Boockvar on Oil, Commodity Stockpiling, Sushi

From Peter Boockvar:

What now?/Commodity stockpiling/The sushi biz/RBNZ hikes

Oil prices are doing what’s expected in response to the news while global bond yields continue higher even with oil prices well off their war highs and a price I mentioned Monday I found most interesting. The US 10 yr yield is now just 10 bps from the May high while the price of oil is still down about 25% from its close high (intraday was about $120).

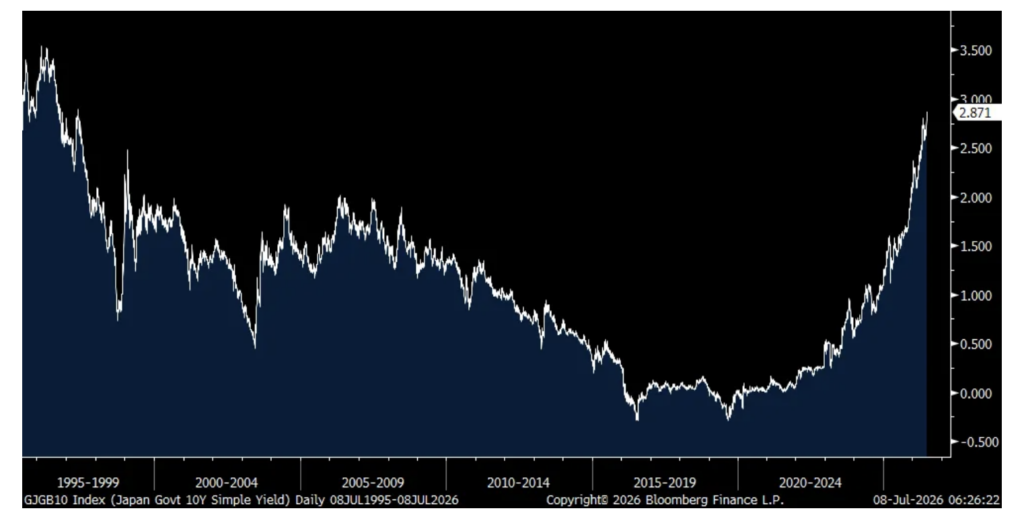

I’ll emphasize again that the move up in developed market bond yields continues to be global as debts and deficits now matter. The bond bear market continues on. The 10 yr JGB yield closed at a fresh 29 year high at 2.87%. The 10 yr French oat yield has broken out to a 17 yr high at 3.90% up 11 bps today. The 10 yr UK gilt yield is up 10 bps to 4.95% but below its May peak of 5.17%. The German 10 yr yield is up 8 bps to 3.07% though about 12 bps from a 15 yr high.

Oil in orange, US 10 yr yield in white

JGB 10 yr yield

French 10 yr yield

One of my bull cases for commodities has been the expected stock piling I expect to see of a variety of things. A story I read on Bloomberg this morning, “The US Department of Defense is buying lithium for its strategic stockpiles as the nation ramps up efforts to reduce supply risks for critical minerals. The Defense Logistics Agency is seeking offers for almost 36 million pounds, about 16,000 tons, of battery grade lithium carbonate over the next five years in a contract worth as much as $300 million, according to a tender document published on a US government website dated July 2.”

Yesterday, I read this on Reuters, “Germany’s Economy Ministry is drawing up plans for a state-owned strategic gas reserve to be used in emergencies…The reserve would hold around 24 terawatt-hours (TWh) of gas, equivalent to just under 10% of Germany’s total gas storage capacity, and would be financed through a levy on gas consumers, the ministry said. The reserve is intended to protect against extreme situation, such as sabotage of critical energy infrastructure or a severe global gas storage.”

I expect to hear a lot more of these type stories in the months to come.

In the June NY Fed Consumer Expectations Survey seen yesterday, one yr inflation expectations rose to 3.7% from 3.5% even as expectations for gasoline prices fell to the lowest since 2022. Higher expectations for health care costs and rents offset the gas decline, along with a lower outlook for food and college tuition costs.

Otherwise from the NY Fed, “Labor market expectations improved, with job-finding expectations increasing and job-loss expectations and expectations about the unemployment rate declining. Spending growth expectations were unchanged. Respondents were more optimistic about their future household financial situations, while expectations about future credit availability deteriorated slightly.”

Of note, and another example of how stock market sentiment follows price, “The mean perceived probability that U.S. stock prices will be higher 12 months from now increased by 2.9 percentage points to 40.9%, the highest level of the series since April 2021.”

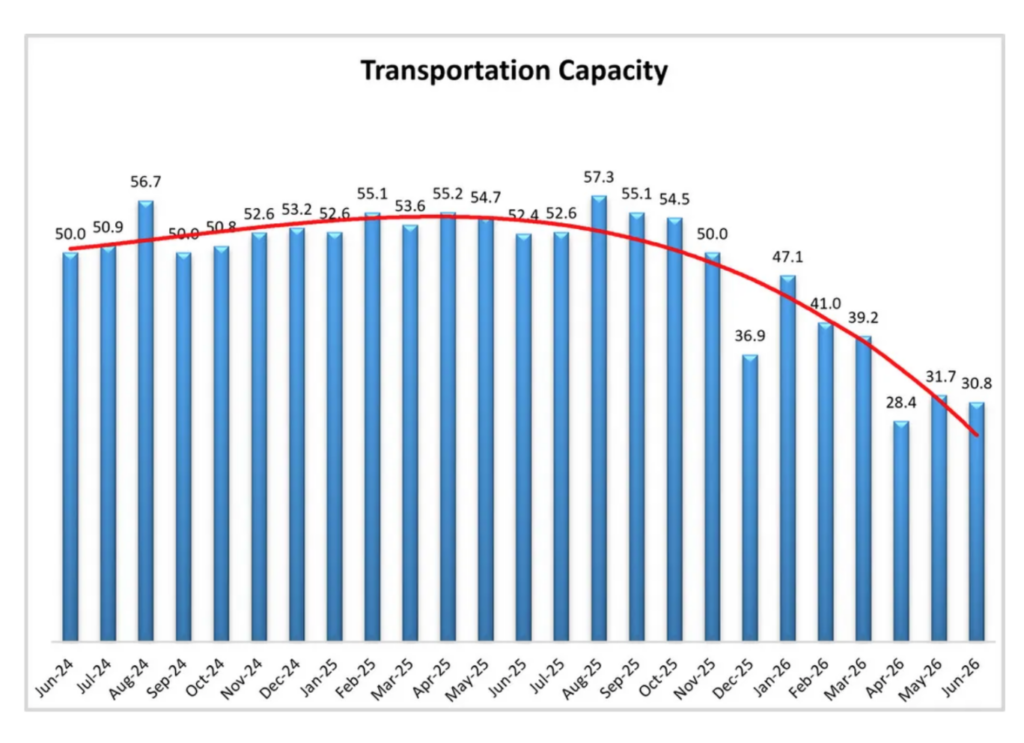

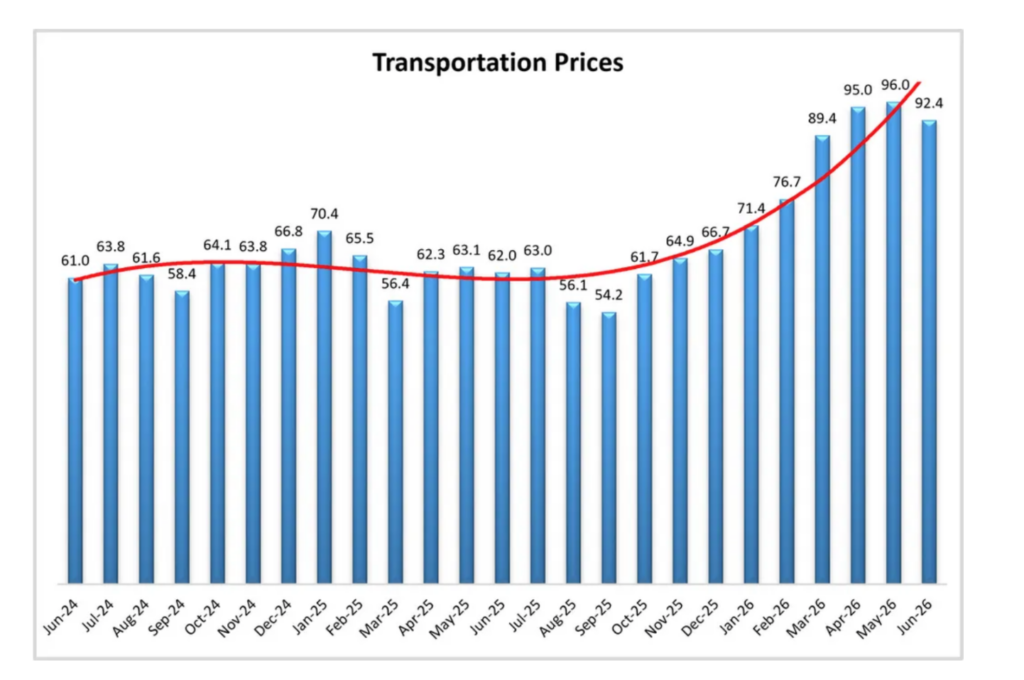

The June Logistics Managers’ Index came out yesterday and rose m/o/m driven by its inventory component. They said “This level of inventory expansion is a flip from what we have seen for most of 2026. The push from retailers is likely representative of two factors: 1)In spite of inflation, consumer spending has held through the first half of the year, giving retailers confidence in bringing forward goods for the second half of the year; 2)tariffs may increase in later July, so some of what we’re seeing is a pull-forward ahead of peak season.”

I think some of the pull forward is also due to companies that want to get ahead of any supply issues and/or other price increases.

Transportation prices did slip a touch after the May read, which was a record in this index as capacity continues to come out of the market.

Kura Sushi is trading lower pre market after they missed estimates, both top and bottom line, and slightly lowered their full year guidance. They said this of note;

Comps fell .4% y/o/y “with negative 5.1% of traffic, offset by positive 4.7% in price and mix. Effective pricing for the quarter was 4.5%.”

“We were certainly disappointed that traffic came in negatively…but we believe that this is largely due to elevated gas prices…As the gas prices have eased, we’re beginning to see a little bit of benefit as we’ve entered Q4, but those benefits are partially offset by how popular the World Cup is, and so the guidance that we’re providing for the revenue contemplates the Q3 and Q4 macro background as well as the construction delays” of new restaurants.

Influenced by the holiday, purchase applications fell .6% w/o/w and little changed over the past 3 weeks, ahead of what will be another rise in mortgage rates if the move in the US 10 yr yield holds. Refi’s were down by 4.1% w/o/w.

The Reserve Bank of New Zealand raised its cash rate to 2.50% as expected. New Zealand is a small country as we know with a modestly sized economy but it is fully developed and why I pay attention to what their central bank does. And, they hinted at further increases, “With inflation still above target and economic activity expected to strengthen, some further reduction in monetary stimulus is likely to be required.”

For perspective, before they started hiking in 2021, their cash rate was .25%. It went as high as 5.5% in 2023 and down to 2.25% early this year.

Positions: None.