Boockvar on Loan Delinquencies, Rig Count, Inventories

From Peter Boockvar:

Perspective/Delinquencies/Rig count & inventories/Transportation costs/PMIs

Some perspective from Michael Burry on X posted last week, that I first saw over the weekend, on the size of the upcoming major IPOs relative to the size and pace we saw in the late 1990’s.

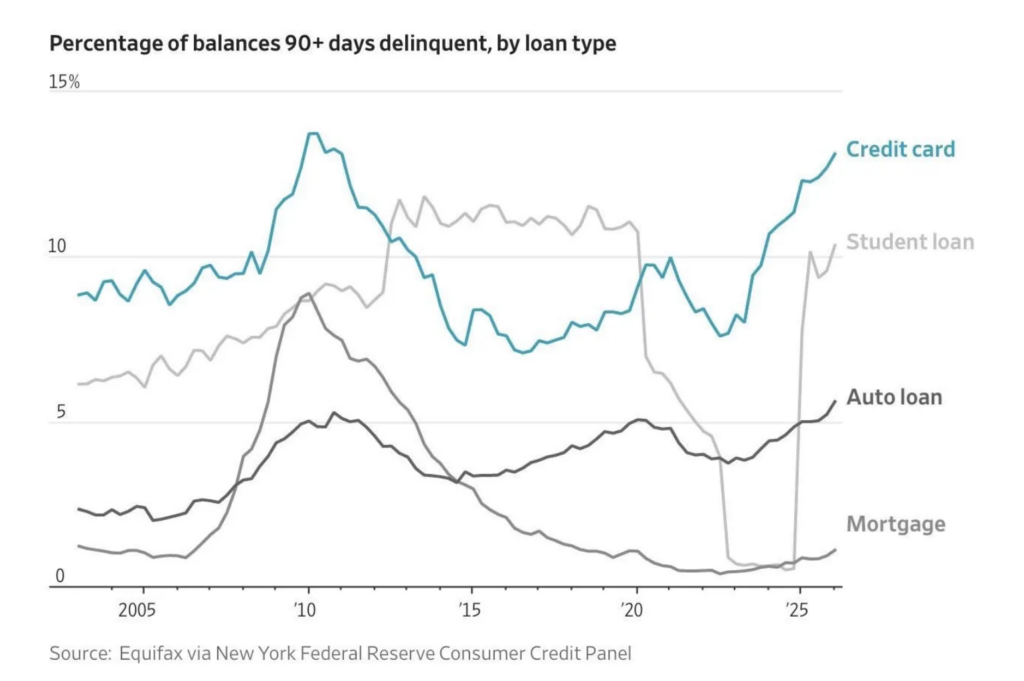

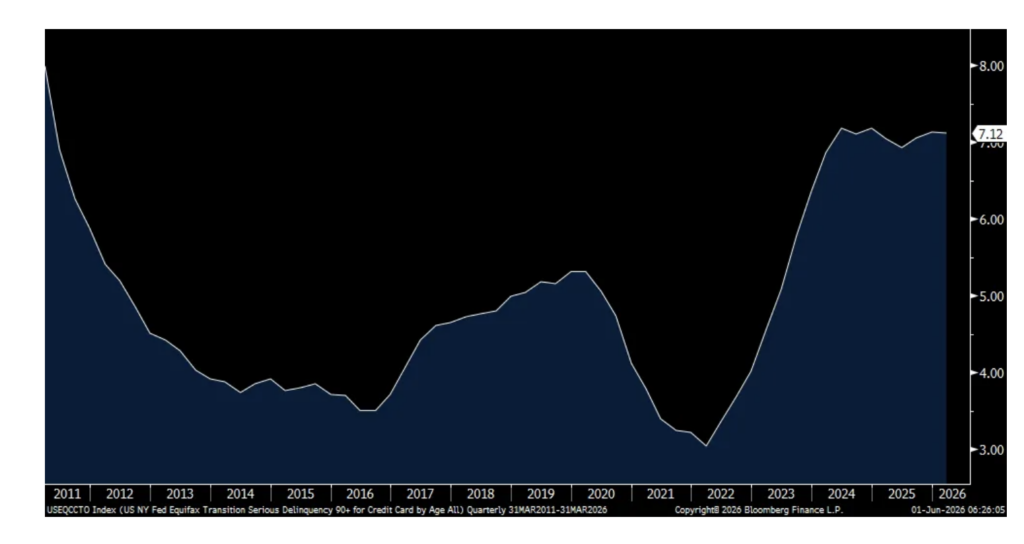

This is an updated chart from the WSJ a few days ago on the % of delinquencies that are 90+ days. What is considered delinquent is a bill that hasn’t been made in 30 days, so, the 13% is not an absolute delinquency figure but of those considered ‘delinquent’, the extent at which it’s 90 days or more. The actual 90 day delinquency rate according to the NY Fed for Q1 was 7.1%, steady over the past 2 years, though around the highest in 15 years. The 90+ day delinquency rate for autos is at 2.97%, just below a 15 yr high.

https://www.wsj.com/personal-finance/credit/us-credit-card-debt-af5c7c77

90 day+ Delinquency Rate for credit cards

90 day+ Delinquency Rate for auto loans

US oil drillers continue to respond to higher oil prices by putting more rigs to work. The Baker Hughes crude oil rig count rose by another 4 as of Friday. That’s the 5th week higher and by 22 over this time frame. We need it as we heard this warning last Thursday from Neil Chapman, a senior VP at Exxon last week speaking at the Bernstein conference.

“Commercial inventories of crude oil, of liquids, think petroleum, gasoline, diesel, jet fuel, they’ve all run down. And running down those inventories has mitigated or offset, supplemented by the release of strategic petroleum reserves, which most of the Western countries have done. All of that has mitigated the impact. You can model this. We’ve modeled it. I think a lot of people in the industry have modeled it. We’re approaching unheard of inventory levels. I mean, really, really low levels. You can debate whether that’s going to hit those really low levels in two weeks or three weeks. Once you get to that point, then you’ll see price shoot up. I mean, I think dated Brent, most people, well, a model would say dated Brent will shoot up. Once you get to that really low inventory level, up to $150, $160, the models would tell you that. And then what happens is when the price gets to a certain level, demand destruction brings it back into balance. Prices go so high, it becomes unaffordable and that’s what happens. And so we’re at that level right now.” I bolded to emphasize.

“And I think crude being in this sort of $90 to $110 for the last whatever it is, six weeks, has really been mitigated by running down inventories. It can’t last forever. So we’ll see what happens. Predicting this and the exact timing, it’s always a challenge. But that’s the way we see the picture.”

Crude Oil Rig Count

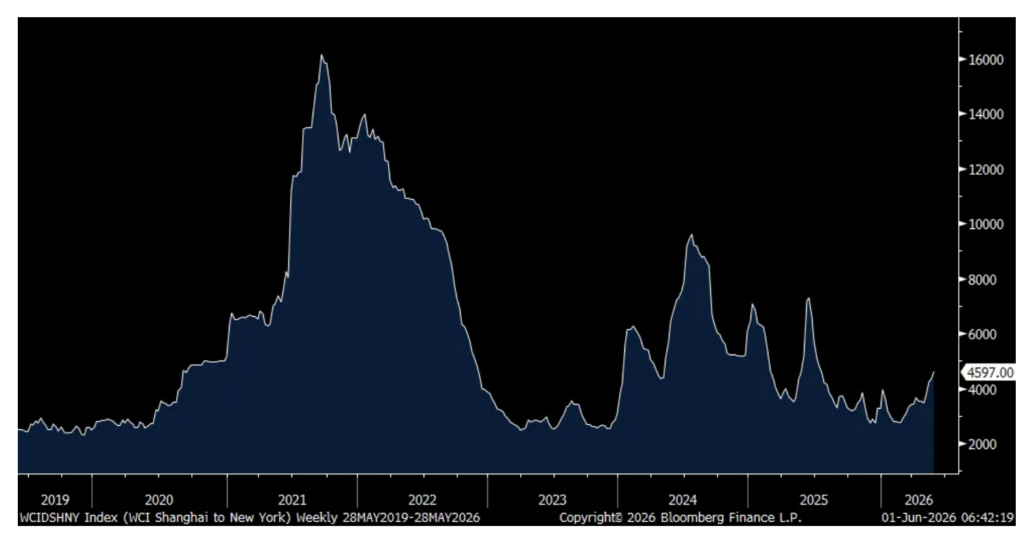

Seen last Thursday, container shipping prices continue to rise. The Shanghai to NY price rose another 6.5% w/o/w, up for the 11th week in the past 13 since the conflict started. Relative to the Covid spikes, we remain well below though. The Shanghai to LA chart looks similar and prices rose 2.6% w/o/w.

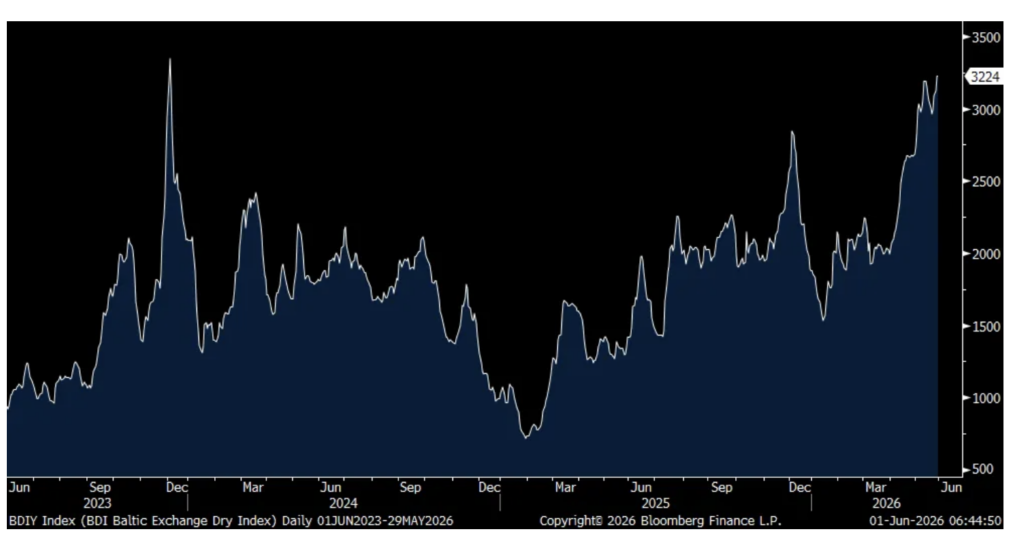

The Baltic Dry Index was flat on Friday but at the highest since late 2023. We know too that spot trucking prices have been rising to record highs. I highlight these transportation costs because we know these price changes flow through to the rest of us.

Shanghai to NY

Baltic Dry Index

Ahead of the US ISM report at 10am est, here were the May PMI’s seen overseas and they mostly improved again, helped by tech and order pull forwards but with rising cost pressures:

South Korea 54.8 vs 53.6 (certainly helped by Samsung and SK Hynix)

Taiwan 56.1 vs 55.3 (certainly helped by TSMC)

Vietnam 52.8 vs 50.5

Japan 54.5 vs 55.1

Australia 50.7 vs 51.3

India 55 vs 54.7

Philippines 50.8 vs 48.3

The China state focused manufacturing was 50 vs 50.3 in April. The non-manufacturing PMI (including construction) was 50.1 vs 49.4.

Germany 50.1 vs 51.4 (and 52.2 in March)

France 49.7 vs 52.8 (and 50 in March)

Italy 52.9 vs 52.1 (and 51.3 in March)

Spain 51.2 vs 51.7 (and 48.7 in March)

UK 53.9 vs 53.7 (and 51 in March)

Positions: None.