Boockvar on China Competition, DXY and More

From Peter Boockvar:

The growing competition with China/DXY/Earnings calls/Overseas

I wrote this in September 2025, “I will continue to highlight the growing commercial competition between the US and China and that US technology companies have a rival the likes they are not used to seeing.” I repeat this in light of the growing reality that US GenAI models now have to compete with its Chinese rivals but also ahead of Micron’s earnings tonight. If it’s a stock you own and/or follow, make sure to familiarize yourself with ChangXin Memory Technologies or CXMT who is going public possibly in July in Hong Kong. They are China’s top DRAM manufacturer. SemiAnalysis, the well know semi research firm, wrote yesterday “China’s CXMT is Set to Challenge DRAM Incumbents…The company is likely to become the largest semiconductor IPO in China and mark a major milestone for the country’s leading memory manufacturer, which is also destined to compete only more fiercely with the leading memory suppliers of Samsung, SK Hynix, and Micron from here.”

On the NAND side, competing against Sandisk and Western Digital is Yangtze Memory Technologies. I bring this up again to just to highlight that US tech investors need to keep a very close eye on the growing competition from China tech because as we’ve seen, many Chinese companies first prioritize market share over profit margins.

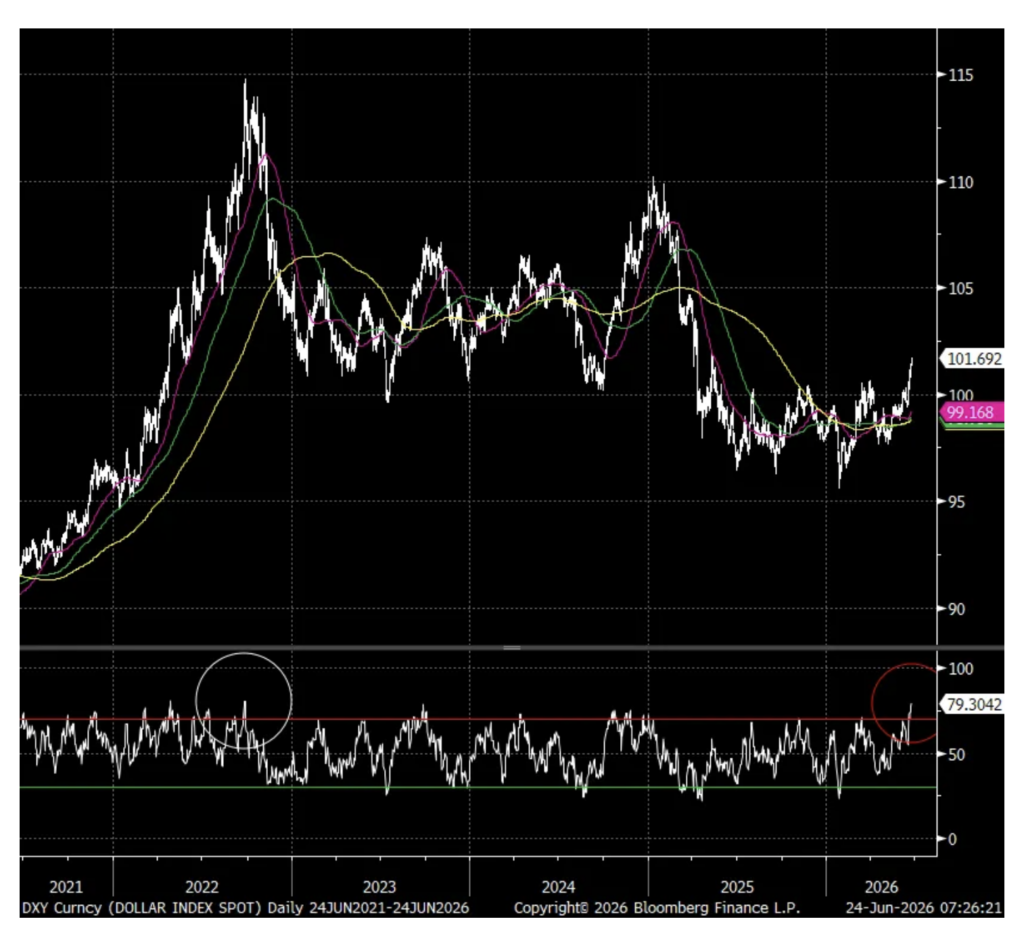

The US dollar rally has been impressive with the euro/yen heavy DXY now at the highest level since May 2025 but it is now the most overbought, according to its 14 day Relative Strength Index, since September 2022. As I continue to believe that we’re in a new world of more diversified global trade and capital flows, I’m not a believer in the sustainability of the rally. The corollary with the dollar strength is continued gold weakness, though I remain positive and long with the continued theme of central bank buying that I believe will persist.

DXY

I’ll next jump to some earnings calls of note.

From FedEx, down pre market:

“We have continued to help our customers navigate a very dynamic and complex environment, the implementation of global trade policy changes, geopolitical unrest in the Middle East, and the IEEPA refund process. In April, we began to file claims with CBP on behalf of our customers, and beginning in August, we will be passing these refunds through to our customers.”

They saw 14% revenue growth, “supported by yield strength across all services, and volume growth aligned with our commercial strategy. This growth includes a 5 percentage point benefit from fuel price driven surcharge revenue.”

To what I keep hearing about order pull forwards and have been highlighting here, “I do think that there’s a little bit of inventory buildup and restocking going on, but phenomenal, successful quarter.”

They are also benefiting from the data center buildout. “The AI and data center space is an emerging and rapidly scaling growth engine for us, delivering double digit revenue growth. Rather than a narrow vertical, this space represents a horizontal ecosystem. We are capturing demand across the entire value chain, from traditional hyperscalers to the industrial and power infrastructures that support these massive build outs.”

Oil prices, particularly diesel, has of course fallen back down again but they said “I was concerned a quarter ago that we maybe would see some demand destruction. That has not at all been the case. We’re growing around the world and we have seen no impact to demand because of the elevated fuel prices.”

From KB Homes that is trading up pre market:

“Although buyers continue to demonstrate the desire for homeownership and the ability to qualify, consumer confidence remains low, driven by a variety of factors, from elevated mortgage interest rates and affordability pressures to rising inflation and geopolitical uncertainties. We continue to attract a healthy level of traffic to our communities, signaling both consumers’ interest in purchasing a home and the appeal of our locations and products, and our cancellation rate was stable, reflecting high quality, committed buyers who can close. However, market conditions precipitated a less than optimal conversion of traffic to sales as many consumers lacked the confidence to purchase, resulting in a community absorption rate of four net orders per month.”

“To wrap up, while the spring selling season was softer than expected given consumer affordability challenges and uptick in mortgage interest rates and broader macroeconomic and geopolitical uncertainty, we made meaningful progress in returning to a predominantly build-to-order business and positioning our operations for future profitable growth.”

From Carnival and whose stock fell 5% yesterday because of a revenue miss:

“Yields exceeded expectations on resilient close-in demand and robust onboard spending.”

“while we are incredibly resilient to major external shocks, we are not immune, and near term disruption can affect the timing of results, especially when it persists for an extended period of time. Accordingly, our second quarter operational outperformance and accelerated cost efforts are offsetting the moderation we’ve incorporated into our back half outlook given the impact of the prolonged conflict. Specifically, this moderation was concentrated on our European deployments, particularly in the Med region, which were closest to the conflict. And it was further exacerbated by elevated airfares and reduced international flight capacity for North American guests. So yes, this did put a bit of a dent in our trajectory.”

With little change in the average 30 yr mortgage rate at 6.59%, purchase applications fell .6% w/o/w but up 2.8% y/o/y. Refi’s rose 3% w/o/w after a 4.5% drop in the week before and higher by 17% y/o/y.