Boockvar on Service Sector’s Heavy Lifting

From Peter Boockvar:

US service sector continues to carry most of the load, as it usually does

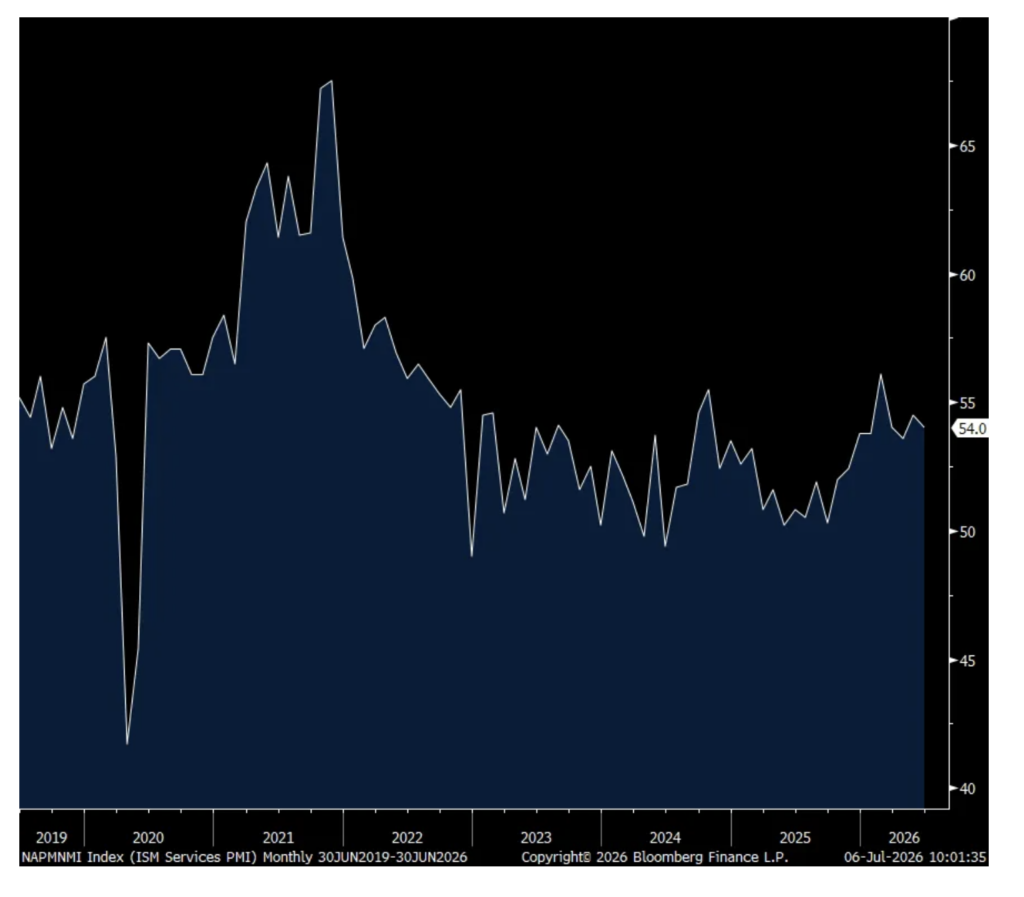

The June ISM services index at 54 was spot on with expectations but down slightly from the 54.5 print seen in May and around the half yr average of 54.3. The Business Activity component fell 2.3 pts m/o/m to 55.4 and below the 6 month average of 56.7.

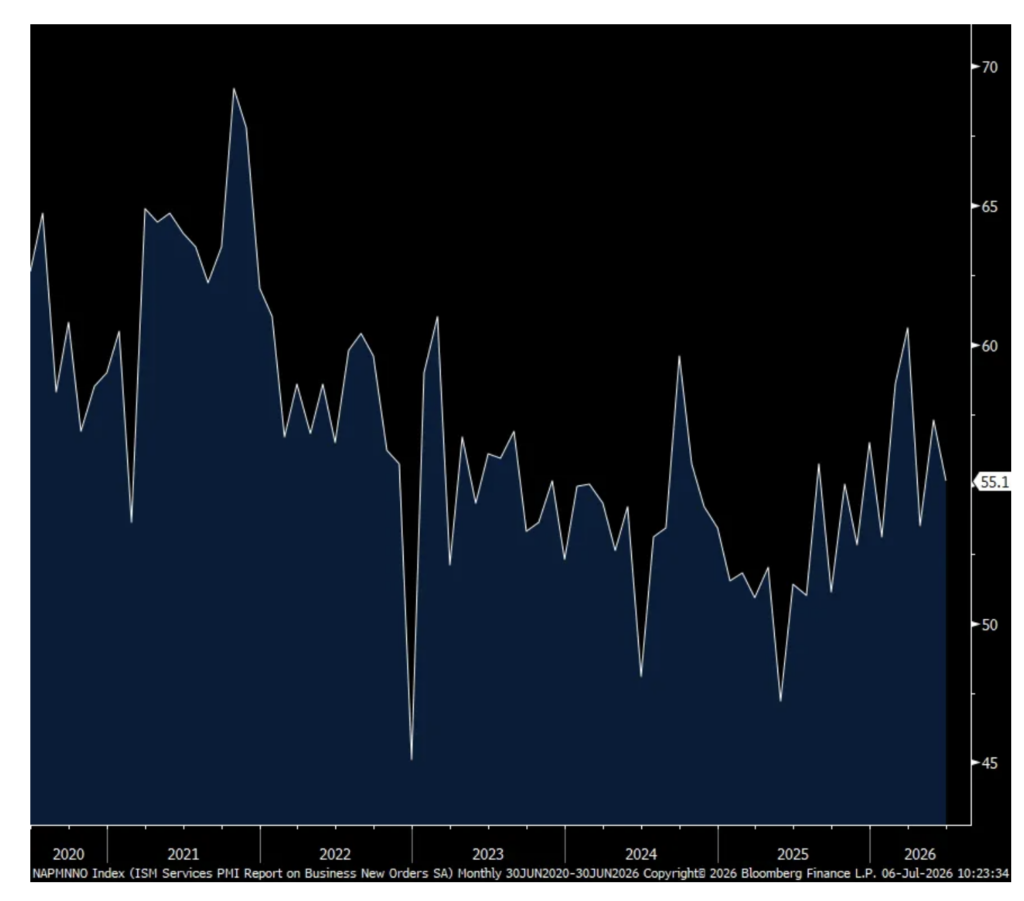

New orders jumped to 60.6 in March right after the war started and in June was 55.1 which compares with the 6 month average of 56.4. Backlogs stayed above 50 for the 5th straight month at 54.9 vs 51.3 in May. Inventories jumped in May to 62.5 as I believe we saw a lot of order pull forwards and it dropped back down by 11.3 pts in June to 51.2. To this, the ISM said “The Inventories Index dropped to its second-lowest level since October 2025, indicating that the buy-ahead phenomenon from earlier in the year may be over.”

Supply chain lead times (Supplier Deliveries) fell .8 pts m/o/m to 54.4 and just below the half yr average of 55.1. The ISM said, “Despite easing of the Supplier Deliveries Index, there was an increase in commodities listed as ‘in Short Supply,’ increasing from five in May to nine in June. All commodities in short supply in June are commodities necessary for data center construction.”

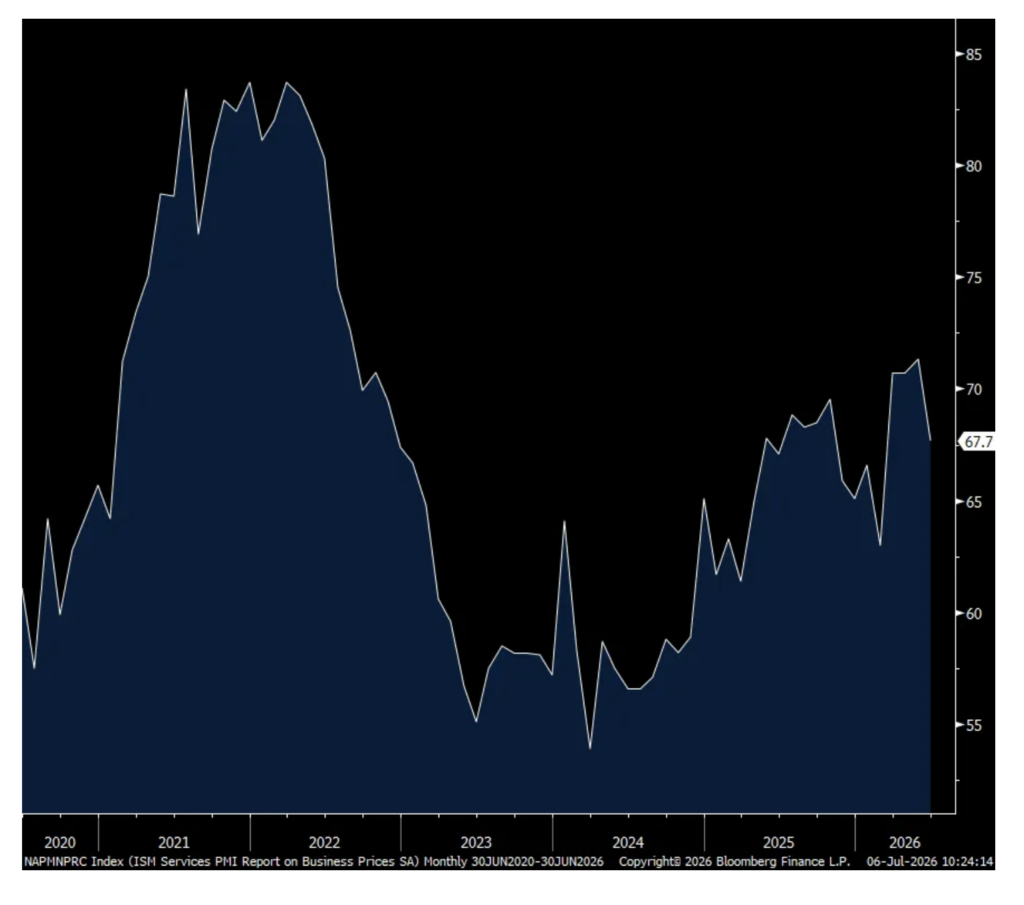

Prices paid was down 3.6 pts m/o/m to 67.7 but still holding well above 50. The ISM said “Respondents in June commented less frequently about pricing impacts on petroleum products, while tariff impacts continued to be a theme for increased pricing pressure…Memory components, copper, aluminum, and heating, ventilation and air conditioning (HVAC) equipment continued multimonth runs of being listed as up in price.” Only from the point of view of an economist is a tariff a one time impact by the way. I’ll give a quick example. A vendor that sources product overseas to sell to Walmart that just absorbed a tariff induced cost increase (assuming not subject to IEEPA refund) can’t just recapture all of it immediately, whether thru productivity gains and/or price increases. The former could take some time and with the latter, Walmart just won’t accept it all at once and why the vendor will space out price increases over a few years.

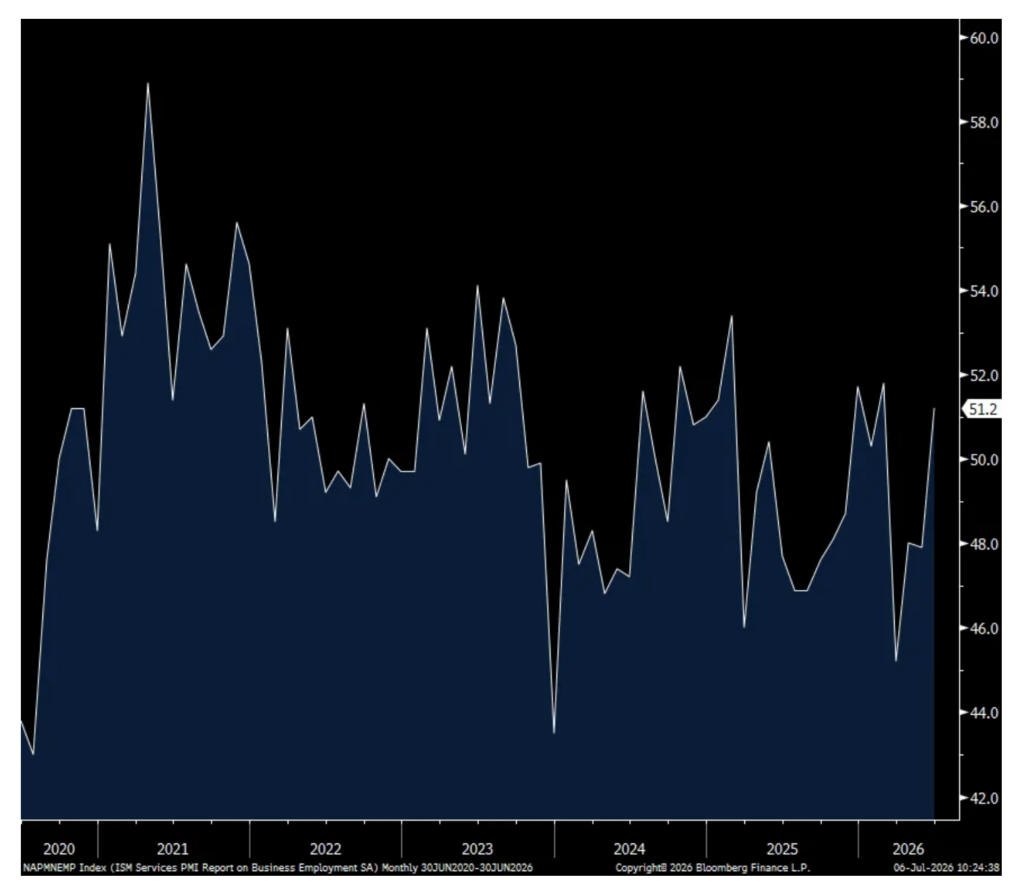

Positively, the employment component rebounded back above 50 at 51.2 after three months below, up 3.3 pts m/o/m. The ISM speculated that “World Cup related hiring in the US likely contributed to the increase to the Employment Index.” Of course in last week’s BLS payroll report, the May jump in leisure/hospitality job growth was more than reversed in June. I’m sure seasonal adjustments also around the end of the school year had an impact too in the BLS survey.

Industry breadth softened in the month with 14 sectors seeing growth vs 17 in May. Four industries saw a contraction in their business vs one in May.

Bottom line, the service sector continues to carry most of the economic weight, as it typically does, with particular strength, as we know, in data center construction (included here as opposed to in manufacturing which captures the things that go into the data center) and upper income spending. The rest of the economic story remains much more uneven.

ISM Services

New Orders

Prices Paid

Employment