Premarket SPY, QQQ Moves

With S&P futures rallying to -56 handles I have sold my Index trading long rentals ahead of the inflation data for a very small profit:

* SPY ($SPY) $731.68

* QQQ ($QQQ) $699.18

Positions: none.

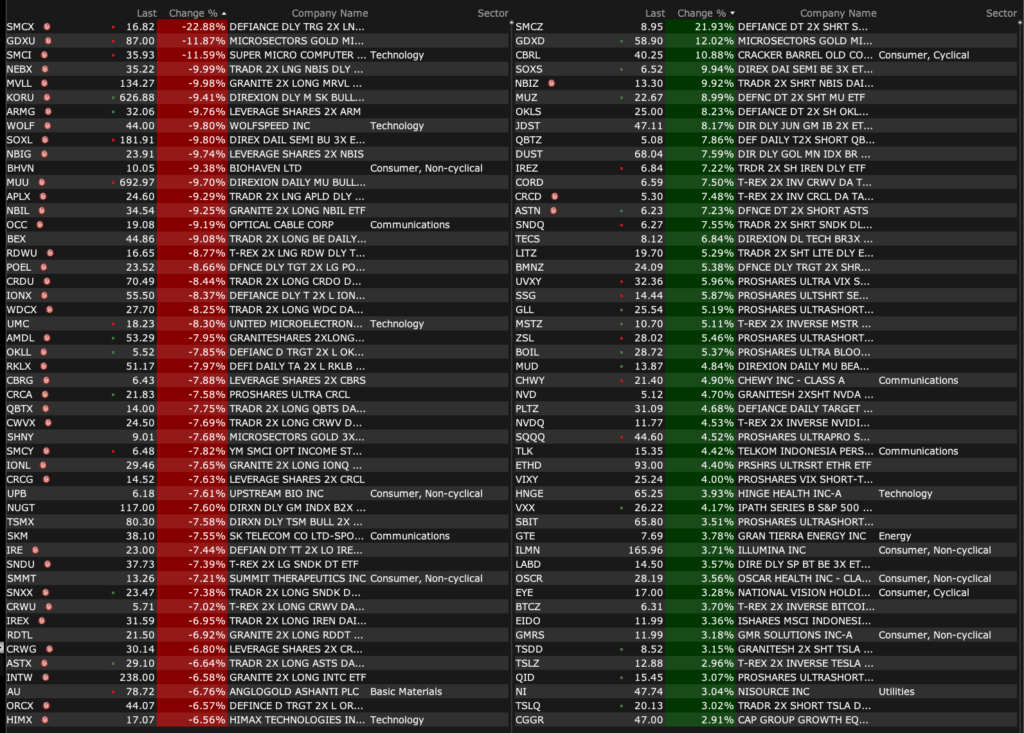

Charting the Premarket Percent Movers

Positions: None.

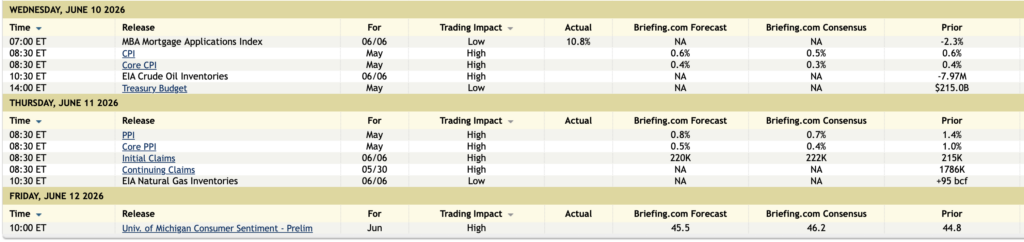

Treasury Auctions, Economic Calendar

Treasury Auctions

11:00 a.m.: Treasury buyback announcement (cash mgmt);

11:30 a.m.: Treasury hosts a $69B 17-Week Bill Auction;

1:00 p.m.: Treasury hosts a $39B 10-Year Note Auction;

Economic Calendar

Positions: None.

Tweet of the Day (Part Five)

Position: None

May CPI, End to Ceasefire?: 8 Key Items Shaping the Stock Market Wednesday

TSM’s May revenue, SpaceX’s oversubscription, bank stress tests, and other headlines are moving stocks this morning.

A Downed Copter, Sinking Sentiment, and a Giant IPO Called SpaceX

Let’s look at how market sentiment on thin ice can absorb a failing ceasefire and a mega-IPO. Also, put Saronic on your radar.

Adding to My Trading Long Rentals

With S&P futures -84 handles and Nasdaq futures -480 handles, I am adding to my trading long rentals:

* $SPY $728.88

* $QQQ $695.71

Position: Long SPY (VS), QQQ (VS)

Tweet of the Day (Part Four)

Position: None