LAKE +8.0% (earnings, color)

-BORR +4.2% (insider purchased ~$5M in common shares)

-OSCR +3.6% (Barclays Raised OSCR to Overweight from Equal Weight, price target: $35)

-ILMN +3.1% (JPMorgan Chase and Co Raised ILMN to Overweight from Neutral, price target: $185)

-CHWY +2.9% (earnings, guidance)

-DNTH -21% (Sanofi halts trial for peer autoimmune drug)

-SMCI -12% (announces $7B in equity and equity-linked financings)

-ARCB -8.2% (transport names lower follow Amazon launch of less-than-truckload freight offering for businesses)

-ODFL -5.6% (truckers lower lower follow Amazon launch of less-than-truckload freight offering for businesses)

-MU -4.8% (profit taking in sector)

-INTC -3.5% (sector weakness)

-BABA -2.8% (lower following report China prepping to spend ~2T yuan over 5-years building data centers to advance domestic AI industry, potentially threatening private cloud operators)

-CCL -1.7% (leisure names under pressure from geopolitical concerns)

Positions: None.

From Peter Boockvar:

While the markets mostly care about consumer price inflation, I don’t believe the inflation picture is complete by just looking at today’s CPI. Tomorrow’s PPI will be just as important with the difference being who is eating the widespread cost pressures and who is not. To print here again what the Beige Book said last week, “The ability to pass on higher costs remained mixed across sectors, particularly among consumer-facing firms.” Today’s headline CPI is expected to rise 4.2% y/o/y while PPI is expected to be up 6.4%. At the core level, consensus today is for a gain of 2.9% for CPI and by 5.4% for PPI.

China is seeing quite the spread between CPI and PPI. In May, CPI rose 1.2% y/o/y while PPI jumped by 6.3% y/o/y. Someone only looking at the former will tell me there is no inflation and then I offer the latter and say there certainly is plenty, just falling out on different parts of the economic chain in differing degrees.

On the heels of the massive equity raise done by Google and chatter about one coming from Meta, I thought the Bloomberg story today on Softbank was really interesting and maybe for the first time I can recall reflecting some questions being asked on valuations, or maybe just for Open AI. Not sure yet. The article said, “Softbank Group Corp.’s talks with potential creditors to raise at least $6 billion from a margin loan backed by its OpenAI stake have stalled, people familiar with the matter said, just weeks after the Japanese conglomerate cut its initial target from $10 billion.”

“It’s unclear why the margin loan discussions stalled. Borrowers and creditors can pause and revisit fundraising discussions for various reasons, and Softbank hasn’t elaborated on its plans, the people said.” The stock fell 8.3% overnight in Tokyo.

Casey’s General Store is one of my favorite earnings results and conference calls to go through because they touch consumers of all income levels with their convenience and gasoline station business. Over the years they have morphed from a business focused on the latter to one more on the former, and they have actually turned the company into a pizza shop in part. While a pizza fan, I have yet to try it. Let me know how it is if you have.

The earnings call is this morning and I will write about what they said tomorrow while this is from the earnings press release:

“Inside same store sales were up 5.5%, or 7.4% on a two year stack basis, driven by strong performance in whole pizzas as well as appetizers and sides in the prepared food and dispensed beverage category in addition to non-alcoholic beverages in the grocery and general merchandise category.

I’ve expressed my bullish stance on the stocks of some consumer staples names, particularly in food and was encouraged to see the Hormel earnings report a few weeks ago, Campbell’s the other day which was about as expected and now followed by JM Smucker yesterday and whose stock jumped by 10.4%.

Understand that a bombed out stock/sector can do better by having its fundamental picture be less bad. And when valuations are cheap, dividends, that are sustainable, are high, sentiment is awful, and the stock charts look ugly, it becomes I believe a fertile ground for opportunity.

They said of note:

“Total company net sales increased 6%, driven by growth in the Coffee, Away From Home, Pet Foods, and Frozen Handheld and Spreads segments.”

In their Coffee business, “We have demonstrated our ability to recover increased commodity costs through responsible pricing. Due to higher costs and the pass-through nature of the coffee category, we implemented price increases in May and August of calendar year 2025. Since then, price elasticity trends have been favorable relative to our initial expectations.” They are now seeing some pullback in green coffee commodity prices and they could reverse some of the price increases if sustained.

Uncrustables continues to do very well for them, with sales up 8% in the quarter and it is now a $1 billion brand.

In Pet Foods, I’m hearing again (from Petco, Colgate, and Chewy) how the cat business is doing better than dog, “net sales increased 2%, driven by continued momentum in cat food, partially offset by a decline in dog snacks.”

With respect to overall inflation, ex green coffee deflation and tariffs, “we do anticipate cost inflation of low single digits across the balance of our portfolio, and that’s largely coming through packaging, ingredients and transportation.”

Also yesterday were a few conferences where companies I follow spoke at. I’ve been highlighting here for months the ever rising cost of truck transportation and both JB Hunt and Schneider National talked about it yesterday.

From JB Hunt:

“Since 2022, we’ve been in an oversupplied overcapacity what would be called a freight recession.” That is so yesterday though with some pricing at “all time highs as indicators of capacity challenges as well as overall potential demand.” They see “industrial demand is solid. Customers are resilient.” I still think some of the demand strength is the pull forward of ordering and we’ll see at some point the extent.

“this industry is behind. It’s been four years in a cost inflationary environment and a rate deflationary environment. The industry is not healthy. It hasn’t generated the returns it’s needed to reinvest, and that has a catch-up aspect that’s going on right now. So the magnitude of what could happen from a catch-up perspective, but also going forward on what we need to execute is still in flight and in motion. So it could be significant as we said.”

From Schneider National:

“Well, I’d say demand, while there’s some pockets of strength, certainly, especially in what we’re seeing with production picking up a little bit, generally, it’s been stable is the way I would characterize it.” On some weakness, “home building, everything that goes into a home being created as well as automotive, perhaps not as strong as what it could be had we seen an interest rate decrease.”

“But, what we’ve seen the most activity is capacity exiting the market.”

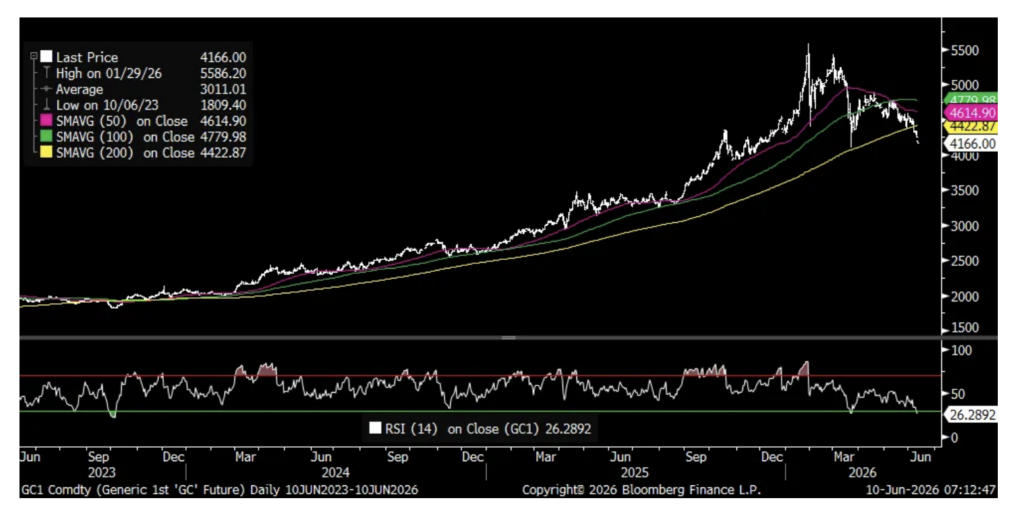

I’ve mentioned my belief that US Treasuries and sovereign bond markets in Europe too that are heavily foreign owned have been a source of funds for those countries seeing ever rising spending needs to cushion the blow of higher energy prices. I think gold has been a source of funds too and the pullback off the early year high continues. But, we’re now stretching it on a technical perspective.

If not aware, there is a technical gauge called the Gold Miners Bullish Percent Index which is a breadth indicator that vacillates between 0 and 100 with 30-70 being a normal range. Yesterday it closed at zero, and thus cannot get any worse. Also, the 14 day Relative Strength Index is down to 26, the lowest since October 2023.

Gold (generic contract)

Not with help from lower mortgage rates as they were little changed from last week at 6.60%, purchase applications rebounded by 7.3% w/o/w after three weeks of declines. Refi’s rose 15.3% w/o/w after six weeks of declines

Positions: None.

Positions: None.

With S&P futures rallying to -56 handles I have sold my Index trading long rentals ahead of the inflation data for a very small profit:

* SPY ($SPY) $731.68

* QQQ ($QQQ) $699.18

Positions: none.

Positions: None.